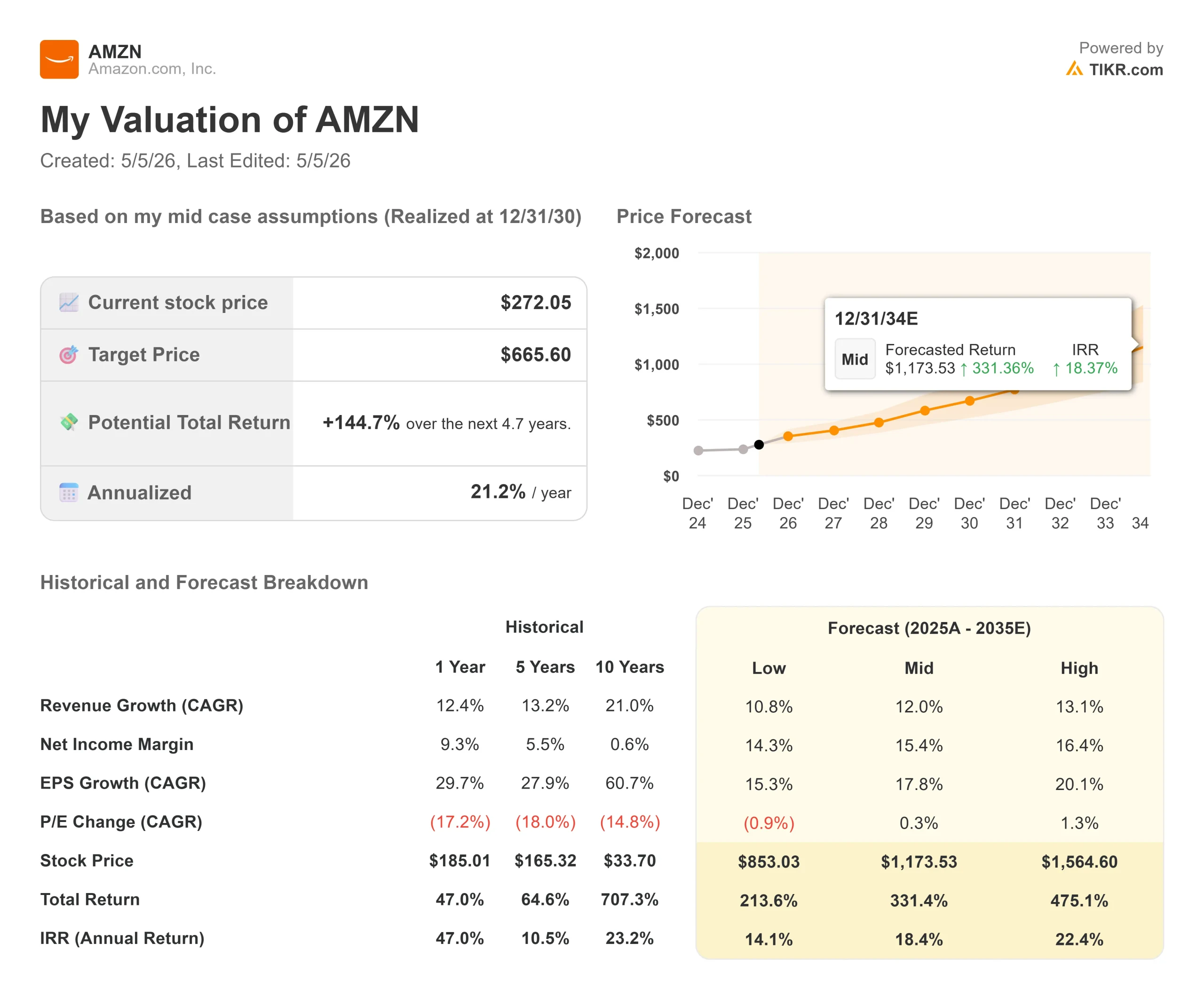

Key Stats for Amazon Stock

- Current Price: $277.61

- Target Price (Mid): ~$666

- Street Target: ~$308

- Potential Total Return: ~145%

- Annualized IRR: ~21% / year

- Earnings Reaction: +0.77% (April 29, 2026)

- Max Drawdown: 21.74% (February 13, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Amazon (AMZN) stock closed up just 0.77% after posting its highest operating margin on record. That muted reaction tells you something. The stock had rallied over 30% in the month heading into earnings, and when a company beats revenue by $4 billion and produces record profitability, a near-flat close means the market has already moved on to a harder question.

Bulls point to accelerating cloud growth, record margins, and a chip business, CEO Andy Jassy says would be worth $50 billion as a standalone company. Bears focus on $43.2 billion in quarterly capital expenditure and a free cash flow line that TIKR estimates turns negative in 2026. The unresolved question is whether Amazon is building the next AWS or stretching capital across too many bets at once.

