Key Stats for Marvell Stock

- 52-Week Range: $54 to $168

- Current Price: $166

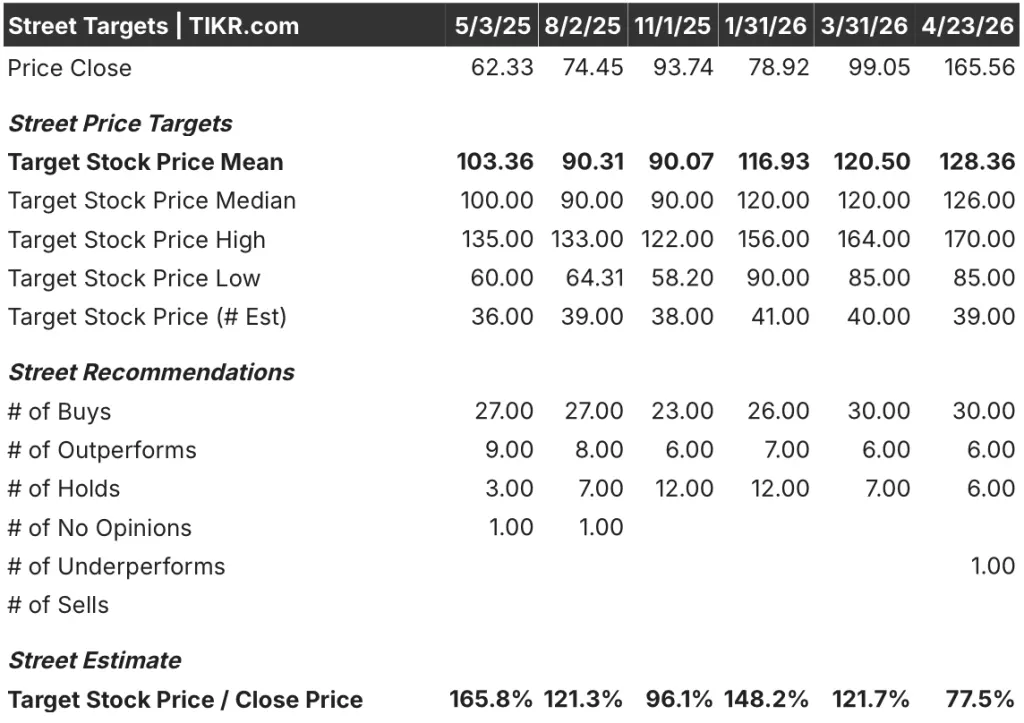

- Street Mean Target: $128

- Street High Target: $170

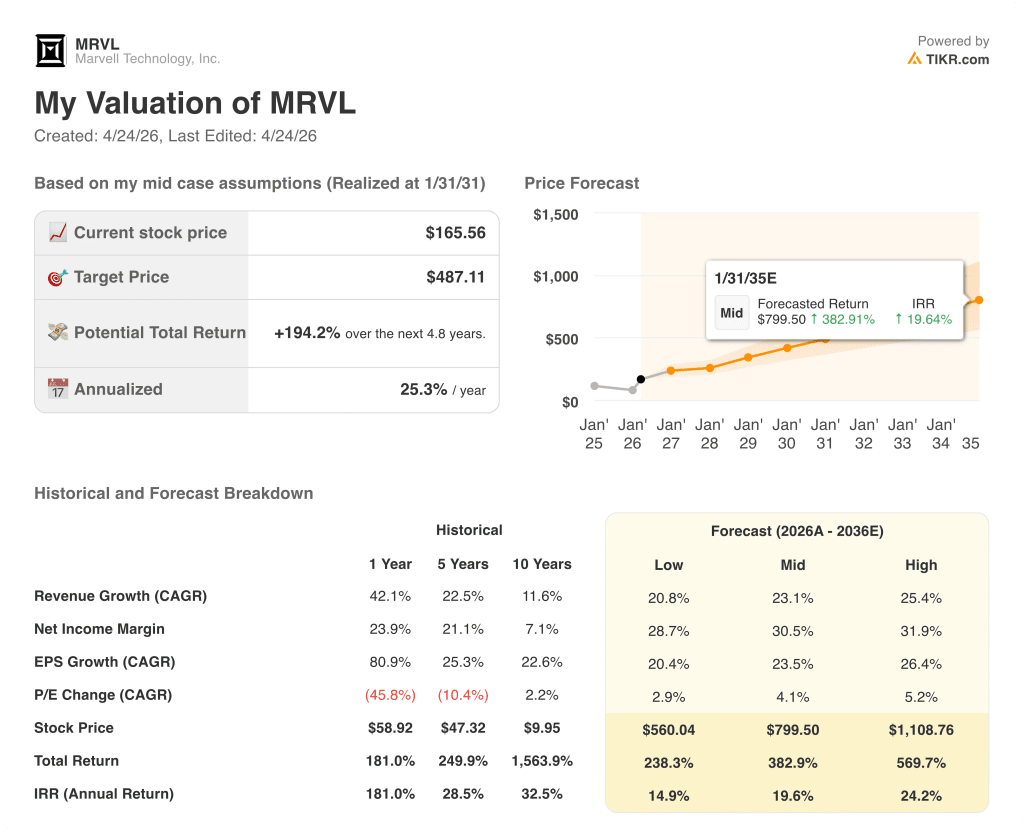

- TIKR Model Target (Jan. 2031): $487

What Happened?

Marvell Technology (MRVL), a semiconductor company specializing in data infrastructure chips for AI, cloud, and telecom networks, posted record quarterly revenue of $2.219 billion in Q4 fiscal 2026, with Marvell stock up over 40% year-to-date as analysts process what may be the most aggressive guidance revision cycle in the semiconductor sector this year.

That revision is the real story: management raised its fiscal 2027 revenue forecast to approximately $11 billion, up from $10 billion guided in December and $9.5 billion guided in September, a third consecutive multi-billion-dollar upward revision in under six months.

The data center segment is what keeps forcing the revisions higher, crossing $6 billion in fiscal 2026 revenue growing 46% year-over-year, with management now projecting 40% growth in fiscal 2027 and close to 50% in fiscal 2028, when total company revenue is expected to approach $15 billion.

On March 31, Nvidia announced a $2 billion equity investment in Marvell and a strategic partnership through NVLink Fusion, a networking architecture that lets Marvell’s custom chips interoperate directly with Nvidia’s AI factory ecosystem, validating Marvell’s platform positioning across the hyperscaler infrastructure stack.

Barclays separately upgraded Marvell stock to overweight on April 9, raising its price target to $150 and citing the optical networking business specifically, noting that optical ports should double in 2026 and double again in 2027, implying around 90% optical revenue growth for the company in each of the next two years.

