Key Takeaways:

- Adobe trades at approximately 11x forward P/E today, down dramatically from a peak above 35x in late 2023, while Atlassian’s forward P/E has compressed from over 230x in 2021 to roughly 15x currently as the company transitions from growth-at-all-costs to profitability.

- Creative software and digital marketing tools anchor Adobe’s $23.8 billion revenue base, with FCF margins above 41%, while Atlassian grew revenue to approximately $5.2 billion, with FCF margins around 27%, as operating losses persist during its cloud migration investment cycle.

- Analysts project Adobe’s revenue of approximately $26 billion for fiscal 2026, up roughly 10% year-over-year, while Atlassian’s consensus is approximately $6.4 billion, up roughly 22%, reflecting a meaningfully faster growth profile despite the smaller revenue base.

- Under mid-case assumptions, TIKR’s model suggests Adobe could deliver approximately 47% total upside through November 2029 at roughly 11% annualized returns, while Atlassian implies approximately 65% upside through June 2029 at roughly 17% annualized returns.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Dominant positions in software categories that looked nearly impossible to disrupt. Deep customer relationships built over decades. Recurring revenue models with high retention and minimal churn. On paper, these are exactly the kinds of businesses long-term investors are supposed to hold.

And yet the stocks have spent the past two years in sustained drawdowns despite the underlying businesses continuing to grow revenue and expand their product platforms.

The selloff raises a legitimate question. Is this a valuation reset that has created a genuine entry point, or is the market correctly pricing in structural risks that were previously obscured by multiple expansions?

Estimate a company’s fair value instantly (Free with TIKR) >>>

Two Dominant Software Businesses With Very Different Margin Stories

Creative professionals and enterprise marketing teams have built decades of workflow around Adobe’s (ADBE) tools, including Photoshop, Illustrator, Premiere Pro, and its Experience Cloud suite. That deep integration makes switching costly in time and productivity, giving the company unusual pricing power over a subscription base that renews with predictable consistency.

Atlassian (TEAM) operates on a different model entirely. Jira and Confluence spread through organizations from the bottom up, adopted first by individual developers, then expanded across entire engineering teams without a traditional sales force. That go-to-market efficiency has historically produced exceptional unit economics relative to the revenue it generates.

Where the two companies diverge most clearly is in maturity. Adobe is profitable at scale, generating FCF margins above 41% on a nearly $24 billion revenue base. Atlassian is still investing heavily in its cloud migration from legacy server products, with operating margins of roughly negative 2.5% even as revenue has grown and FCF has recovered to around 27%.

