Key Takeaways:

- GE Aerospace reported a strong start to 2026, with Q1 adjusted EPS of $1.86, adjusted revenue up 29%, and orders up 87%, but the stock fell as investors focused on oil, fuel availability, and slower airline activity assumptions instead of the earnings beat.

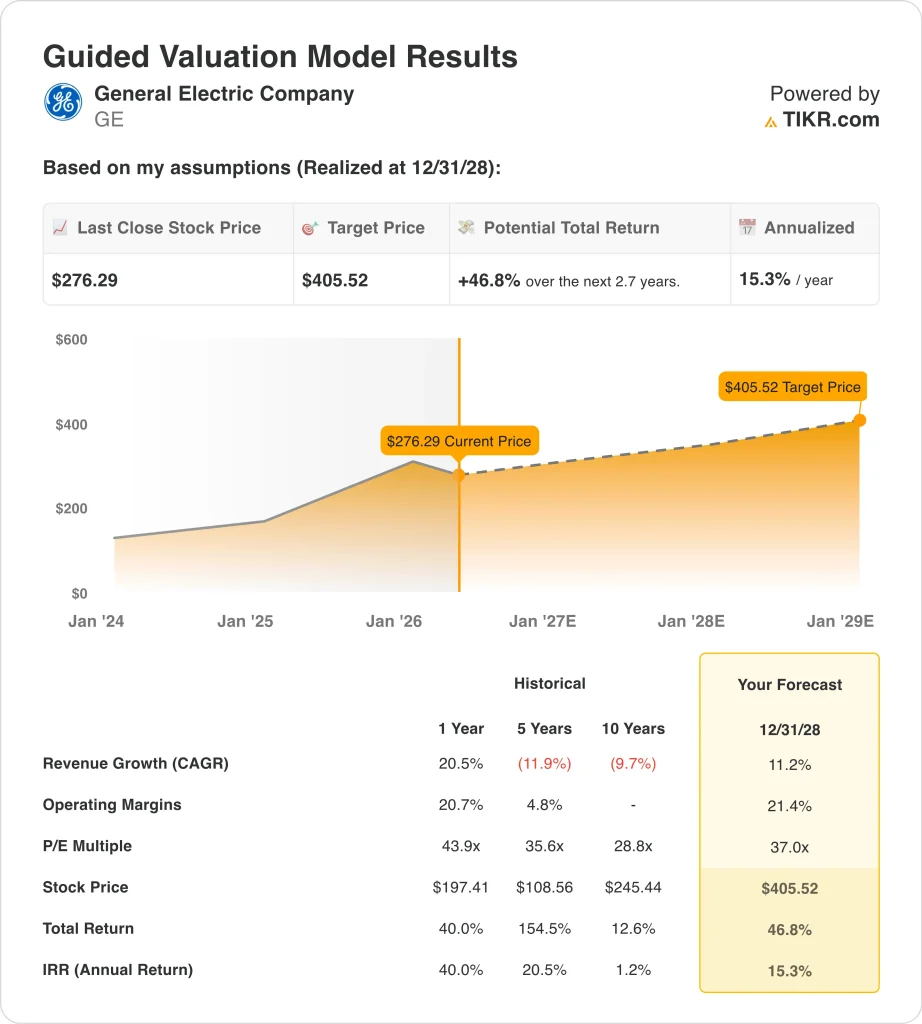

- GE stock could rise from $276 to about $406 per share based on around 11% annual revenue growth, a ~21% operating margin, and a 37x P/E multiple.

- That implies a 46.8% total return, or a 15.3% annualized return, over the next 2.7 years.

What Happened?

General Electric (GE) moved into focus this week after reporting first-quarter 2026 results that beat expectations on revenue and profit, while management kept full-year guidance unchanged and said results are trending toward the high end of the range.

The market reaction was more complicated than the headline numbers. Reuters reported that GE shares fell as investors focused on rising oil prices, fuel supply constraints, and a weaker outlook for global departures tied to the Iran war and broader geopolitical uncertainty.

General Electric now assumes flat to low-single-digit flight departure growth in 2026, down from a prior mid-single-digit view, and that matters because more flying typically drives more engine wear, spare-parts demand, and shop visits.

Management’s tone helps explain why the stock traded this way. Larry Culp said, “GE Aerospace had a strong first quarter with orders growing 87% and revenue up 29%,” but he also said the company kept guidance in place because of the “dynamic geopolitical landscape.”

Even so, the business backdrop is not weak. General Electric said its commercial services backlog is over $170 billion, the total backlog is above $210 billion, and demand for spare parts still exceeds supply.

Reuters also noted that delayed aircraft deliveries from Boeing and Airbus are helping keep older fleets in service longer, which supports aftermarket engine revenue for companies like GE and Safran.