On Q4 2026 earnings call, CEO Matthew Murphy stated, “We expect data center revenue in fiscal 2028 to grow close to 50% year-over-year,” anchoring the forward case to purchase orders already in place and a new Tier 1 hyperscaler XPU program entering high-volume production.

The three-year growth architecture rests on four product lines ramping simultaneously: optical interconnects scaling from 800G toward 1.6T, custom silicon (XPUs and XPU-attached chips) that doubled to $1.5 billion in fiscal 2026 and is projected to at least double again by fiscal 2028, data center Ethernet switching targeting over $600 million in fiscal 2027, and Celestial AI’s co-packaged optics (CPO) technology, a new acquisition projected to reach a $500 million annualized run rate by Q4 fiscal 2028.

Wall Street’s Take on MRVL Stock

The market has spent most of fiscal 2026 underestimating Marvell’s revenue trajectory, and the data strongly suggests it is doing so again with fiscal 2027 and fiscal 2028.

MRVL’s EBITDA is forecast to grow from $3.24 billion in fiscal 2026 to around $3.92 billion in fiscal 2027 and around $5.57 billion in fiscal 2028, a 42% two-year compound rate backed by the $11 billion revenue outlook and operating leverage that expanded EBITDA margins from 34% in fiscal 2025 to 40% in fiscal 2026, with continued expansion modeled as revenue scales faster than headcount.

Thirty of 39 analysts rate Marvell stock a buy, six rate it outperform, and six rate it hold, with one underperform; the mean price target sits at $128, implying roughly 23% downside from the current price, a structural disconnect that reflects consensus still anchored to guidance frames that management has already revised twice above.

