Key Stats for Salesforce Stock

- 52-Week Range: $164 to $296

- Current Price: $190

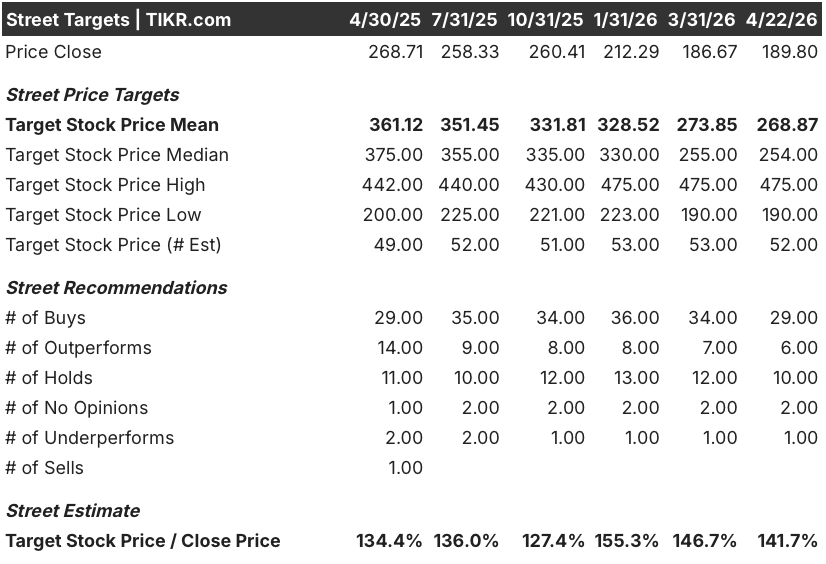

- Street Mean Target: $269

- Street High Target: $475

- Analyst Consensus: 29 Buys, 6 Outperforms, 10 Holds, 1 Underperform

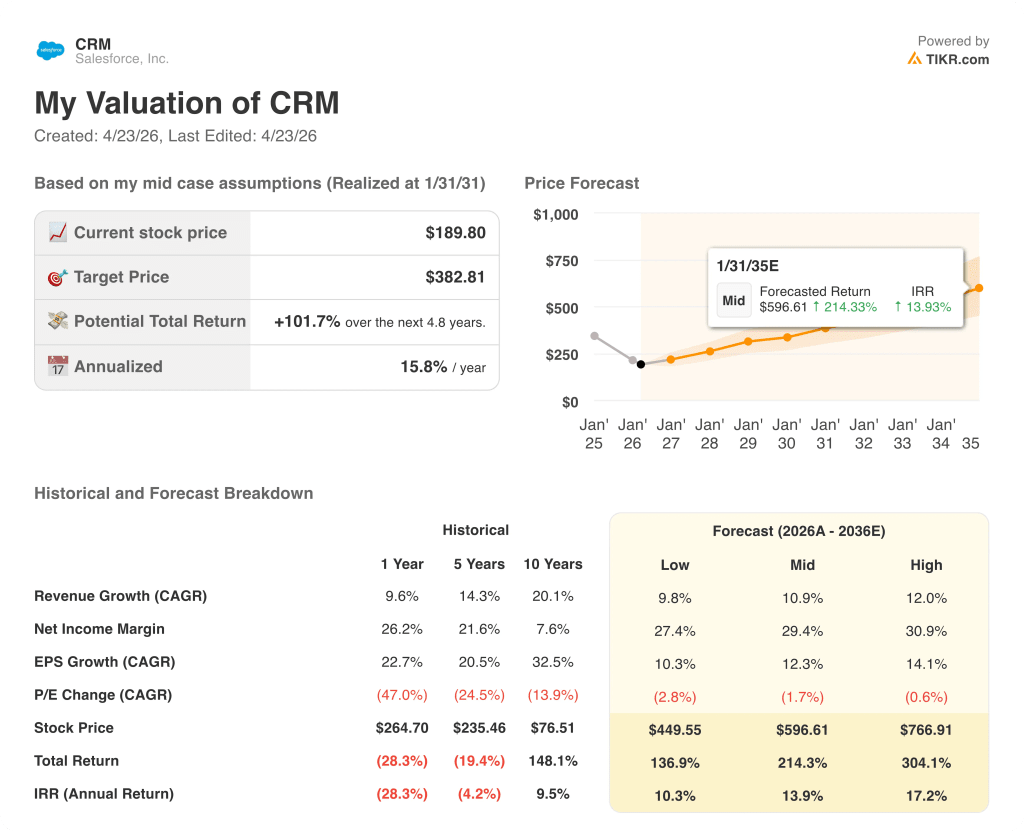

- TIKR Model Target (Dec. 2030): $383

What Happened?

Salesforce (CRM), the world’s largest customer relationship management platform, is trading near its 52-week low of $164 even as its AI agent product just crossed $800 million in annual recurring revenue, growing 169% year-over-year.

That product, Agentforce, a platform that deploys autonomous AI agents across enterprise sales, service, and marketing workflows without human intervention, closed 29,000 deals in its first 15 months, up 50% quarter-over-quarter.

Every single one of Salesforce’s top 10 Q4 wins included Agentforce, with deals over $10 million growing 33% year-over-year and cRPO (current remaining performance obligation, a measure of near-term contracted revenue) rising to $35.1 billion, up 16%.

