Key Stats

- Current Price: $355 (May 5, 2026)

- Q1 2026 Revenue: $10.3B (+38% YoY)

- Q1 2026 Non-GAAP EPS: $1.37 (+43% YoY)

- Q2 2026 Revenue Guidance: ~$11.2B (+/- $300M; ~46% YoY)

- Q2 2026 Non-GAAP Gross Margin Guidance: ~56%

- TIKR Model Price Target: $917

- Implied Upside: ~158%

AMD Stock Earnings Breakdown

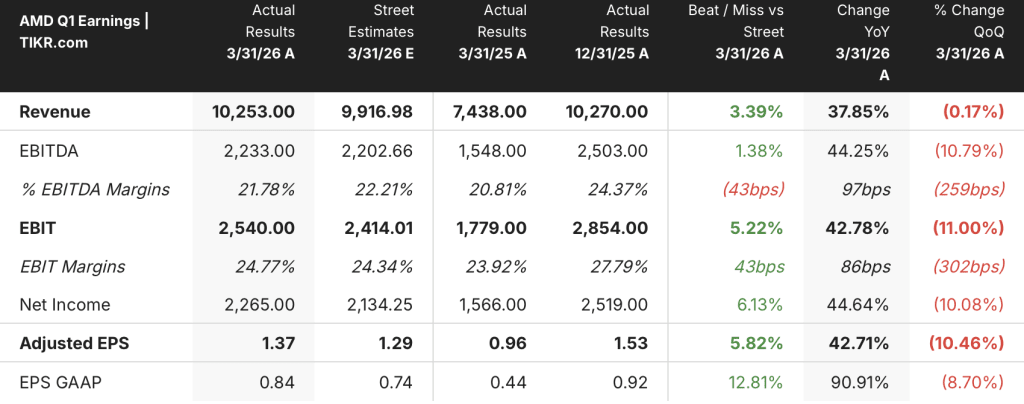

Advanced Micro Devices stock (AMD) delivered Q1 2026 revenue of $10.3B, up 38% year over year, with non-GAAP EPS of $1.37, up 43% year over year.

Data Center revenue hit a record $5.8B, up 57% year over year and 7% sequentially, driven by both EPYC server CPUs and Instinct GPU ramp.

Server CPU revenue grew more than 50% year over year, with sales to both cloud and enterprise customers each expanding more than 50%, according to Chair and CEO Lisa Su on the Q1 2026 earnings call.

AMD expanded its Instinct GPU partnership with Meta to deploy up to 6 gigawatts of AMD Instinct GPUs spanning multiple product generations, including a custom GPU accelerator based on the MI450 architecture.

Client and Gaming segment revenue reached $3.6B, up 23% year over year, with client revenue of $2.9B up 26% driven by Ryzen processor demand and commercial PC share gains.

Gaming revenue came in at $720M, up 11% year over year, though semi-custom revenue declined as expected given the console cycle stage.

Embedded segment revenue was $873M, up 6% year over year, with design win momentum growing by a double-digit percentage year over year across new markets.

Free cash flow more than tripled to a record $2.6B, representing 25% of revenue, according to CFO Jean Hu on the Q1 2026 earnings call.

For Q2 2026, AMD guided revenue of approximately $11.2B (plus or minus $300M), implying roughly 46% year-over-year growth, with non-GAAP gross margin of approximately 56%.

AMD also flagged a headwind: management expects second-half gaming revenue to decline more than 20% compared to the first half, and second-half PC shipments to be lower due to higher memory and component costs.

