Key Stats for Starbucks Stock

- Current Price: $98.67

- Target Price (Mid): ~$199

- Street Target: ~$101

- Potential Total Return: ~102%

- Annualized IRR: ~9% / year

- Earnings Reaction: -1.35% (January 28, 2026)

- Max Drawdown: -19.06% (October 10, 2025)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Starbucks (SBUX) stock is up 17% year to date, but bulls and bears are more divided than the price chart suggests.

Bulls point to the first positive U.S. transaction quarter in eight periods and a now-closed China restructuring that removes a major cost drag. Bears point to a North America operating margin that has collapsed and a 40x NTM P/E that prices in a recovery the income statement hasn’t yet confirmed.

The question the market is asking three days before Q2 earnings on April 28: Is the turnaround durable, or is the stock running ahead of the fundamentals?

Two product announcements this week add a new layer to that debate.

First, Starbucks announced that it would be scheduling mobile ordering across North America on May 11. The feature is powered by Starbucks’ Smart Queue algorithm, which automatically sequences and balances orders across drive-thru, in-store, and mobile channels. Nation’s Restaurant News Customers select five-minute pickup windows up to one hour ahead, with availability reflecting real-time store capacity.

That is not a marketing feature. It is throughput management software, and for a company that has publicly committed to operating margins recovering to 13.5%–15% by fiscal 2028, reducing order backlog without adding labor hours is exactly the kind of structural lever that makes a margin target credible.

Second, Starbucks launched a beta app within ChatGPT in mid-April, allowing customers to receive tailored drink suggestions based on mood, preferences, or photos, then complete the order in the Starbucks app. The feature targets drink discovery at the top of the funnel, where Rewards members who explore new customizations tend to spend more per visit.

Brian Niccol, Chairman and Chief Executive Officer, framed both launches at January’s Investor Day: “Customers are responding to our commitment to world-class service, compelling menu innovation, and marketing that truly resonates.”

See historical and forward estimates for Starbucks stock (It’s free!) >>>

Is Starbucks Undervalued Today?

At $98.67, Starbucks trades at a NTM P/E of 40x and an NTM EV/EBITDA of 23.8x.

For context, McDonald’s trades at roughly 22.7x NTM earnings, Chipotle at around 30x, and Yum! Brands at under 24x, based on TIKR competitor data. The peer group median NTM EV/EBITDA sits at 12.6x. Starbucks carries a premium because of its brand, 41,000-plus global locations, and a 35.5 million-member loyalty program. But that premium demands execution.

