Key Stats for Duolingo Stock

- Past week’s performance: -7.3%

- 52-week range: $100 to $143

- Valuation model target price: $155

- Implied upside: 26.5% over 2.8 years

Value your favorite stocks like Duolingo with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Duolingo (DUOL) stock is trading like a growth company that lost investor trust in its near-term earnings path. The stock slipped 1.3% this week and closed near $103. That small weekly move hides a much bigger reset, because shares are down sharply from their 52-week high of $545.

The major shift happened after Duolingo’s February earnings update. The company beat Q4 revenue expectations, but investors focused on weaker bookings guidance. Bookings represent customer payments before revenue is recognized, so they are a key signal for future growth.

Management said it is prioritizing user growth over near-term monetization. That means Duolingo is reducing friction from ads and subscription prompts so more people keep using the app. CEO Luis von Ahn said the company is aiming for faster user growth and sees about 20% as a key benchmark for whether the strategy is working.

The strategy also includes expanding AI-powered learning features. Duolingo is moving “Video Call with Lily,” an AI speaking-practice tool, from the higher-priced Max plan into Super Duolingo. That can improve engagement, but it also lowers near-term monetization pressure because more value is being offered at lower tiers.

Investors reacted because the trade-off is real. Reuters reported that Duolingo expects 2026 bookings growth of about 11%, below the roughly 20% growth the company said it could have delivered under its prior approach.

If Duolingo stock is going to stabilize going forward, investors will need proof that stronger user growth can eventually rebuild bookings momentum.

See analysts’ growth forecasts and price targets for DUOL (It’s free) >>>

Is Duolingo Stock Undervalued?

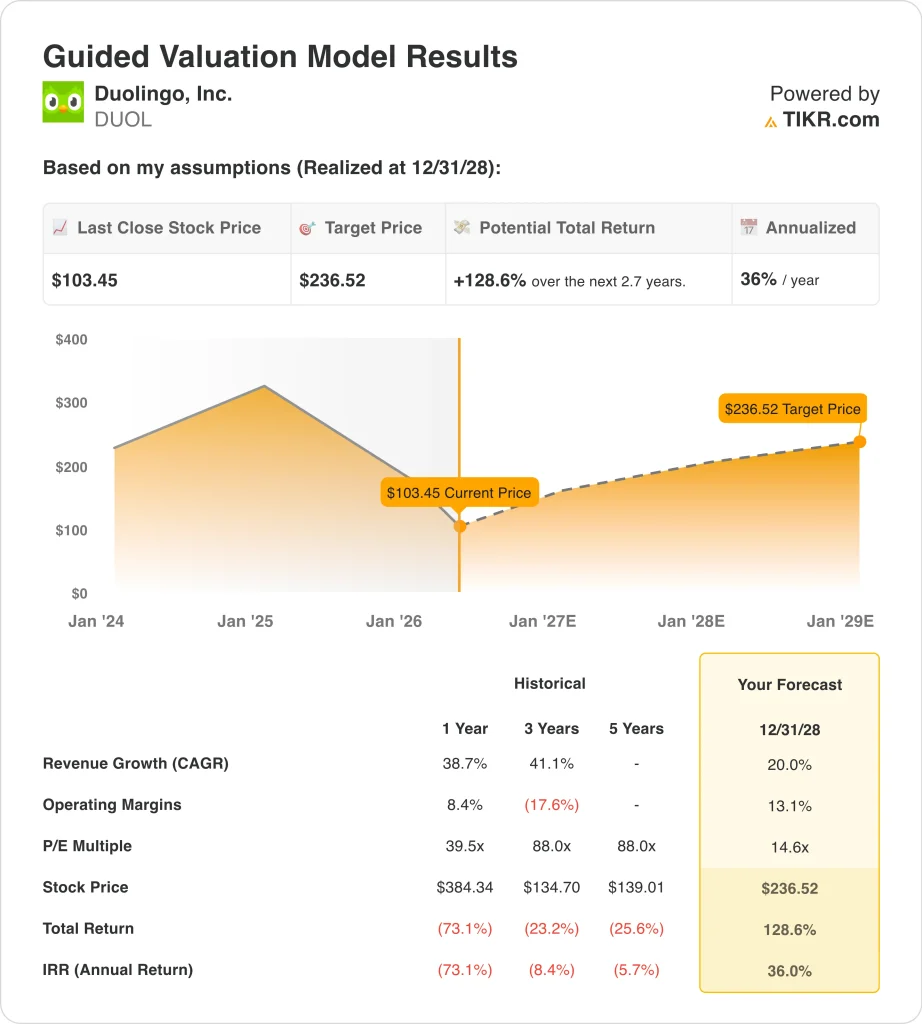

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 20%

- Operating Margins: 13.1%

- Exit P/E Multiple: 14.6x

Based on these inputs, the model estimates a target price of $236.52, implying 128.6% total upside from the current share price and a 36.0% annualized return over the next 2.7 years.

That return profile looks very attractive, but it reflects a major valuation reset. Duolingo trades at 14.6x forward earnings, far below its 1-year historical P/E of 39.5x and 3-year average of 88.0x. The market is no longer paying a premium multiple for growth without cleaner bookings visibility.

The 20.0% revenue growth assumption depends on daily active users, paid subscribers, and AI-driven product adoption. Duolingo has more than 250 language courses and is expanding into math, music, and chess. Those new subjects matter because they can increase time spent in the app.

Margins are the harder part of the story. Duolingo’s LTM gross margin is 72.2%, and its LTM EBIT margin is 13.6%. That is strong for a consumer app, but management’s 2026 strategy could pressure margins as it invests in AI access and marketing.

Duolingo competes with Babbel, Rosetta Stone, Busuu, Memrise, and broader online learning platforms like Coursera. Coursera grew 2025 revenue 9%, while Duolingo grew 38.7%, so Duolingo remains the faster grower. Its moat is brand, gamified learning, organic word-of-mouth, and daily engagement, but user growth must translate back into bookings.

What’s Driving DUOL Stock Going Forward?

Q1 earnings on May 4 will be the next major catalyst. Investors will focus on daily active user growth, bookings, paid subscriber trends, and margin guidance. Duolingo confirmed it will report results after the market closes that day.

AI learning tools will be central to the story. Video Call with Lily is designed to help users practice spoken conversation with an AI character. If lower-cost AI features improve retention, they could support stronger long-term subscription growth.

The company’s balance sheet gives it room to invest. Duolingo has $1.1 billion in cash and short-term investments and a net cash of about $1.0 billion. That helps fund AI development, marketing, and the $400 million buyback authorization.

Profitability remains the main question. Free cash flow reached $370 million in 2025, with a 35.6% free cash flow margin. But investors want to know whether that cash flow can keep growing while Duolingo lowers monetization friction.

The stock’s setup is simple from here. Duolingo needs to show that a better user experience can drive faster user growth without permanently weakening bookings or margins. A strong Q1 update could help, but another weak bookings signal would likely keep pressure on the stock.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Duolingo?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DUOL, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track DUOL alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Duolingo stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!