Key Stats: CVS Health (CVS)

- Current price: ~$76

- Full year 2025 revenue: over $400B

- Full year 2025 adjusted EPS: $6.75

- Q4 2025 revenue: $105.1B (+8.4% YoY)

- Q4 2025 adjusted EPS: $1.09

- 2026 revenue guidance: at least $400B

- 2026 adjusted EPS guidance: $7–$7.2

- TIKR model price target: ~$125

- Implied upside: ~63%

CVS Health Q4 2025 Earnings Breakdown

CVS Health stock (CVS) delivered $105.1B in Q4 2025 revenue, an 8.4% increase year over year, capping a full year in which the company generated over $400B in revenue and $6.75 in adjusted EPS.

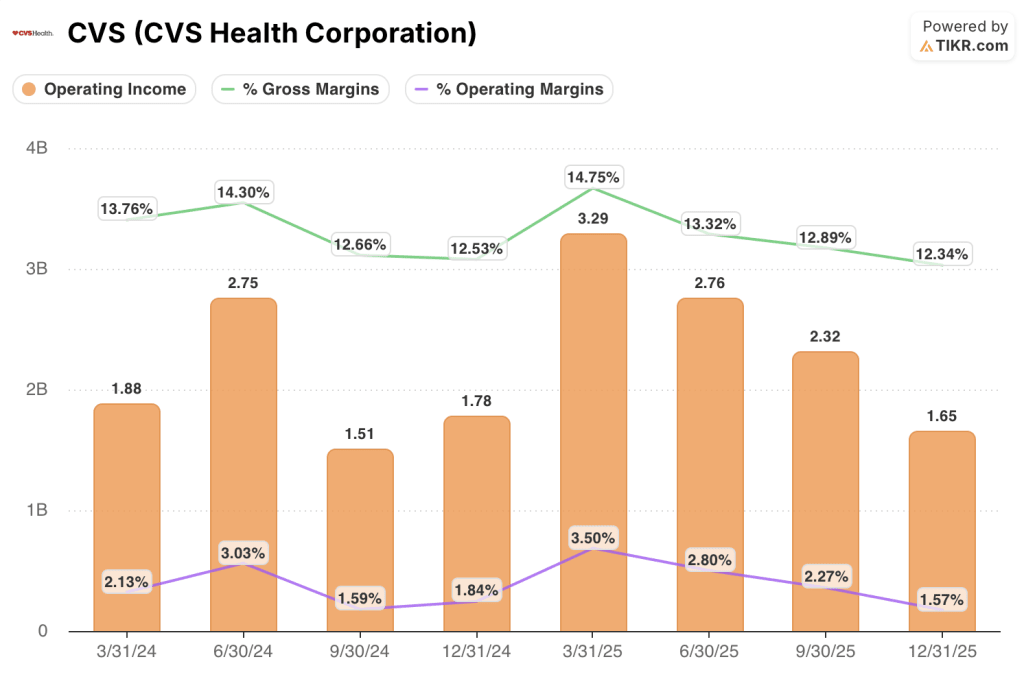

Adjusted EPS for the quarter came in at $1.09, while adjusted operating income reached approximately $2.6B.

The Pharmacy & Consumer Wellness segment was the standout driver, posting nearly $38B in revenue for the quarter, up over 12% year over year.

Same-store pharmacy sales grew over 19% in Q4, supported by a nearly 10% increase in same-store prescription volumes.

Script share reached over 29% in the quarter, with the Rite Aid asset acquisition providing incremental volume on top of organic market share gains.

The Health Services segment generated over $51B in Q4 revenue, up 9% year over year, with adjusted operating income growing over 9% to approximately $1.9B, driven by improved purchasing economics.

Health Care Benefits generated over $36B in Q4 revenue, a 10% year-over-year increase, but posted an adjusted operating loss of $676M in the quarter.

The loss in Health Care Benefits was driven primarily by changes in Medicare Part D seasonality under the Inflation Reduction Act, along with a deterioration in the Individual Exchange risk adjustment position and a provision for elevated flu activity late in the quarter.

