Key Stats

- Current Price: ~$95 (May 6, 2026)

- Q1 2026 Revenue: $2.1B, up ~10% YoY

- Q1 2026 Adjusted EPS: $1.23, up ~8% YoY

- Q1 2026 Adjusted EBITDA: $881M, up ~9% YoY; margin of ~42%

- Full-Year 2026 Organic Revenue Growth Guidance: 7.5% to 8% (Big 3 at ~9.5%)

- Full-Year 2026 Adjusted EBITDA Margin Guidance: ~40% (up ~100 bps YoY)

- Full-Year 2026 Free Cash Flow Guidance: ~$2.1B

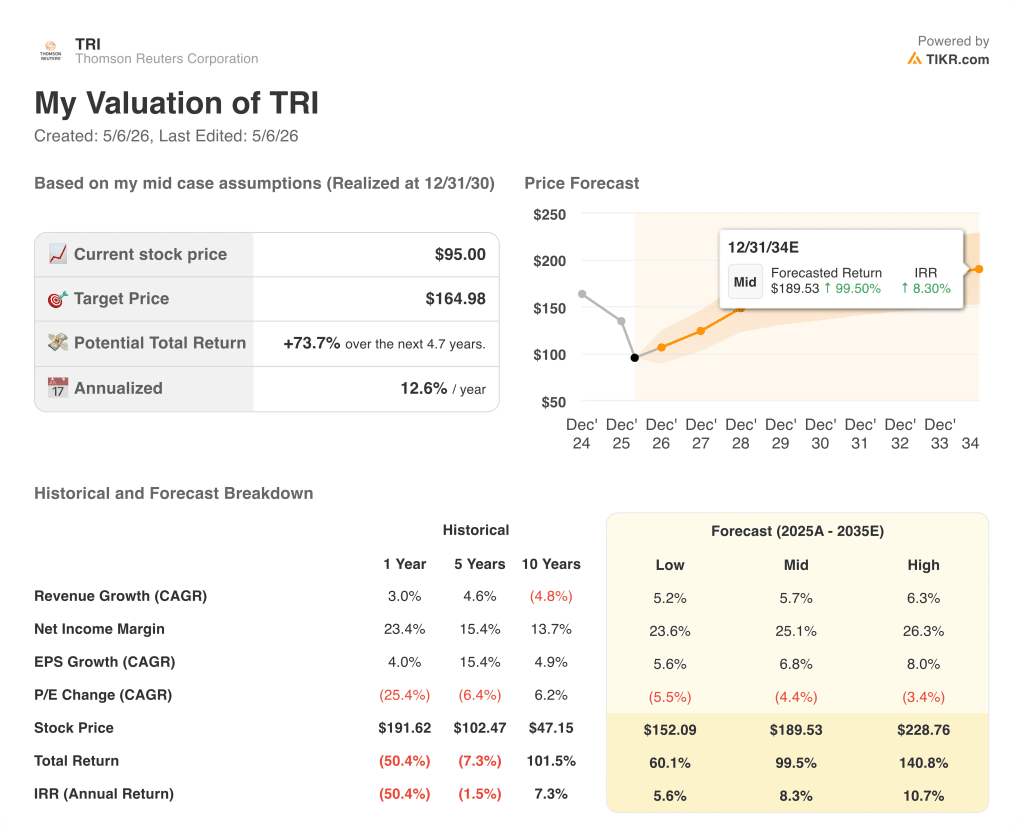

- TIKR Model Price Target: ~$165

- Implied Upside: ~74%

Thomson Reuters Stock Posts a Clean Beat as AI Adoption Accelerates

Thomson Reuters stock (TRI) opened Q1 2026 with $2.1B in revenue, up ~10% year-over-year and slightly ahead of prior guidance, as accelerating AI adoption lifted the Big 3 segments to 9% organic growth.

Adjusted EPS came in at $1.23, up from $1.12 in Q1 2025, according to CEO Steve Hasker and CFO Mike Eastwood on the Q1 2026 earnings call last May 5.

The Legal Professionals segment was the standout driver, with organic revenue up 9% overall and Legal ex-Government accelerating to 11%, up from 9% in Q4 2025, according to Eastwood.

That acceleration was powered by Westlaw Advantage, the agentic deep research product launched in August 2025, with Eastwood noting adoption is tracking faster than the two prior Westlaw upgrade cycles across large, mid, and small law segments.

