Key Stats for ServiceNow Stock

- Current Price: $102.71

- Target Price (Mid): ~$220

- Street Target: ~$165

- Potential Total Return: ~120%

- Annualized IRR: ~18% / year

- 52-Week High / Low: $211.48 / $81.24

- Max Drawdown: (60.28%) on 4/10/26

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

ServiceNow (NOW) has shed roughly a third of its value in 2026, and investors are split on whether the damage reflects a real structural threat or a sector-wide overreaction.

Bulls argue the platform is built to monetize AI adoption. Bears say the valuation still has room to fall as AI-native tools squeeze enterprise software budgets.

The year started badly. In late January, ServiceNow reported strong Q4 2025 results, with subscription revenue of $3.47 billion growing 21% year over year and cRPO (current remaining performance obligations, meaning contracted revenue due in the next 12 months) rising 25% to $12.85 billion, per the company’s Q4 2025 earnings release.

The stock still fell 11.44% on results day, per TIKR, because investors were already focused on whether AI agents would pressure the software pricing model. The broader rout deepened in February when the S&P 500 Software and Services Index fell as much as 17% in six sessions after Anthropic launched agentic AI plugins, triggering fears that traditional SaaS products could be made obsolete.

On April 10, shares fell nearly 8% in a single session as a ceasefire breakdown in the Middle East drove risk-off selling while Anthropic’s expanding AI agent presence simultaneously weighed on software sentiment.

That session marked a 60.28% drawdown from ServiceNow’s all-time highs, per TIKR. The stock has since recovered to around $102.

CEO Bill McDermott has been direct in pushing back on the AI disruption narrative. In February, he purchased $3 million in ServiceNow shares using personal funds.

On the Q4 2025 earnings call, McDermott argued that AI without workflow orchestration delivers no real enterprise value, positioning ServiceNow as the layer where AI actually gets work done rather than a legacy platform under threat.

The company also disclosed that half of its new business revenue now comes from non-seat-based models, including AI token consumption, decoupling its growth from the headcount reductions AI enables at customers.

See historical and forward estimates for ServiceNow stock (It’s free!) >>>

Is ServiceNow Undervalued Today?