CEO Marc Benioff stated on the Q4 FY2026 earnings call that “we are one of the largest consumers of tokens in the world to date, now over 19 trillion tokens,” underscoring that Agentforce has moved from pilot deployments into enterprise-grade production scale.

Salesforce paired that AI momentum with the most aggressive capital return in its history: a $50 billion share repurchase authorization funded by a $25 billion bond offering, with the company having already returned 99% of its free cash flow to shareholders in FY2026.

The U.S. Army awarded Salesforce a 10-year indefinite delivery contract with a $5.6 billion ceiling, a government-sector win that validates Agentforce beyond commercial enterprise and into regulated institutional workflows.

Wall Street’s Take on CRM Stock

The SaaSpocalypse narrative, the sector-wide fear that AI tools will automate away the workflows that SaaS companies charge for, is being directly contradicted by Salesforce’s own production data.

Agentforce and Data 360 combined annual recurring revenue reached $2.9 billion in FY2026, up 200% year-over-year, with more than 60% of those bookings coming from existing customers expanding their commitments rather than from new logo additions.

Thirty-five analysts currently rate Salesforce stock a buy or outperform, against 10 holds and just one underperform, with a mean price target of $269, implying roughly 42% upside from current levels as the Street waits for organic revenue re-acceleration to show in reported numbers.

The target spread tells a story in itself: the high sits at $475 and the low at $190, a $285 range reflecting a genuine structural debate between bears who see seat-based revenue under existential pressure from agent-driven automation and bulls who see Agentforce as a 2x to 4x revenue-per-customer multiplier based on early enterprise deployments already in production.

Priced at roughly $190, trading just 16% above its 52-week low while delivering $41.5 billion in FY2026 revenue and $2.9 billion in Agentforce ARR at triple-digit growth, Salesforce stock appears undervalued as the market prices in a disruption scenario that the company’s own booking data, 29,000 Agentforce deals and counting, does not support.

Management’s decision to authorize $50 billion in buybacks and fund it with debt at these prices is not standard treasury operations; it is a direct statement from the people with the most complete view of the business that the current discount relative to intrinsic value is real and actionable.

If LLM token costs fail to decline as Agentforce scales, gross margin compression could stall the operating leverage story that underpins the entire bull case for CRM.

Q1 FY2027 revenue, guided at $11.03 billion to $11.08 billion, is the first hard data point that will confirm or challenge management’s forecast of organic growth re-acceleration in the second half of the fiscal year: watch whether subscription and support revenue growth exceeds 12% year-over-year.

What Does the Valuation Model Say?

TIKR’s mid-case model targets Salesforce stock at $383, driven by an 11% revenue CAGR through FY2030 and net income margins expanding toward 29%, assumptions the company has already directionally confirmed with its own raised FY2030 revenue framework of $63 billion and a 200-basis-point operating margin expansion already delivered in FY2026.

The model’s extended scenario puts CRM at $597 by FY2035 on a 14% annualized return, and even the low case of $450 represents a 137% total return from current levels, with all three paths anchored to revenue growth in the 10% to 12% range that management has explicitly guided and backed with a $72 billion total RPO base.

At $190 with a $383 mid-case target sitting 102% above the current price, Salesforce stock is undervalued against a company that generated $41.5 billion in FY2026 revenue, closed 29,000 Agentforce deals in 15 months, and is buying back its own shares at these prices with the conviction of a $50 billion authorization.

The single thing the argument hinges on is whether Agentforce’s 169% ARR growth rate represents a durable new revenue layer or a temporary adoption surge that stalls once the initial enterprise rollout wave clears.

Bull Case

- Agentforce ARR crossed $800 million growing 169% year-over-year and represents less than 2% of FY2026 revenue, with penetration still below 30% of the 23,000-plus active Agentforce customer base, leaving the majority of the addressable expansion untouched

- The $50 billion buyback, funded at a price near the 52-week low of $163.52 with final settlement expected in Q3 or Q4 of FY2027, will compress the float materially, accelerating per-share metrics even at modest top-line growth

- Early enterprise deployments are producing 2x to 4x spending expansion per customer as organizations layer Data 360, Tableau, and MuleSoft onto Agentforce foundations, a dynamic already visible in 7 of the top 10 Q4 deals

- The U.S. Army’s 10-year IDIQ contract with a $5.6 billion ceiling adds a durable government revenue channel that scales through procurement cycles rather than annual software renewals

Bear Case

- Organic cRPO growth was 9% in Q4 when the 4-point Informatica contribution is excluded, a deceleration that sits well below the 16% headline and raises questions about the underlying momentum heading into FY2027

- The $25 billion bond offering introduces meaningful leverage to a balance sheet that previously carried minimal debt, leaving the company more exposed to any revenue shortfall in a fiscal year where management has staked its credibility on a second-half acceleration

- Weakness in Marketing Cloud, Commerce Cloud, and Tableau was explicitly flagged in Q4 guidance as an ongoing headwind, and those segments represent a substantial portion of the installed base that Agentforce alone cannot immediately offset

- The seat-based model underlying the majority of Salesforce revenue faces structural pressure if Agentforce agents begin replacing human users at scale before consumption-based pricing fully compensates, a transition whose timing and magnitude remain genuinely uncertain

Should You Invest in Salesforce, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CRM stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Salesforce, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CRM stock on TIKR for Free →