Key Stats for DAL Stock

- Past week’s performance: -3.9%

- 52-week range: $40 to $76

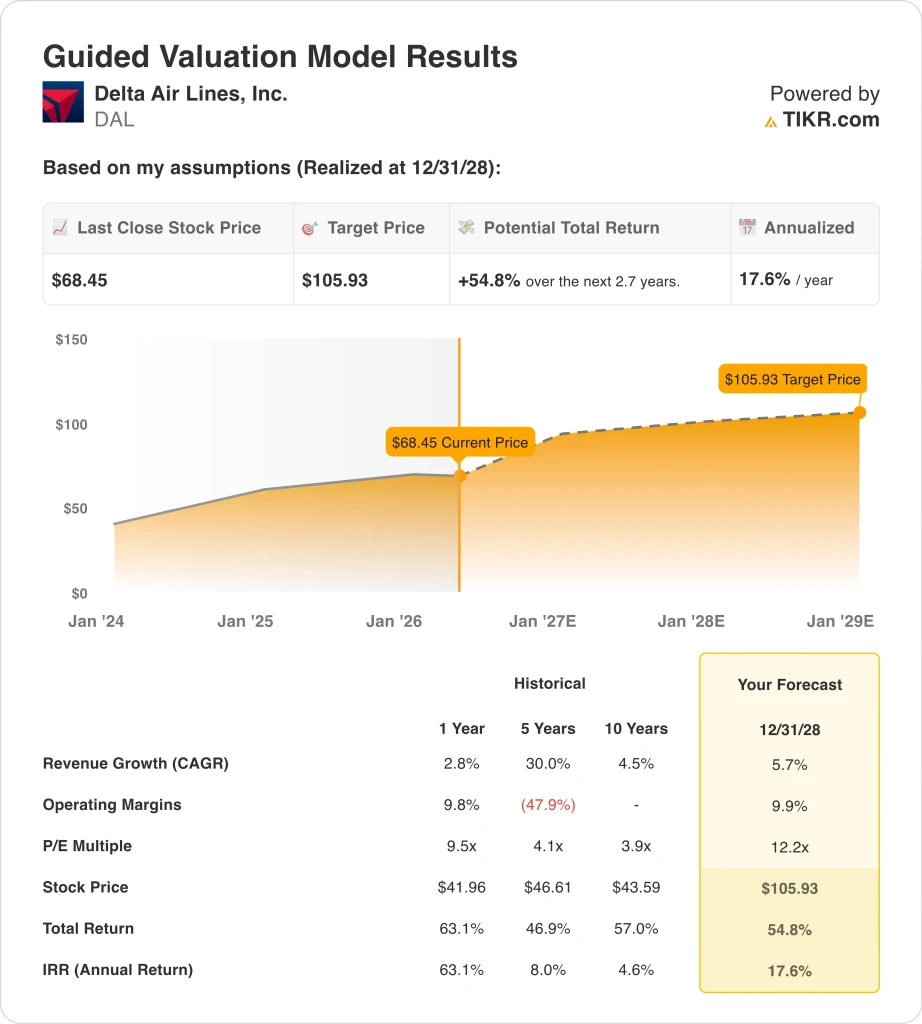

- Valuation model target price: $106

- Implied upside: 54.8% over 2.7 years

Value your favorite stocks like DAL with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Delta Air Lines (DAL) stock fell 3.9% this week as investors focused on rising fuel costs. The airline sector came under pressure after Reuters reported that higher jet fuel prices are squeezing margins across U.S. carriers. Delta still has strong travel demand, but fuel is one of its highest costs, so the market repriced the stock lower.

This follows Delta’s April 8 Q1 report, where management said March fuel prices rose sharply. Delta delivered record March-quarter revenue, but adjusted fuel expense increased 8% year over year. CEO Ed Bastian said Delta delivered “record March quarter revenue,” but the fuel spike made investors more cautious about near-term profits.

The week also had some positive company-specific news. Delta declared a $0.1875 quarterly dividend, payable June 4 to shareholders of record on May 14. That supports the shareholder-return story, but it was not enough to offset concern about fuel and airline margins.

Delta also announced an eight-year TechOps engine maintenance deal with IndiGo. TechOps is Delta’s maintenance, repair, and overhaul business, so the deal adds a non-passenger revenue stream. Still, the stock’s weekly move was mostly about fuel costs, not the maintenance contract.

See analysts’ growth forecasts and price targets for DAL (It’s free) >>>

Is DAL Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 5.7%

- Operating Margins: 9.9%

- Exit P/E Multiple: 12.2x

Based on these inputs, the model estimates a target price of $106, implying 54.8% total upside from the current share price of $68 and an annualized return of 17.6% over the next 2.7 years.

That return looks attractive, but it depends on Delta keeping demand strong while managing fuel volatility. The 5.7% revenue growth assumption is tied to premium travel, international demand, loyalty revenue, and steady capacity growth. It is not just about selling more seats.

The 9.9% operating margin assumption is the key swing factor. Delta’s LTM EBIT margin is 8.6%, so the model assumes some recovery from current levels. That would require fuel costs to stabilize, fares to hold up, and non-fuel costs to stay controlled.

The 12.2x exit P/E is above Delta’s recent historical range. That premium can be justified if Delta keeps producing stronger margins than most airline peers. But if fuel remains elevated, investors may refuse to pay that higher multiple.

What’s Driving DAL Stock Going Forward?

The next major item is the dividend record date on May 14 and payment on June 4. This is not a huge catalyst by itself, but it reinforces that Delta is still returning cash to shareholders. Investors will watch whether future cash flow can support dividends while fuel costs remain high.

Over the next few weeks, jet fuel prices will be the biggest driver. Reuters reported that airlines are cutting growth plans and raising fares because fuel costs have surged. If fuel prices stay high, Delta’s summer profit margins could remain under pressure.

The June 18 shareholder meeting is another near-term event. Investors may look for updates on capital returns, fleet plans, debt reduction, and cost control. Those topics matter because Delta still has $16.3 billion of LTM net debt.

The next major earnings catalyst is Q2 results, expected in July. Investors will focus on summer demand, fare strength, fuel expense, and operating margin. The stock can recover if Delta shows that pricing power is offsetting higher fuel costs.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Delta Air Lines, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DAL, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track DAL alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Delta Air Lines stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!