AMD Stock Financials

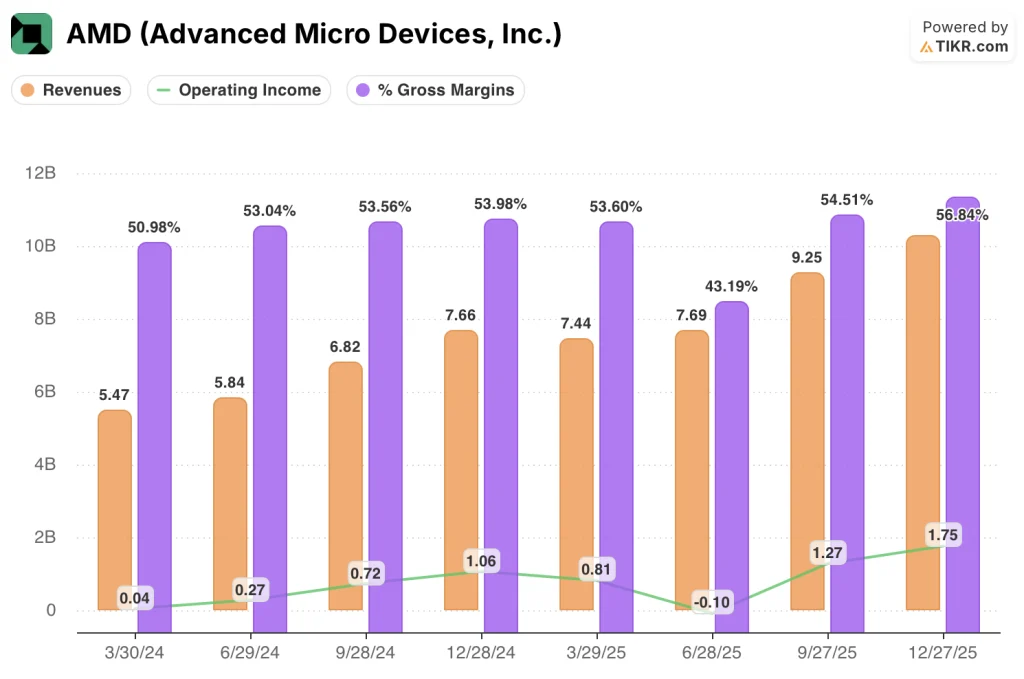

AMD stock’s income statement tells a clear operating leverage story: gross margin expanding toward the upper end of long-term targets while operating income has compounded sharply off a near-zero base.

Revenue grew from $7.44B in Q1 2025 to $7.69B in Q2, $9.25B in Q3, and $10.27B in Q4 2025, before reaching $10.3B in Q1 2026, up 38% year over year, per the Q1 2026 earnings call.

Gross margin in Q4 2025 reached 56.8%, expanding from 54.5% in Q3 2025 and recovering sharply from the 43.2% trough in Q2 2025, which was distorted by an unfavorable product mix during that quarter.

Operating income in Q4 2025 reached $1.75B at a 17.1% operating margin, up from $1.27B and 13.7% in Q3 2025.

A year prior, in Q1 2025, operating income stood at $810M on a 10.8% operating margin, making the trajectory over the past four quarters a near-doubling of operating dollars.

On the Q1 2026 earnings call, CFO Jean Hu confirmed non-GAAP gross margin of 55% for the most recent quarter, up 170 basis points year over year, with Q2 2026 guided to approximately 56%.

Management attributed the gross margin expansion to a favorable product mix, specifically the rising contribution of Data Center revenue, where the segment generated $1.6B in operating income at a 28% segment margin, according to Jean Hu on the Q1 2026 earnings call.

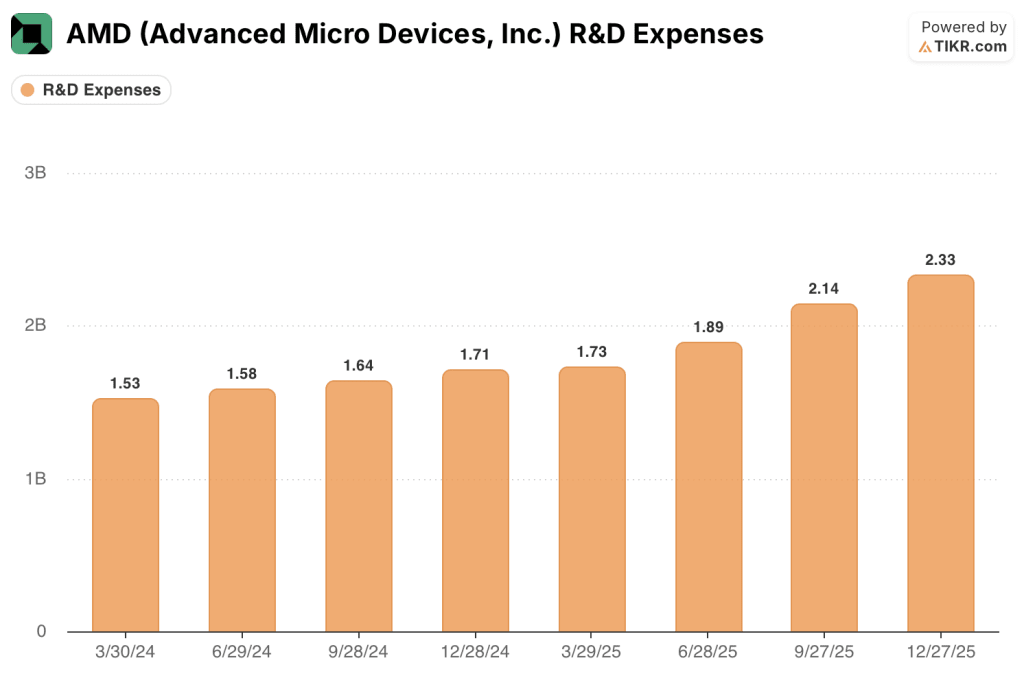

Meanwhile, non-GAAP operating expenses of $3.1B in Q1 2026 grew 42% year over year, with management guiding $3.3B for Q2, reflecting continued R&D investment that has risen every quarter from $1.73B in Q1 2025 to $2.33B in Q4 2025, consistent with AMD’s accelerating AI roadmap spend.

What Does the Valuation Model Say?

