Key Stats

- Current Price: ~$67

- Q1 2026 Revenue: $13.6B, +7% YoY

- Q1 2026 Non-GAAP EPS: $0.29 (vs. guidance of breakeven)

- Q1 Revenue Beat: $1.4B above guidance midpoint

- Q2 2026 Revenue Guidance (midpoint): $14.3B

- Q2 2026 Non-GAAP EPS Guidance: $0.20

- Q2 2026 Non-GAAP Gross Margin Guidance: 39%

- TIKR Model Price Target: ~$161

- Implied Upside Over ~5 Years: ~141%

Intel’s Q1 2026 Earnings: Six Straight Beats as CPU Demand Surges

Intel stock (INTC) delivered its sixth consecutive quarter of exceeding financial expectations, posting Q1 2026 revenue of $13.6B, which was $1.4B above the midpoint of its own guidance.

Non-GAAP EPS came in at $0.29 against a guidance range of breakeven, driven by higher volume, improved product mix, and pricing actions taken in part to offset rising input costs.

The single biggest driver was the Data Center and AI segment: DCAI revenue of $5.1B grew 22% year-over-year and 7% sequentially, well above internal expectations.

CEO Lip-Bu Tan attributed the strength to a structural shift in AI workload patterns, stating the CPU “now serves as the orchestration layer and critical control plane for the entire AI stack.”

Intel’s AI-driven businesses represent 60% of total revenue and grew 40% year-over-year, according to CFO David Zinsner on the Q1 2026 earnings call.

The Client Computing Group posted revenue of $7.7B, down 6% sequentially but better than expectations, with AI PC revenue growing 8% sequentially and now exceeding 60% of client CPU mix.

CCG operating profit was $2.5B, 33% of segment revenue, up roughly $300M quarter-over-quarter on improved mix and sales of previously reserved inventory.

Intel Foundry posted revenue of $5.4B, up 20% sequentially, carrying an operating loss of $2.4B as the company absorbed early ramp costs for Intel 18A.

18A yields are running ahead of internal projections, on pace to hit year-end targets by mid-2026, according to Zinsner on the Q1 2026 earnings call.

Intel guided Q2 revenue to $13.8B to $14.8B, with DCAI expected to grow double digits sequentially and CCG growing modestly.

Q2 non-GAAP gross margin is guided to 39%, down from 41% in Q1, as 18A mix grows roughly 6-7x in volume and the Q1 inventory benefit does not repeat.

The ASIC business, included in DCAI, more than doubled year-over-year and is already running above a $1B annual revenue rate, according to Zinsner on the Q1 2026 earnings call.

Intel Stock’s Income Statement: A Recovery in Progress, With Margin Stability Still Ahead

Intel stock’s income statement shows a company emerging from deep operating losses, with gross margin volatility reflecting the cost of ramping two new nodes simultaneously.

Gross margin compressed to a low of 33.7% in Q2 2025 before recovering to 38.2% in Q3 2025 and 37.3% in Q4 2025.

Q1 2026 non-GAAP gross margin came in at 41%, approximately 650 basis points ahead of guidance, according to CFO David Zinsner on the Q1 2026 earnings call, driven by volume, mix, pricing, and previously reserved inventory.

Operating income swung from a loss of $490M in Q2 2025 to a gain of $860M in Q3 2025, then settled at $700M in Q4 2025 at a 5.1% operating margin.

Operating margin was still negative in Q1 2025 at (0.2%) and Q2 2025 at (3.8%), making the turn to consistent positive territory a meaningful step for Intel stock.

Zinsner flagged gross margin expansion as his top priority, noting on the Q1 call that 18A remains below corporate average and that rising memory, substrate, and wafer costs present growing headwinds into the second half.

