Key Takeaways:

- Tesla delivered 358,023 vehicles in Q1 2026, down around 13% year over year, and is trading at roughly 191x forward earnings, a multiple that only makes sense if you believe the autonomy and robotics narrative plays out at scale.

- Rivian reaffirmed full-year 2026 delivery guidance of 62,000 to 67,000 vehicles, a target that requires deliveries to nearly double from Q1 levels over the remaining three quarters, hinging almost entirely on the R2 ramp in the back half of the year.

- Analyst price targets sit close to current prices for both stocks. The more interesting question is what assumptions are buried inside those targets and whether either company can actually get there.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Both stocks have had a rough stretch. Tesla (TSLA) is down sharply from its late 2024 highs, despite the stock more than doubling over the past year amid optimism about Elon Musk and enthusiasm for autonomy. Rivian (RIVN) has stabilized after years of painful dilution and delivery shortfalls, trading around $17, with Wall Street’s consensus target barely above its current price.

The comparison is unusual because these companies are not at the same stage. Tesla is the dominant EV manufacturer in the world and is now also pitching itself as an AI and robotics company. Rivian is a startup that has not turned a profit, is burning cash, and is betting its future on a mid-size SUV that has not yet hit the market.

Putting them side by side is useful precisely because of that asymmetry, because it forces you to think clearly about what kind of risk you are actually taking on with each.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Two Different Revenue Engines

Tesla sells mass-market electric vehicles, led by the Model 3 and Model Y, which together account for over 96% of quarterly delivery volume. But the Tesla investment thesis in 2026 is not really about those cars. It is about Full Self-Driving, the Robotaxi program currently in unsupervised testing in Austin, and Optimus, the humanoid robot Elon Musk has described as potentially the most valuable product the company has ever built.

Energy storage, which includes the Powerwall for homes and the Megapack for utilities, generated over $10 billion in annualized revenue in 2025 and is one of the fastest-growing segments.

The stock trades on all of those narratives simultaneously, which is why it trades at a 191x forward P/E despite a trailing EBIT margin of only 4.6%.

Rivian sells premium electric trucks and SUVs, primarily the R1T pickup and R1S SUV, targeting buyers who want an adventure-capable electric vehicle and are willing to pay for it. The company also has a commercial delivery van contract with Amazon, which provides some baseline volume.

Rivian is still pre-profit at scale, with a trailing gross margin of only 2.7% and an EBIT margin of around -67%. The entire investment case rests on whether the R2, a more affordable mid-size SUV priced from $45,000, can ramp up fast enough to achieve sustainable unit economics.

What the Estimate Tab Shows

The TIKR Estimates tab reveals just how different the growth trajectories look for each company, and more importantly, how different the confidence intervals are.

For Tesla, analysts expect revenue of around $102 billion in 2026, growing by around 8%, followed by around $120 billion in 2027 as delivery volumes recover and energy storage continues to scale. The EPS consensus sits around $2.03 for 2026, rising to around $2.75 in 2027, with earnings acceleration expected to come from margin recovery as the vehicle mix improves and FSD subscription revenue grows.

The challenge is that, at 191x forward earnings, even that earnings-growth trajectory implies years of flawless execution before the valuation becomes conventionally defensible.