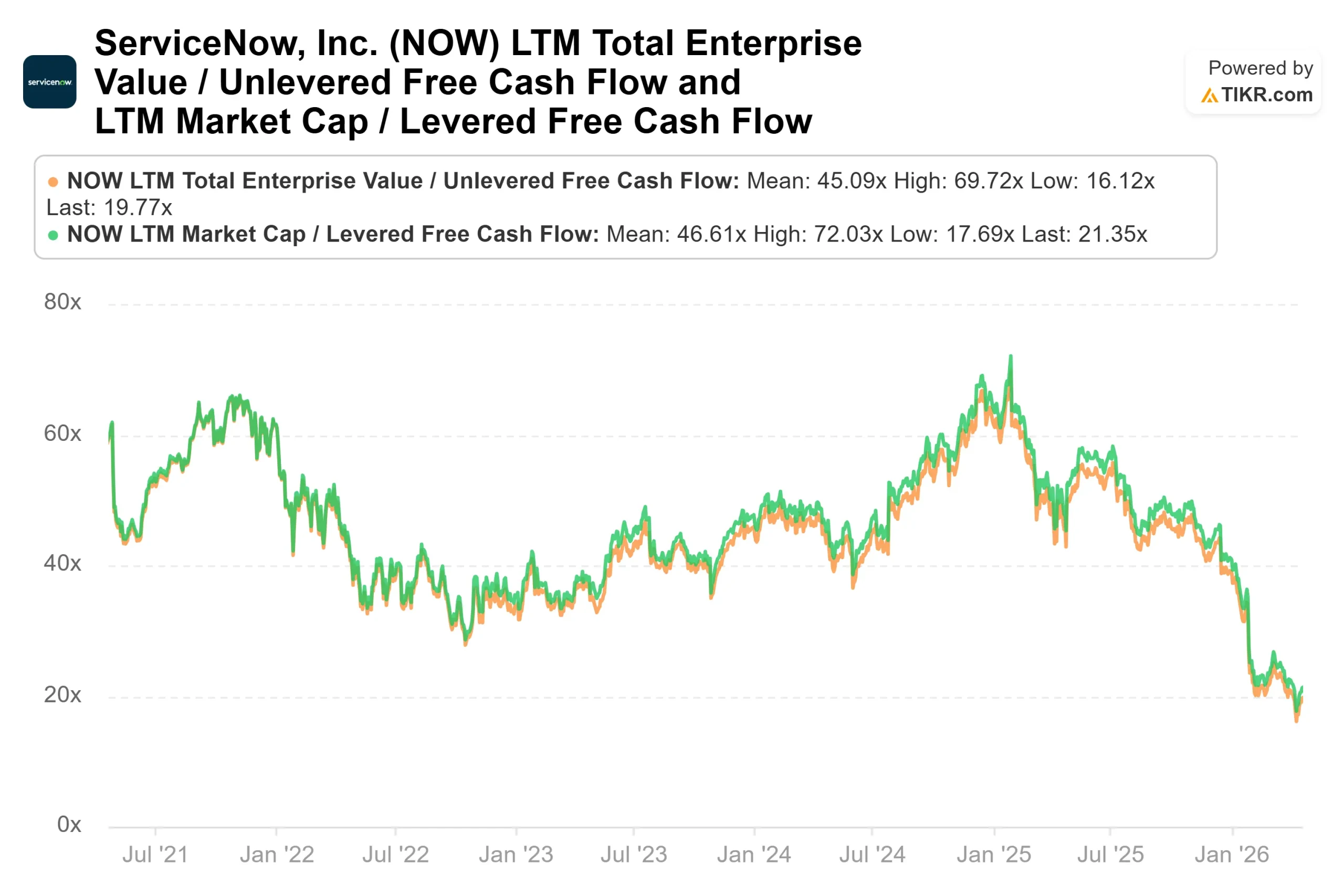

A year ago, investors were paying nearly 34x NTM EV/EBITDA for ServiceNow. Today, multiple sits at 16.77x, per TIKR, roughly a 50% compression while the business kept growing revenue at around 21% per year.

Put simply, the stock got about twice as cheap while the company barely slowed down.

The comparison to peers makes that compression look starker. Salesforce (CRM), which is growing revenue at roughly half ServiceNow’s pace, still trades at 8.86x NTM EV/EBITDA. Microsoft (MSFT) trades at 24.13x NTM P/E versus ServiceNow’s 23.91x, per TIKR’s Competitors page.

The market is now pricing ServiceNow at nearly the same earnings multiple as Microsoft despite the company growing revenue considerably faster.

The free cash flow picture reinforces this. ServiceNow generated $4.86 billion in LTM free cash flow, putting the stock at roughly 21x LTM FCF against a market cap of around $104 billion, per TIKR. That is a level that does not reflect a business growing revenue at a near-20% pace.

The bear case is structural and worth taking seriously. ServiceNow’s traditional growth engine is adding seats as enterprise customers grow their employee count. As AI lets those same customers do more with fewer people, that model faces direct pressure.

McDermott’s token consumption pivot is the direct response, but it is still early, and the market wants proof that the model works at scale.

What gives the bull case near-term teeth is today’s Q1 print. Per the Q4 2025 earnings call, ServiceNow guided Q1 subscription revenues of $3.65 to $3.655 billion, with cRPO growth of 20% in constant currency, though with a 150-basis-point headwind from a mix shift toward hosted hyperscaler offerings.

The company is also targeting over $1 billion in Now Assist ACV (annual contract value for its AI agent suite) in 2026, up from a doubling trajectory exiting Q4. A beat on both lines today would directly challenge the AI disruption thesis.

The $5 billion share repurchase authorization from January 2026, including a planned $2 billion accelerated buyback, signals that management views the current price as a significant undervaluation.

The Knowledge 2026 conference on May 5-7 in Las Vegas adds a second potential catalyst, where ServiceNow is expected to showcase its full AI platform expansion following the $2.85 billion Moveworks acquisition completed in December 2025.

See how ServiceNow performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $102.71

- Target Price (Mid): ~$220

- Potential Total Return: ~120%

- Annualized IRR: ~18% / year

See analysts’ growth forecasts and price targets for ServiceNow stock (It’s free!) >>>

The TIKR mid-case model projects ServiceNow reaching around $220 by December 31, 2030, roughly 120% total return from the April 22 entry price of $100.14, or around 18% per year. Two drivers underpin the revenue CAGR of around 17% through 2030: Now Assist and AI token consumption growth, and continued enterprise platform expansion into security and HR from ServiceNow’s IT service management core. Net income margin expands to around 29% by 2030 as operating leverage builds on the subscription base, per TIKR estimates.

The upside risk is AI consumption monetization accelerating faster than modeled, which lifts the high case to around $391 per share by December 2034 at roughly 21% annualized. The downside risk is that the seat-based headwind proves larger than expected and integration costs from Moveworks, Armis, and Veza compress margins. Even in the low case, the model projects positive returns through 2030, supported by a net cash position of $7.65 billion and a 98% renewal rate, per ServiceNow’s Q4 2025 earnings release.

Conclusion

The metric to watch tonight is subscription revenue against the $3.65 to $3.655 billion guidance range, paired with cRPO growth versus the 20% constant-currency target. A beat on both, with Now Assist ACV tracking toward the $1 billion 2026 target, shifts the narrative from disruption to opportunity.

ServiceNow is a free cash flow-compounding platform priced near its lowest valuation multiples in years. What management says tonight will determine whether Q1 2026 marks the turning point.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in ServiceNow?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ServiceNow, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track ServiceNow alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze ServiceNow on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!