What the Quarter Delivered

Net sales reached $181.5 billion in Q1 2026, up 17% year-over-year, beating the $177.3 billion Wall Street consensus. EPS came in at $2.78 against a $1.64 estimate a 69% beat per TIKR’s Beats & Misses data. One important qualifier: Amazon’s Q1 2026 press release confirms the net income figure includes $16.8 billion in pre-tax gains from its Anthropic investment. The operational beat is still real operating income, which cleared the top of management’s own guidance range by $2.4 billion, but the headline EPS overstates the core business performance.

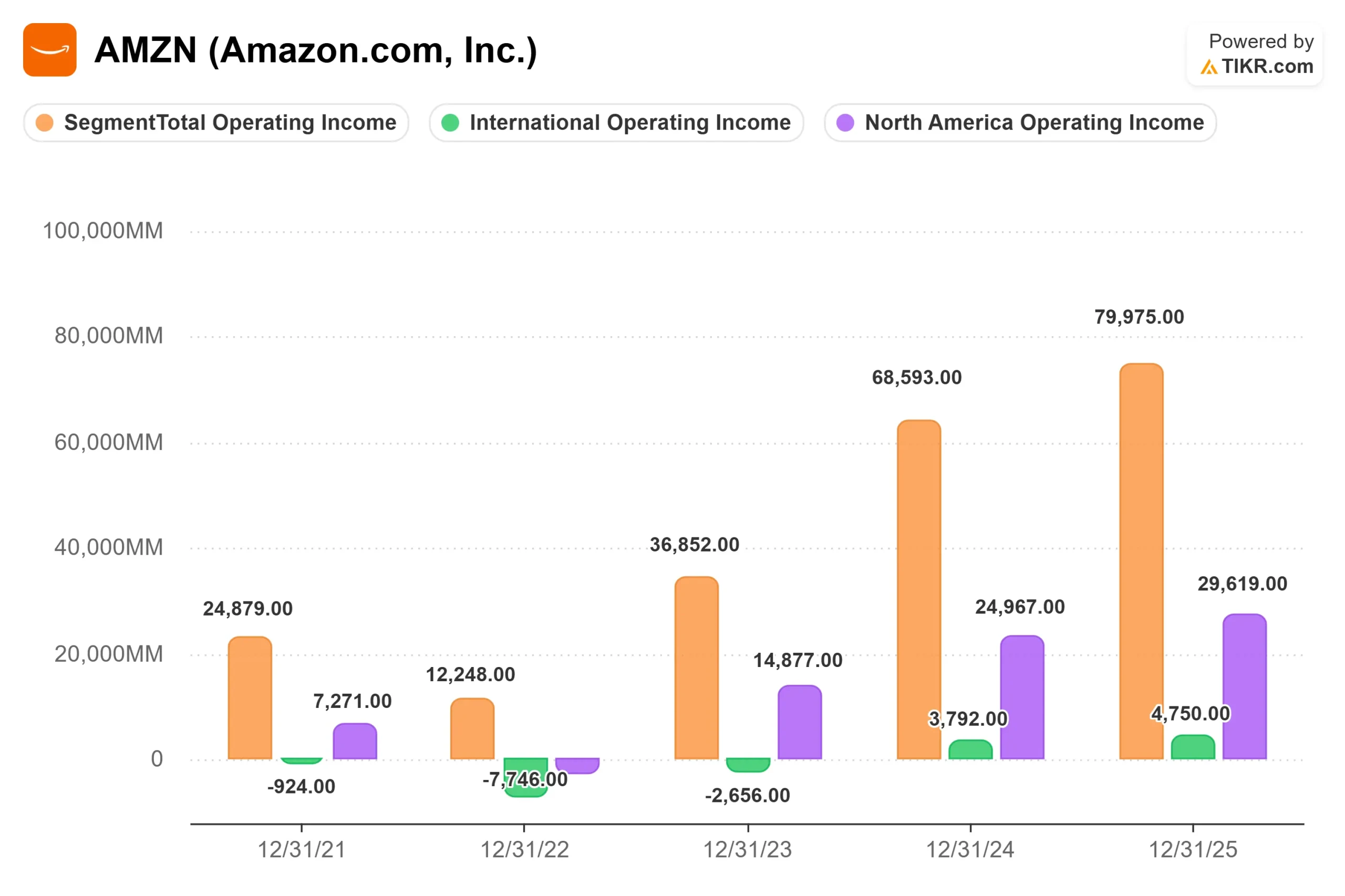

Operating income of $23.9 billion produced a 13.1% margin, the highest Amazon has ever recorded, per CFO Brian Olsavsky on the earnings call.

AWS drove the result. Revenue reached $37.6 billion, up 28% year-over-year, the fastest rate in 15 quarters, at a 37.7% segment operating margin. Advertising contributed $17.2 billion, up 24% year-over-year per Amazon’s Q1 2026 earnings release. Unit growth in stores reached 15%, the fastest since the COVID lockdown era. Outbound shipping costs grew 12%, and fulfillment expense grew 9% on an FX-neutral basis, with costs running below volume growth, which is what operating leverage looks like in practice.