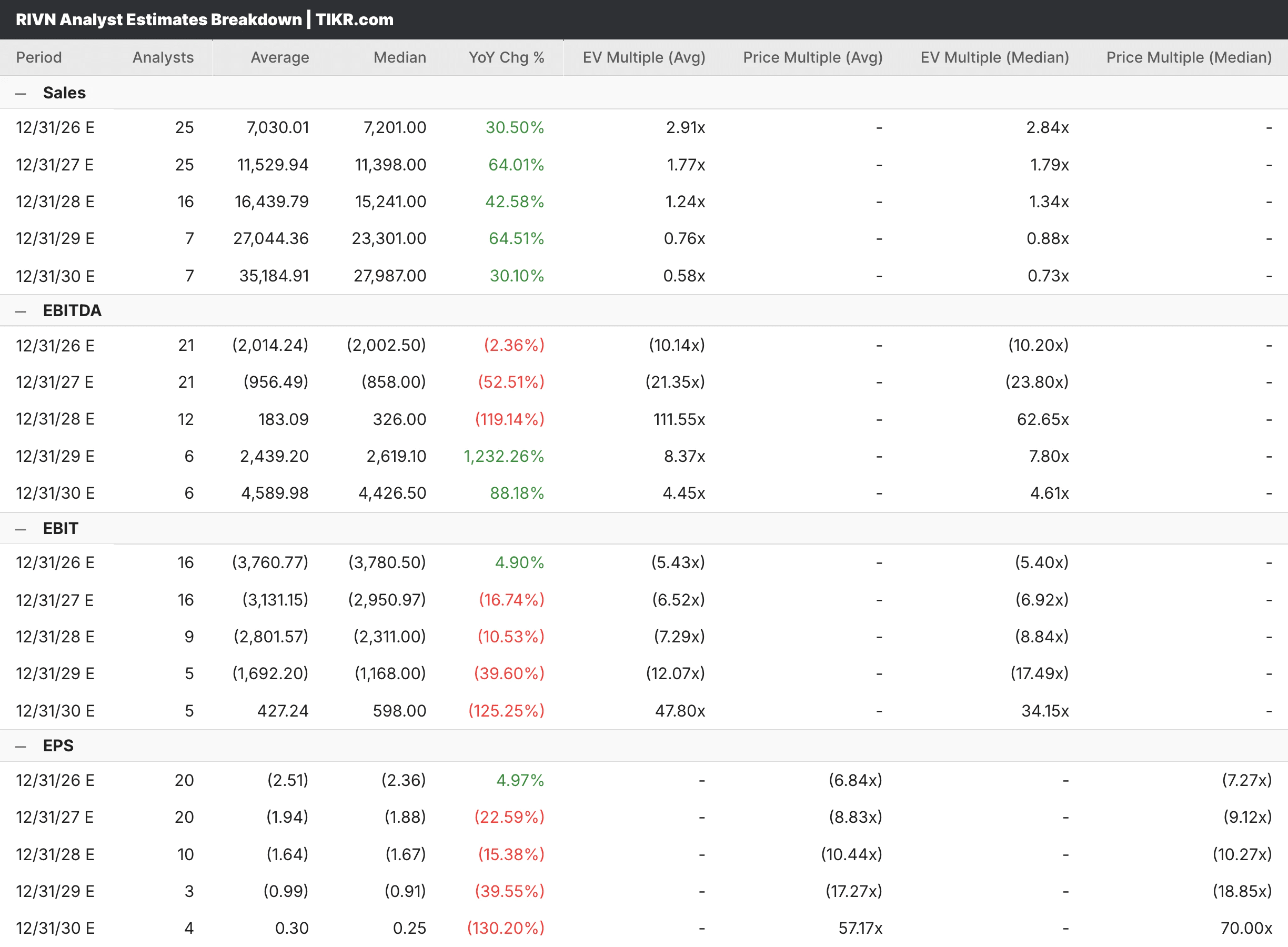

For Rivian, the revenue picture is more dramatic in terms of growth rate. Analysts expect revenue of around $7 billion in 2026, growing around 30%, then nearly doubling again to around $11.5 billion in 2027 as R2 volumes build. EPS remains deeply negative through at least 2027, with consensus around negative $2.51 in 2026 and negative $1.94 in 2027, meaning this is entirely a story about whether the path to profitability arrives before the company runs out of runway to get there.

The Street consensus price target is around $18, barely above today’s price, suggesting Wall Street sees the setup as balanced rather than compelling at current levels.

Forward Valuations: Different Frameworks for Different Companies

Traditional P/E is the right starting point for Tesla, even if the number itself is difficult to work with. At roughly 191x forward earnings, the stock is priced for an outcome that assumes dramatic margin expansion, autonomous-driving revenue, and Optimus contributing meaningfully to earnings over the next several years. The NTM EV/Revenue multiple of roughly 14x reflects a similar premium.

For Rivian, P/E simply does not apply to a company losing money, so EV/Revenue is the more useful lens. On that basis, Rivian trades at around 2.9x forward revenue, which is actually modest for a company expected to grow revenue by 30% this year and 64% the year after.

The question is not whether the multiple is reasonable but whether the growth actually materializes, and that depends almost entirely on the R2 launch going smoothly in the back half of 2026.