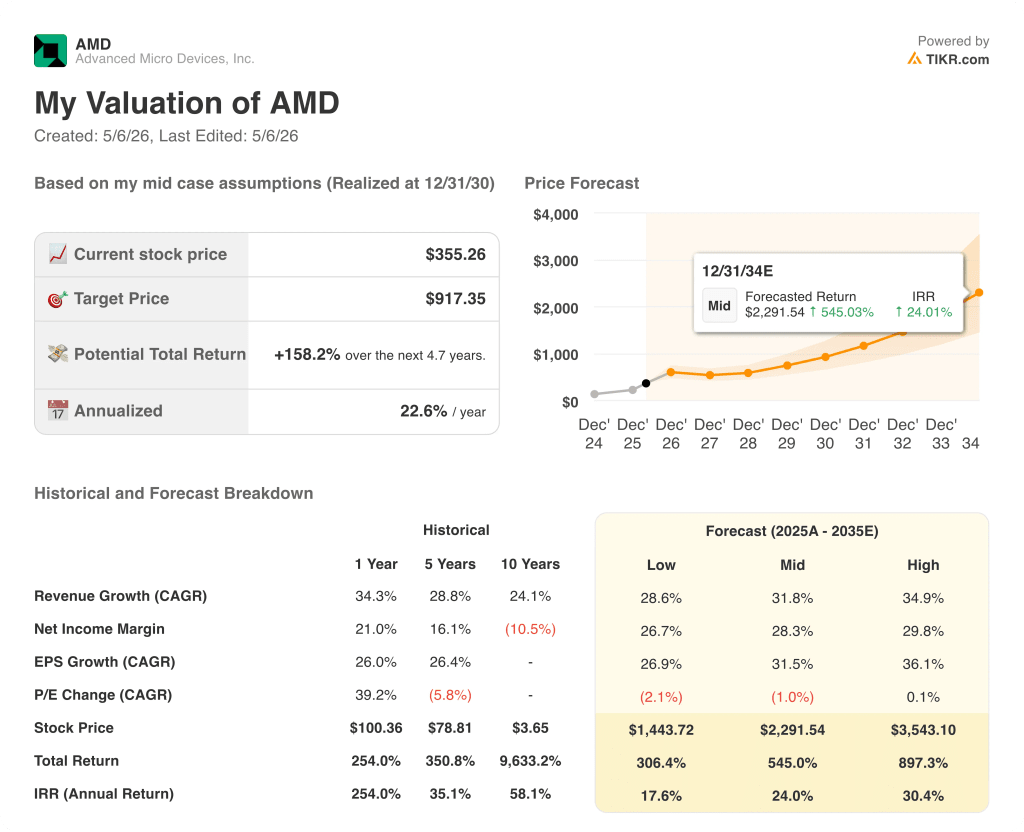

The TIKR valuation model sets a mid-case price target of $917 for AMD stock, implying roughly 158% upside from the current price of $355 over approximately 4.7 years, at an annualized return of 22.6%.

The model assumes a revenue CAGR of 31.8% (mid case), a net income margin of 28.3%, and EPS CAGR of 31.5%, all measured through 2035.

Q1 2026’s combination of 38% revenue growth, record free cash flow, and a Q2 guide implying 46% year-over-year expansion positions AMD ahead of the model’s near-term trajectory, strengthening the base case.

AMD stock’s investment case is materially stronger after this report: accelerating Data Center revenue, a TAM upgrade for server CPUs from $60B to over $120B by 2030, and expanding multi-gigawatt customer commitments for MI450 all point toward the mid-to-high scenario range.

AMD’s Q1 beat and Q2 guide above prior expectations puts the investment argument squarely on one question: whether the Helios/MI450 ramp in the second half of 2026 executes at the scale management is signaling, or whether it slips.

What Has to Go Right

- Helios production ramp begins initial volume in Q3 2026 and scales significantly in Q4, as Lisa Su outlined on the earnings call, with “tens of billions” in annual Data Center AI revenue targeted for 2027

- Server CPU growth sustains above 70% year over year in Q2 and continues through the second half, supported by Venice (sixth-gen EPYC on 2-nanometer) and Zen 6 architecture ramping later in 2026

- Meta partnership (up to 6 gigawatts of AMD Instinct GPUs) and OpenAI co-engineering relationships convert into multi-year, predictable revenue streams, expanding gross margin as volume scales

- Gross margin holds near 56% through the second half despite MI450 dilution, supported by server CPU mix, declining gaming revenue, and continued Embedded segment accretion at 39% segment margins

What Could Still Go Wrong

- Data Center AI revenue was described as down modestly sequentially in Q1 due to lower China revenue, a factor that adds geographic concentration risk to the Instinct GPU ramp

- MI450 carries below-corporate-average gross margin and is set to ramp significantly in Q4, creating margin pressure at the exact moment revenue is peaking for the year

- Second-half PC and gaming shipments face a demand headwind from higher memory and component costs, with gaming revenue expected to decline more than 20% versus the first half

- OpEx grew 42% year over year in Q1 and is guided to $3.3B in Q2, outpacing what management characterized as the R&D-led investment model, adding execution risk if revenue growth moderates

Should You Invest in Advanced Micro Devices, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up AMD stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Advanced Micro Devices, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze AMD stock on TIKR for Free →