Broadcom Trades at a Higher Multiple Than NVIDIA Despite Growing More Slowly

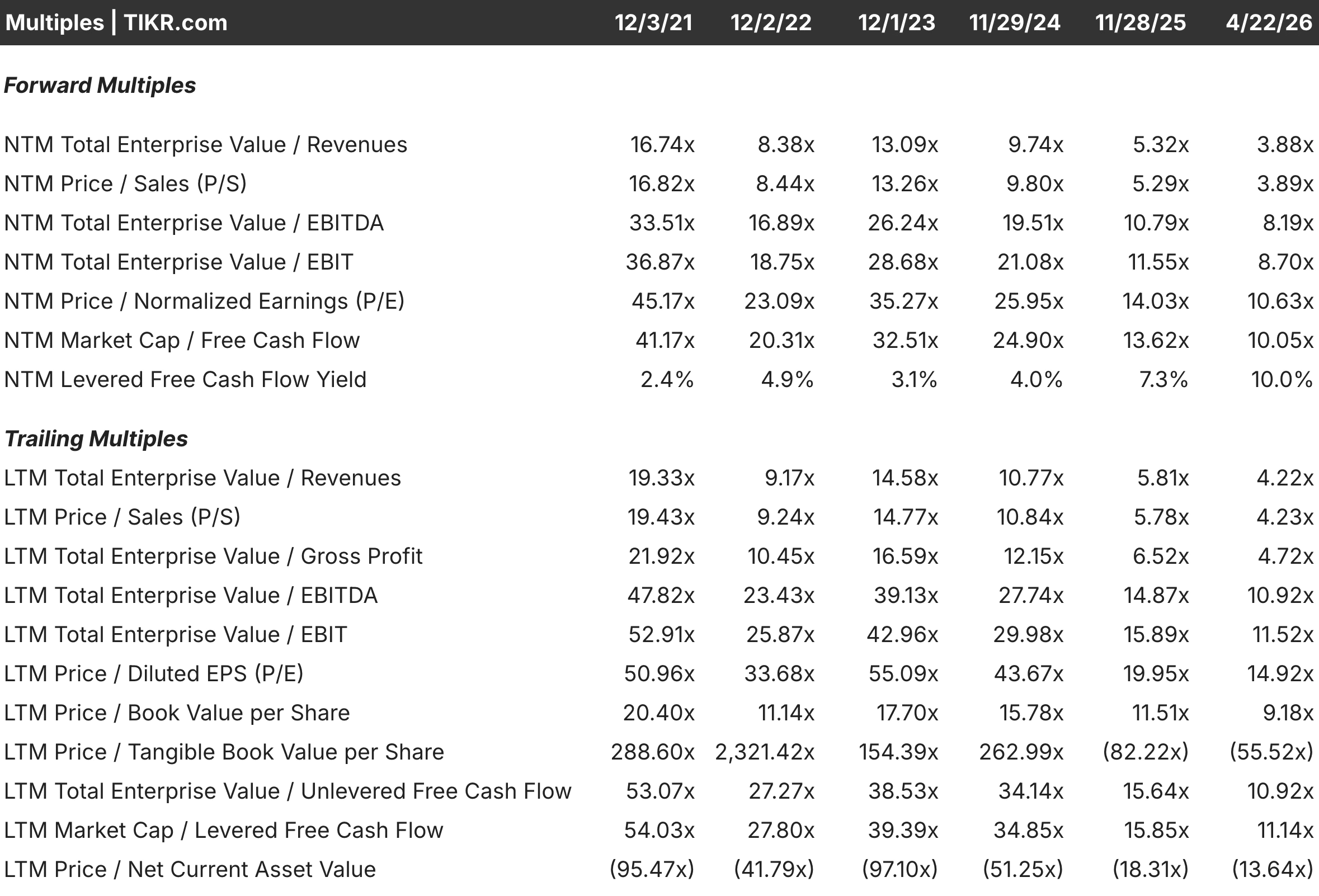

Sitting at approximately 11x forward P/E today, Adobe has not traded at this level since well before its subscription transition was complete. The NTM EV/EBITDA of roughly 8x and EV/FCF of around 10x are similarly compressed relative to the past five years, and neither reflects a business in fundamental decline.

Revenue grew from $12.9 billion in fiscal 2020 to $23.8 billion in fiscal 2025, with FCF margins recovering to 41% after a temporary dip during integration spending. The compression is entirely driven by AI disruption fears, specifically the concern that generative tools could erode demand for professional creative software over time.

That concern is real, but not yet showing up in the numbers. Generative AI features have been embedded across the product suite and are being monetized through higher-priced subscription tiers. Whether that monetization accelerates or gets disrupted is the central debate, and the current multiple suggests the market is pricing in a pessimistic outcome.

From 230x to 15x: Atlassian’s Valuation Has Returned to Earth

Few multiple compressions in software history have been as dramatic. Atlassian’s forward P/E peaked above 230x in fiscal 2021, when the stock was priced for decades of uninterrupted hypergrowth, and has since compressed to approximately 15x as cloud migration creates temporary margin headwinds and complicates revenue recognition.

The NTM EV/EBITDA of roughly 10x and EV/FCF around 10x still carry a modest premium to Adobe on some metrics, which requires justification given operating losses that Adobe simply does not have. The market’s answer is the growth rate. Revenue is expanding at roughly 22% annually versus Adobe’s 10%, and the completion of the cloud migration should unlock operating leverage that the current income statement does not yet reflect.

Paying 15x forward earnings for a company still operating at a loss is a bet on execution, not on current profitability. That distinction matters when sizing the position and setting expectations for the recovery timeline.

See what analysts think about TEAM stock right now (Free with TIKR) >>>

What the Consensus Numbers Are Pricing In Through 2030

Thirty-seven analysts covering the Adobe project expect fiscal 2026 revenue of approximately $26 billion, up roughly 10% year-over-year. The EPS consensus sits around $23.49, up approximately 12%. Looking further out, steady 9%-10% annual revenue growth is expected through 2030, with earnings expanding at a slightly faster pace while margins hold near current levels. High renewal rates and low churn give these estimates unusual visibility.

Thirty-one analysts covering Atlassian project fiscal 2026 revenue of approximately $6.4 billion, up roughly 22% year-over-year. The EPS consensus sits around $4.76, up approximately 29%. Revenue growth of 17% to 18% annually is projected through 2028 as the cloud migration tailwind compounds, though outer-year EPS estimates carry lower coverage and wider variance, reflecting genuine uncertainty about when profitability inflects meaningfully upward.

The contrast highlights the classic growth-versus-quality trade-off. Predictable numbers with less execution risk on one side. Faster growth with more uncertainty around the timing of margin recovery on the other.

See analysts’ full growth forecasts and estimates for ADBE stock (It’s free) >>>

The FCF Gap Is the Most Concrete Difference Between the Two

Adobe’s FCF margins have been consistently above 35% for several years, demonstrating that the subscription model is well-matured and that the incremental costs of serving additional users are minimal. With $23.8 billion in revenue and 41% FCF margins, cash generation is substantial, and funds are used for buybacks, dividends, and continued product investment without external financing.