The spread from $85 to $170 across the analyst range exposes the fault line directly: the low-end target is modeling something close to the September $9.5 billion framework, while the high end has partially incorporated the March $11 billion revision, and neither has yet priced in a scenario where the revision cadence continues into fiscal 2028.

With EBITDA compounding at over 40% annually over the next two fiscal years, consensus targets sitting more than 20% below where Marvell stock already trades, and three successive upward guidance revisions demonstrating that management’s early forecasts have consistently proven conservative, Marvell stock appears undervalued for investors underwriting the fiscal 2027 and 2028 revenue pathway against the current forward multiple.

The Nvidia $2 billion investment is the signal that shifts the framework: it confirms Marvell’s status as a platform supplier with ecosystem-level lock-in rather than a component vendor exposed to hyperscaler program risk, changing how customer concentration and program longevity should be modeled.

If the new Tier 1 XPU program slips in timing or CapEx growth moderates faster than assumed, the fiscal 2028 doubling thesis breaks at its foundation and estimates compress sharply across the board.

Fiscal Q1 fiscal 2027 guidance of $2.4 billion implies 27% year-over-year growth; the specific number to watch is whether data center sequential growth of around 10% holds and whether Murphy’s “record pace” bookings characterization is reiterated or softened on the next call.

What Does the Valuation Model Say?

TIKR’s mid-case model prices Marvell at $487, based on around 23% annualized revenue growth compounding through fiscal 2031 alongside net income margins expanding from 30.1% in fiscal 2026 toward around 30% to 32% — inputs anchored directly to management’s stated $15 billion fiscal 2028 revenue commitment and the 640-basis-point operating margin expansion already recorded in fiscal 2026.

Running at roughly a 25% annualized IRR, with three successive upward guidance revisions on record, a $2 billion Nvidia equity anchor, and custom silicon projecting to at least double by fiscal 2028, the current price of $165 leaves Marvell stock undervalued by any model that takes the $11 billion and $15 billion revenue frameworks at face value.

The investment case for MRVL hinges on a single question: does management deliver a fourth consecutive upward revision, or does the fiscal 2027 cadence prove the ceiling rather than another floor?

What Has to Go Right

- Fiscal 2027 data center revenue reaches the 40% growth target, with the interconnect business growing over 50% as guided, driven by 1.6T ramps across multiple Tier 1 hyperscalers

- The new Tier 1 hyperscaler XPU program ramps into high-volume production in fiscal 2028, contributing alongside the existing program that already doubled to $1.5 billion in fiscal 2026

- Celestial AI’s CPO technology hits its stated $500 million annualized run rate by Q4 fiscal 2028, validating the scale-up networking opportunity management projects at over $10 billion by 2030

- AEC and retimer revenue, already doubling in fiscal 2027 from a base of around $200 million, continues compounding as 1.6T upgrades pull through across all five major U.S. hyperscalers

- Non-GAAP OpEx growth remains in low-to-mid single digits per quarter in the second half of fiscal 2027, sustaining operating leverage toward the mid-to-high 30s operating margin range

What Could Go Wrong

- The analyst mean target of $128 is already 23% below current price, meaning even a credible bookings deceleration — not a miss, just a deceleration — reprices Marvell stock sharply against a valuation running well ahead of consensus

- The new Tier 1 XPU program remains in development with high-volume production not expected until fiscal 2028; any NPI delay or design pivot at the customer level compresses the doubling assumption at the model’s core

- Celestial AI and XConn add around $75 million in annual non-GAAP operating expenses before contributing meaningful fiscal 2027 revenue, creating near-term earnings drag that the current forward multiple is already absorbing

- Gross debt-to-EBITDA of 1.38x alongside the newly priced $1 billion in 5.3% senior notes due 2036 adds balance sheet load at the exact moment Marvell needs supply chain flexibility for its largest ramp cycle

- If hyperscaler CapEx growth moderates faster than currently assumed, the close-to-50% fiscal 2028 data center growth rate that anchors the $15 billion target compresses from the top line down, and the TIKR $487 mid-case unravels at its first assumption

Should You Invest in Marvell Technology, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up MRVL stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Marvell Technology, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MRVL stock on TIKR for Free →