Corporates grew 9% organically, with transactional revenue rising 12%, driven by Pagero, Confirmation, and international businesses.

Tax, Audit & Accounting delivered 10% organic growth, though Eastwood noted two product updates shifted revenue recognition toward the second half, leaving full-year guidance of 11% to 13% growth unchanged.

Reuters grew 6% organically, driven by the LSEG news agreement and Agency business, while Global Print declined 5% in line with expectations.

Adjusted EBITDA rose 9% to $881M with a margin of ~42%, inclusive of $12M in severance tied to ongoing efficiency initiatives.

Free cash flow reached $332M in Q1, up 19% from $277M in the prior-year period, with EBITDA growth cited as the primary driver.

Thomson Reuters reaffirmed full-year 2026 organic growth guidance of 7.5% to 8%, raised Legal Professionals guidance to approximately 9% (from the prior 8% to 9% range), and expects approximately $2.1B in free cash flow for the year.

The company returned $262M through share repurchases in Q1 and completed a $605M return of capital on May 4, together reducing the share count by approximately 2%, according to Eastwood.

Thomson Reuters Stock Financials: Operating Leverage Intact as Margins Hold

The income statement shows a business maintaining margin stability while re-accelerating revenue growth, following a period of muted YoY gains through 2025.

Total revenues rose from $1.90B in Q1 2025 to $2.09B in Q1 2026, with YoY growth re-accelerating from the 0.8% to 5.2% range that characterized the 2025 quarters.

Gross margin held at ~42% in Q1 2026, consistent with Q1 2025’s ~42%, and above the troughs of ~36% to ~38% seen in the mid-2024 and mid-2025 periods.

Operating income reached $660M in Q1 2026, up from $560M in Q1 2025, with the operating margin at ~32%, roughly flat YoY and well above the ~24% to ~24% troughs in the mid-year quarters.

Eastwood attributed the Q2 margin step-down to ~38% to Tax, Audit seasonality, higher LLM costs tied to Westlaw Advantage, and modest M&A dilution, while flagging that all three factors begin to normalize in H2, supporting the full-year target of approximately 40% EBITDA margin.

What Does the Valuation Model Say?

The TIKR model prices Thomson Reuters stock at ~$165, implying approximately 74% total upside from the current price of ~$95 over roughly 4.7 years, with an annualized return of ~13%.

The mid-case model assumes a revenue CAGR of approximately 5.7% and a net income margin of approximately 25%, a meaningful step up from the 23.4% margin delivered over the past year.

Q1’s clean beat on revenue and free cash flow, combined with the Legal guidance raise and accelerating AI product adoption, modestly strengthens the base case toward the mid-to-high scenario range.

The investment case for Thomson Reuters stock rests on whether AI monetization can sustain organic growth above 8% while the margin expansion pathway holds through rising LLM costs and integration spend.

Thomson Reuters stock enters the second quarter with 8% organic growth already in hand, but whether that pace can hold depends almost entirely on how quickly CoCounsel Legal next converts beta momentum into booked revenue.

What Has to Go Right

- Legal ex-Government sustaining 11% organic growth through Q2 and beyond as Westlaw Advantage adoption penetrates mid and small law after strong Q1 traction across all firm sizes

- CoCounsel Legal next launching in Q3 and contributing meaningful Q4 revenue recognition, with Eastwood flagging strong beta momentum and the larger uplift expected in 2027

- AI-enabled ACV, currently at 30% of total, continuing to increase 2 to 3 percentage points per quarter as newer products including ONESOURCE become gen AI-enabled

- Free cash flow of approximately $2.1B for the year enabling continued buybacks, with approximately $338M of remaining NCIB capacity planned for Q2

What Could Still Go Wrong

- Government legal growth stuck at 1% in Q1, with a full recovery contingent on lapping H2 2025 cancellations and downgrades that may not fully normalize until late 2026 or 2027

- LLM costs increasing in Q1 and Q2 as Westlaw Advantage scales, creating a headwind to margin that depends on the proprietary Thomson model delivering cost relief before it is fully production-ready

- Tax, Audit and Accounting at 10% organic growth in Q1 impacted by revenue recognition timing, with full-year 11% to 13% guidance requiring H2 acceleration that has not yet been demonstrated

- Transactional revenue moderation flagged for Q2, with Corporates growth expected to slow from Q1 levels due in part to pull-forward activity

Should You Invest in Thomson Reuters Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Thomson Reuters stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Thomson Reuters Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze TRI stock on TIKR for Free →