Atlassian’s FCF margins recovered from a trough of around 24% in fiscal 2023 to approximately 27% in fiscal 2025 as revenue scaled. Operating margins remain negative, meaning reported earnings understate cash generation, but also confirm that the business still requires investment to reach the profitability profile implied by its valuation.

A successful cloud migration would materially improve Atlassian’s FCF picture. That recovery is the thesis. For Adobe, the cash is already there, which is why the valuation compression feels more clearly disconnected from what the business is actually producing.

What the Three-Year IRR Math Looks Like

For Adobe, the mid-case model targets an implied stock price of approximately $341 by November 2028, with cumulative dividends adding roughly $0.72 per share, bringing the total target value to approximately $342. That implies a total return of roughly 34% and an annualized return of approximately 12% over three years. The range between scenarios is relatively tight, reflecting the stability of Adobe’s revenue base and the consistency of its margin profile.

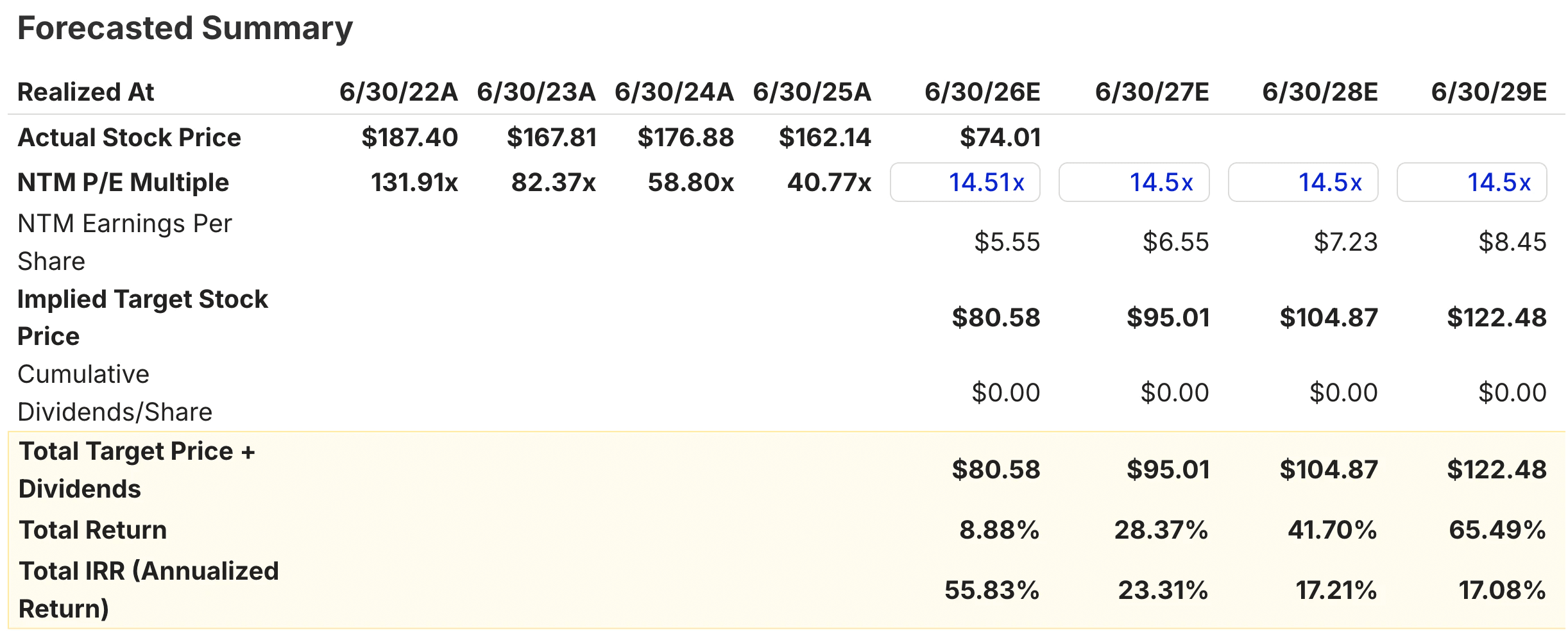

For Atlassian, the mid-case model targets an implied stock price of approximately $105 by June 2027, rising to approximately $122 by June 2029. The three-year total return through June 2028 implies approximately 42% upside, or roughly 17% annualized. A wider range of outcomes than Adobe’s reflects the execution risk around cloud migration completion and the timing of operating leverage materializing at scale.

The IRR difference is meaningful but not enormous. A more defensive path at slightly lower annualized returns on one side, and a modestly higher IRR with more variance on the other.

Build your own Valuation Model to value any stock (It’s free!) >>>

How Much Upside Does ADBE Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!