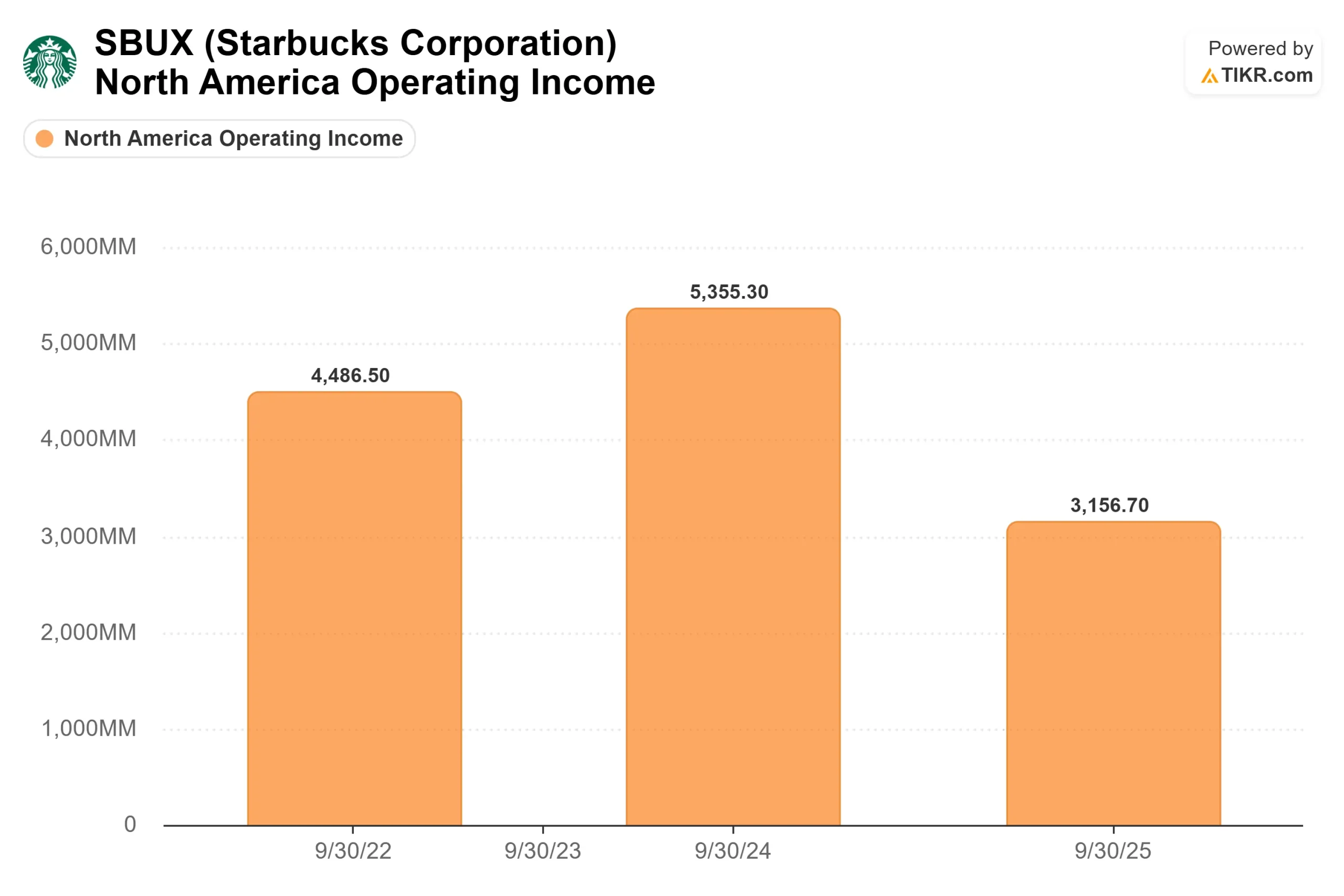

The execution gap is visible in the margins. North America’s operating income fell 41% to $3.2 billion in fiscal 2025 from $5.4 billion in fiscal 2024, driven by the $500 million Green Apron Service labor investment, tariffs, and elevated coffee pricing. LTM net debt stands at $21.9 billion at 2.53x net debt/EBITDA, and free cash flow on a levered trailing basis turned deeply negative. If Q2 earnings on April 28 show the Q1 transaction recovery was seasonal rather than durable, the 40x multiple becomes very hard to justify.

The recovery path has specific mechanics, though. Green Apron Service labor costs begin anniversarying in Q4 fiscal 2026, which means cost comparisons ease structurally in the second half regardless of whether traffic improves further. The China joint venture with Boyu Capital, now closed, converts company-operated China losses into a higher-margin licensing model.

CFO Cathy Smith said on the Q1 fiscal 2026 earnings call that on an annualized basis, the new structure could be approximately 40 basis points accretive to consolidated margins, that is, management guidance, not a guaranteed outcome. And management’s fiscal 2028 framework targets EPS of $3.35–$4.00, which would represent more than 70% earnings growth from fiscal 2025’s normalized EPS of $2.13.

See how Starbucks performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $98.67

- Target Price (Mid): ~$199

- Potential Total Return: ~102%

- Annualized IRR: ~9% / year

See analysts’ growth forecasts and price targets for Starbucks stock (It’s free!) >>>

The TIKR mid-case uses around 5% revenue CAGR through fiscal 2034, consistent with management’s own growth targets once the Green Apron investments anniversary. The two drivers are U.S. comp growth sustaining above 3% as the service model matures across 18,000-plus North American stores, and international revenue rebuilding as Boyu JV licensing fees replace company-operated China costs.

The margin driver is net income recovering from around 6.5% in fiscal 2025 toward around 10% by fiscal 2034. That is still well below the 12%–13% Starbucks posted before the downturn, so the mid-case reflects a partial recovery, not an optimistic one. The primary risk is margin compression persisting beyond fiscal 2026. If North America’s operating margins do not inflect in fiscal 2027, multiple contractions would likely offset the earnings recovery and compress returns. The conservative low-case targets around $160 at 9/30/34 on around 4.6% revenue CAGR and net income margins of around 10%.

Conclusion

Watch U.S. comparable transactions in the Q2 fiscal 2026 report on April 28. One positive quarter was Q1. Two consecutive positive quarters establish a trend and give the margin recovery thesis its most important validation. If that number comes in positive and management reaffirms its fiscal 2026 guidance, the gap between the Street’s ~$101 mean target and the TIKR model’s ~$199 mid-case starts to close in a meaningful way.

Starbucks is not cheap on any trailing metric. But the TIKR model says around 102% total return is available at current prices if the turnaround executes. April 28 is the first real test of whether it will.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Starbucks?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Starbucks, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Starbucks alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Starbucks on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!