For Q2, Amazon guided revenue of $194 billion to $199 billion and operating income of $20 billion to $24 billion, with Prime Day moving to Q2 for most major geographies, including the U.S.

See historical and forward estimates for Amazon stock (It’s free!) >>>

The Business the Market Hasn’t Fully Priced

Here is where the article diverges from a standard Q1 recap. The most consequential news Amazon delivered in April wasn’t a financial line item, it was a strategic one.

On April 14, Amazon announced an agreement to acquire Globalstar for approximately $10.8 billion. Globalstar currently powers Apple’s iPhone Emergency SOS satellite feature and holds globally harmonized mobile satellite spectrum, a scarce, regulated asset that allows satellites to communicate directly with standard smartphones. That capability is something Amazon Leo, Amazon’s low-Earth-orbit satellite internet service, cannot currently deliver from its broadband network alone. Alongside the acquisition, Amazon and Apple entered an agreement for Amazon Leo to power satellite features on future iPhones and Apple Watches, including Emergency SOS, Messages, Find My, and roadside assistance.

Amazon Leo’s commercial service is on track for Q3 2026, per Jassy on the Q1 earnings call. Enterprise customers are already signed before launch: Delta Airlines, JetBlue, AT&T, Vodafone, DIRECTV Latin America, Australia’s National Broadband Network, and NASA, among others. Delta has committed to at least half its fleet starting in 2028. Over 20 satellite launches are planned for 2026 and more than 30 for 2027, per Jassy’s remarks.

Jassy was direct about the scale he expects: “The business has a chance to be a very large many-billion-dollar revenue business.” He drew an explicit parallel to early AWS capital-intensive upfront, with free cash flow and ROIC characteristics improving materially once capacity monetizes. The near-term cost is already visible: management guided approximately $1 billion in year-over-year Q2 cost increases tied to Leo satellite manufacturing ahead of the commercial launch.

See how Amazon performs against its peers in TIKR (It’s free!) >>>

The Capex Debate

Amazon spent $43.2 billion on capital expenditure in Q1 alone. TIKR consensus estimates show free cash flow turning negative for the full-year 2026 as the $200 billion annual commitment runs ahead of revenue monetization. LTM levered free cash flow stands at $26.9 billion per TIKR data, but the near-term trajectory compresses that figure sharply. BofA’s post-earnings research note expects free cash flow to remain negative through both 2026 and 2027.

Jassy’s counterargument is the demand already locked in against that capacity. The AWS backlog stood at $364 billion at Q1-end, excluding the Anthropic deal, Jassy confirmed, and exceeded $100 billion. Trainium revenue commitments exceed $225 billion, per his Q1 call remarks. Trainium2 is largely sold out. Trainium3, which began shipping in early 2026, is nearly fully subscribed. Much of Trainium4, roughly 18 months from broad availability, is already reserved.

The risk is real: three simultaneous bets on AI infrastructure, satellites, and agentic commerce could prove harder to monetize together than each appeared individually. The Q2 operating income guidance range of $20 billion to $24 billion is wide, reflecting genuine uncertainty around Leo manufacturing costs and the timing of stock-based compensation headwinds.

Wall Street is siding with the long-term case: 46 Buys, 15 Outperforms, 5 Holds, zero Underperforms, and zero Sells per TIKR as of May 4, 2026, with a mean Street target of ~$308.

TIKR Advanced Model Analysis

- Current Price: $277.61

- Target Price (Mid): ~$666

- Potential Total Return: ~145%

- Annualized IRR: ~21% / year

See analysts’ growth forecasts and price targets for Amazon stock (It’s free!) >>>

The TIKR mid-case model uses a 12% revenue CAGR and a ~15% net income margin as its central assumptions. The two primary revenue drivers are AWS accelerating as enterprise AI moves from pilot to production, and advertising compounding as Prime Video inventory scales and agentic commerce expands sponsored placement formats. TIKR consensus estimates project revenue growing from $716.9 billion in 2025 toward approximately $1.31 trillion by 2030, with EBITDA margins expanding toward around 38% over the same period.

The margin driver is operating leverage at AWS. At scale, Jassy said Trainium is expected to save Amazon tens of billions in annual CapEx and provide several hundred basis points of operating margin advantage versus relying on external chips for inference.

The downside: FCF remaining negative through 2027, AWS growth decelerating toward 20%, and Leo facing regulatory delays against a Starlink competitor already operating over 10,000 satellites serving more than 9 million subscribers. The TIKR model entry price was $272.05. The current price of $277.61 is a modest premium to that level.

Conclusion

The key metric at Amazon’s next earnings report, scheduled for July 31, 2026, is AWS growth rate for Q2. A result at or above 26% confirms the acceleration is structural. The secondary watch item is the Leo cost line: any upward revision to the guided $1 billion Q2 manufacturing expense before commercial service launches would reopen the capex discipline debate. Amazon is building a third profit engine alongside cloud and advertising. Whether that engine looks like AWS in 2015 is the question the stock is currently being asked to answer.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Amazon?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Amazon, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Amazon alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!