Here’s why GE stock could remain highly sensitive from here: investors are weighing a very strong engine-and-services cycle against a macro shock that could slow airline activity before it slows GE’s earnings.

What the Model Says for GE Stock

We analyzed the upside potential for General Electric stock using valuation assumptions based on its strong installed engine base, commercial services backlog, defense exposure, and improving earnings profile.

Based on estimates of around 11% annual revenue growth, a ~21% operating margin, and a normalized P/E multiple of 37x, the model projects GE stock could rise from $276 to about $406 per share.

That would be a 46.8% total return, or a 15.3% annualized return, over the next 2.7 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for GE stock:

1. Revenue Growth: 11%

GE’s revenue base has been rising sharply. Using the financial data provided, total revenue rose from $35.3 billion in 2023 to $38.7 billion in 2024 and $45.9 billion in 2025, with LTM revenue at $48.3 billion. That shows the post-spin aerospace business is scaling faster and with a cleaner mix.

The most recent quarter supports that direction. GE reported Q1 adjusted revenue up 29%, helped by 39% growth in Commercial Engines & Services revenue and double-digit growth in Defense & Propulsion Technologies. Orders rose 87%, and management said the total backlog is now above $210 billion, giving the company unusually strong visibility for an industrial business.

The growth assumption is also tied to what actually drives the business. More engine shop visits, higher spare-parts demand, and rising installed-base utilization are all favorable, while delayed aircraft deliveries can keep older fleets flying longer and extend maintenance demand.

Based on analysts’ consensus estimates, we use around 11% annual revenue growth because GE is still benefiting from a strong aerospace cycle, even as management turns more cautious on flight departures.

2. Operating Margins: 21%

GE’s margin profile has improved materially over the last several years. Using the financial data provided, operating margin moved from -0.1% in 2021 to 13.7% in 2022, 17.7% in 2023, 20.0% in 2024, and 20.7% in 2025, with LTM operating margin at 20.3%. That kind of improvement usually signals better mix, stronger pricing, and more disciplined execution.

The latest quarter showed both strength and some limits. GE posted a 21.8% operating profit margin in Q1 2026, but that was down 200 basis points year over year as higher install-engine growth, investments, and inflation offset the benefits of price and services volume.

In Commercial Engines & Services, profit still rose 23%, which shows the service model remains very attractive even when margins do not expand every quarter.

Margin durability matters because it tells investors whether revenue growth is turning into real earnings power. GE’s services business is the key driver here, since spare parts and maintenance generally carry better economics than equipment.

Based on analysts’ consensus estimates, we use an operating margin of around 21% because current profitability already supports that range, but the assumption still leaves room for inflation, mix pressure, and incremental investment.

3. Exit P/E Multiple: 37x

The valuation model uses a 37x P/E multiple, which is high in absolute terms but not random. GE’s LTM P/E in the overview data is about 34x, while the guided valuation framework uses 37x in the forecast. That means the model is not assuming a dramatic rerating from current levels.

There are fundamental reasons the market is willing to pay a premium multiple. GE now has a more focused aerospace profile, a large recurring services stream, a commercial services backlog above $170 billion, and a total backlog above $210 billion.

The company also continues to reduce share count, with diluted shares falling from 1.094 billion in 2024 to 1.068 billion in 2025 and 1.062 billion on an LTM basis, which supports per-share earnings growth.

The multiple still depends on execution. If growth slows faster than expected, or if airline stress causes investors to question the durability of aftermarket demand, the market could assign a lower earnings multiple even if profits keep rising.

Based on analysts’ consensus estimates, we use a 37x exit P/E because it broadly matches the current quality premium investors are already assigning to GE’s aerospace cash flows.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for GE stock over the next decade show varied outcomes based on commercial aerospace demand, margin execution, and valuation discipline (these are estimates, not guaranteed returns):

- Low Case: Airline demand softens, fuel costs remain elevated, and GE’s valuation multiple contracts faster than earnings grow → 8.0% annual returns

- Mid Case: GE continues converting backlog into revenue, services demand stays firm, and margins remain near current levels → 11.2% annual returns

- High Case: Commercial aerospace demand stays strong, defense orders expand, and investors continue assigning GE a premium multiple → 14.1% annual returns

The stock’s next move will probably depend less on whether GE can beat a quarter and more on whether investors regain confidence in the second-half airline backdrop.

If fuel pressure eases and departure trends stabilize, the market may refocus on backlog, services, and cash flow. If oil stays high and airline caution spreads, GE could keep trading like a strong business facing a tougher macro tape.

See what analysts think about GE stock right now (Free with TIKR) >>>

Should You Invest in General Electric Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up GE, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track GE alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze General Electric stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!