See what analysts think about TSLA stock right now (Free with TIKR) >>>

What the TIKR Models Say

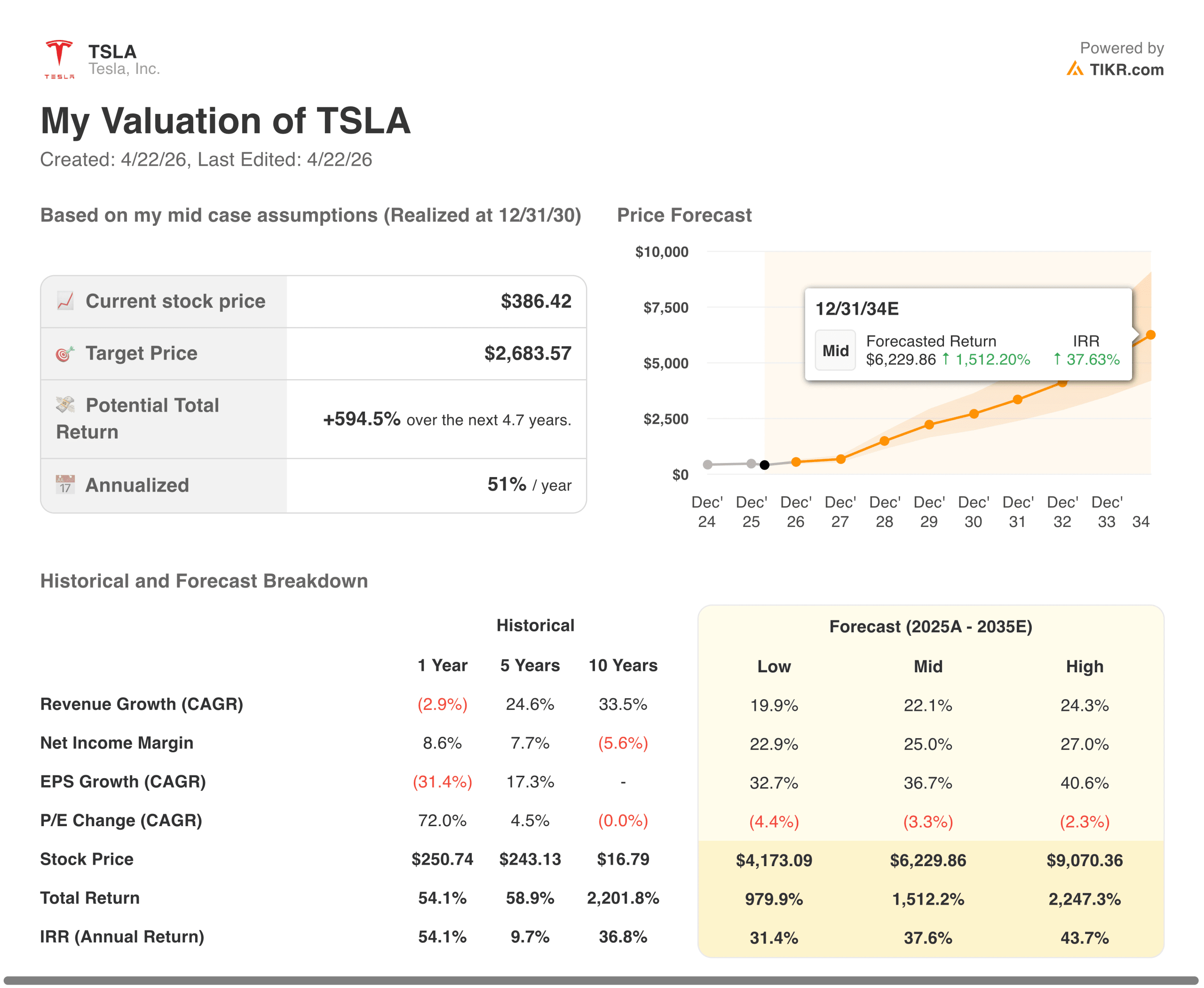

The TIKR model for Tesla targets around $2,680, implying roughly 595% upside from current levels and an annualized return of about 51% over the next several years.

That number will look shocking until you understand what is embedded in it: the mid case assumes around 22% annual revenue growth through 2035 and net income margins expanding toward 25%, essentially pricing in Tesla successfully monetizing autonomy and energy at scale. If you believe that scenario is plausible, the return math is extraordinary. If you think it is too optimistic, the current stock price already prices in a great deal of good news.

The TIKR model for Rivian is one of the more sobering outputs you will see on the platform. The mid-case target is actually negative, reflecting a scenario where the company continues burning cash, the R2 ramp comes in below what is needed to sustain the business, and the stock essentially goes to zero before profitability arrives.

The model’s annualized return is just above 1%, implying that the base case for Rivian at current prices is a poor risk-adjusted outcome. The high case, which requires the aggressive revenue growth consensus to fully materialize, gets you to a better place, but the distance between the base and the high case is unusually wide.

See analysts’ full growth forecasts and estimates for RIVN stock (It’s free) >>>

The Bottom Line for Investors

Tesla and Rivian are not really comparable as investments because they are not comparable as businesses. Tesla is a bet on whether the most ambitious technology roadmap in the auto industry actually delivers, priced at a premium that assumes it does. Rivian is a bet on survival and eventual scale, priced at a level where the base case in the TIKR model does not even cover your principal.

What they share is high risk and high sensitivity to execution. Tesla needs its autonomy timeline to hold and its margins to recover as delivery volumes rebuild. Rivian needs the R2 to launch cleanly, ramp quickly, and prove that the unit economics improve enough to stop the cash burn before the balance sheet becomes a problem.

Neither is a position for someone seeking safety. Tesla at least has a profitable core business beneath the narrative, which provides some floor. Rivian does not have that yet, and the TIKR model is clear-eyed about what that means for the probable range of outcomes.

Build your own Valuation Model to value any stock (It’s free!) >>>

How Much Upside Does TSLA Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!