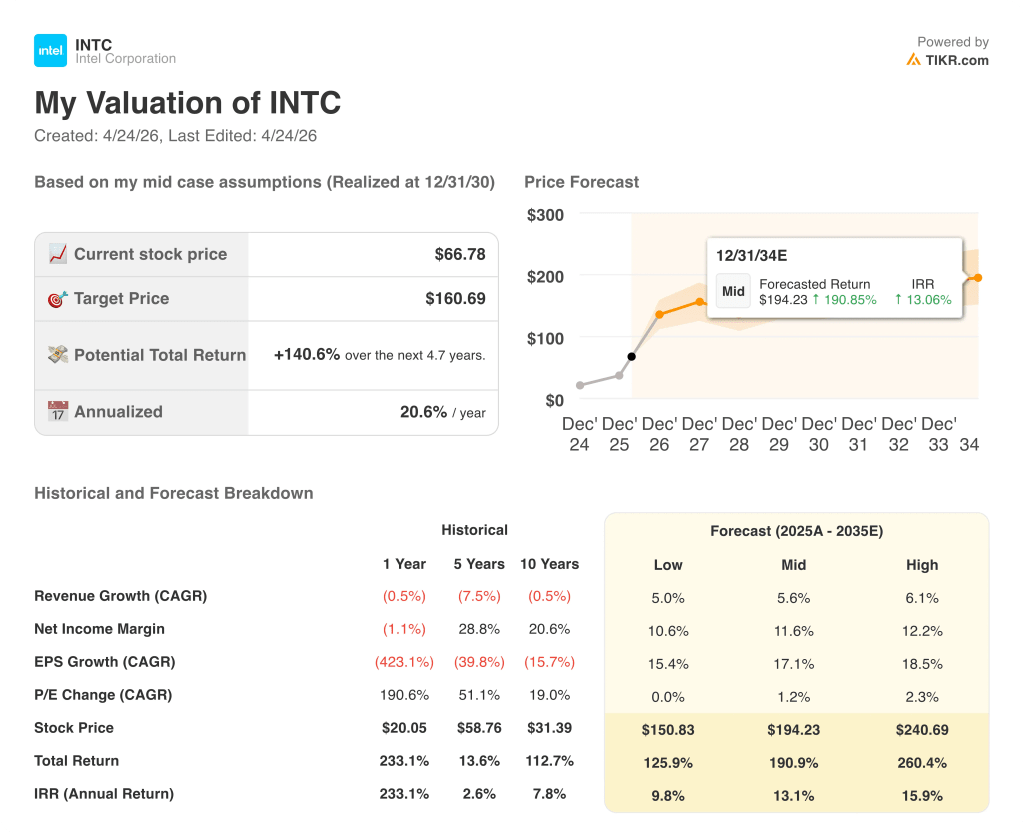

What Does the Valuation Model Say?

The TIKR model prices Intel stock at a target of ~$161, implying roughly 141% upside from the current price of ~$67, based on a mid-case revenue CAGR of 5.6% and a net income margin of 11.6%.

The annualized return in the mid case is 20.6%, with the full scenario range spanning roughly 126% to 260% in total return.

The Q1 report is broadly consistent with those assumptions: DCAI growing 22% year-over-year, a confirmed multiyear LTA with Google, an ASIC business above a $1B annual run rate, and 18A yields tracking ahead of schedule all support the model’s growth path.

Intel stock is a high-conviction recovery trade if foundry execution holds, but the gap between ~$67 and ~$161 reflects how much needs to go right over the next four years.

Intel stock’s investment case hinges on whether Intel 18A can scale to volume production without derailing the gross margin recovery that the model’s 11% to 12% net income margin targets require.

What Has to Go Right

- Intel 18A yields hit mid-year internal targets, as Zinsner indicated on the Q1 call, enabling the node to approach corporate-average gross margins before year-end

- DCAI sustains double-digit sequential growth into Q2 and beyond, supported by the Google LTA and the structural CPU-to-GPU ratio shift from 1:8 toward parity in agentic workloads

- The ASIC business, already above a $1B annual run rate, scales as purpose-built silicon demand grows from customers in active evaluation

- Intel 14A design commitments begin emerging in H2 2026 as guided, establishing a second foundry revenue layer

What Could Still Go Wrong

- Q2 gross margin guidance of 39% signals compression even after a 41% Q1 print, and memory and substrate cost inflation could widen that gap in the second half

- PC TAM is guided down low double digits for the full year, with CCG revenue expected to flatten from Q2 onward, limiting a key volume lever in the gross margin recovery

- Intel Foundry’s $2.4B Q1 operating loss persists even as yields improve, requiring multiple quarters of below-average margins before becoming accretive to the P&L

- Demand is outpacing supply by a figure management described as starting with a “B,” a constraint that limits near-term upside if factory output improvements fall short

Should You Invest in Intel Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up INTC stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Intel Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze INTC stock on TIKR for Free →