For the full year, the Aetna segment delivered a year-over-year adjusted operating income improvement of over $2.6B, according to CEO David Joyner on the Q4 earnings call.

CVS Health reaffirmed its 2026 adjusted EPS guidance range of $7.00 to $7.20 and confirmed revenue guidance of at least $400B for the year.

Operating cash flow for full year 2025 came in at $10.6B, exceeding initial expectations, and the company distributed over $3B in dividends to shareholders during the year.

CVS Health Stock: Financials

The Q4 2025 income statement tells a story of revenue momentum running ahead of margin delivery, with operating leverage compressed at the consolidated level by the Health Care Benefits drag.

Gross margin came in at 12.3% for Q4 2025, down from 12.5% in Q4 2024 and well below the 14.8% posted in Q1 2025, reflecting segment mix and ongoing reimbursement dynamics across the pharmacy businesses.

Operating income for Q4 2025 was $1.65B, a 7.2% decline year over year while operating margin contracted to 1.6% in Q4 2025, down from 1.8% in Q4 2024.

The full margin trajectory across 2025 was uneven: operating margin peaked at 3.5% in Q1, compressed through mid-year to 2.3% in Q3, then fell to 1.6% in Q4 as Health Care Benefits seasonality and reserve charges weighed on the consolidated result.

CVS Health Stock Valuation Model Take

The TIKR model prices CVS Health stock at approximately $125, implying roughly 63% upside from the current price near $76.

The mid-case assumptions underlying that target include a revenue CAGR of 4.2% and a net income margin of 2.6%, which is a meaningful step up from the 1.8% net income margin CVS delivered over the trailing one-year period.

The Q4 result reinforces that CVS Health stock has a credible earnings recovery path: Aetna posted over $2.6B in full-year AOI improvement, the pharmacy business stabilized under CostVantage, and full-year EPS guidance was reaffirmed and stepped higher for 2026.

The investment case is incrementally stronger after Q4, but the margin expansion embedded in the TIKR model still requires Aetna to continue recovering toward target margins across 2026 and 2027, which is not yet fully de-risked.

The investment thesis on CVS Health stock hinges on whether Aetna’s margin recovery holds its trajectory against a still-elevated medical cost trend and an adverse 2027 Medicare Advantage rate notice.

What Has to Go Right

- Aetna delivered over $2.6B in year-over-year AOI improvement in 2025 and management reaffirmed the path to target margins, with Medicare, Medicaid, and Commercial all expected to show further improvement or stability in 2026

- The Pharmacy & Consumer Wellness segment established a baseline of at least flat annual earnings going forward, with the completed CostVantage transition and over 29% script share removing a multiyear structural drag on consolidated results

- The PBM’s TrueCost model is positioned as a natural alignment with incoming PBM legislation, with management citing over $6B in net new revenue onboarded for 2026 at a retention rate above 98%

- The TIKR mid-case model requires only a 4.2% revenue CAGR and a 2.6% net income margin to reach approximately $125, thresholds that look achievable if Aetna executes even modestly on its stated recovery arc

What Could Still Go Wrong

- The proposed 2027 Medicare Advantage rate notice was described by management as failing to match current medical cost trends, and any adverse final rate decision could slow the margin recovery timeline at Aetna

- Full-year 2025 consolidated operating margin never exceeded 3.5% in any single quarter, and the Q4 figure of 1.6% highlights how exposed CVS Health stock remains to Health Care Benefits seasonality and reserve charges

- Management guided 2026 operating cash flow to at least $9B, a step down from the $10.6B delivered in 2025, partly reflecting the pull-forward of certain payments that benefited last year’s figure

- Gross margin compressed from 14.8% in Q1 2025 to 12.3% by Q4, and the TIKR model’s 2.6% net income margin assumption requires a reversal of that trend that has not yet materialized at scale

Should You Invest in CVS Health Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CVS stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CVS Health Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CVS stock on TIKR for Free →