Key Stats for Arista Networks Stock

- 52-Week Range: $72 to $178

- Current Price: $178

- Street Mean Target: $179

- Street High Target: $220

- Analyst Consensus: 21 Buys, 6 Outperforms, 3 Holds

- TIKR Model Target (Dec. 2030): $325

What Happened?

Arista Networks (ANET), the pure-play networking company powering AI and cloud data centers with its industry-leading EOS (Extensible Operating System) software stack, has nearly tripled from its 52-week low of $72 to touch $178, fueled by a fundamental demand inflection in AI infrastructure.

On February 12, Arista reported Q4 2025 revenue of $2.49 billion, up 28.9% year-over-year, beating estimates by over $100 million, and raised its 2026 full-year revenue outlook to approximately $11.25 billion, representing 25% annual growth.

Arista simultaneously doubled its AI networking revenue target from $1.5 billion in 2025 to $3.25 billion for 2026, a figure underpinned by all four of its large AI customers actively deploying Ethernet-based clusters, with three already exceeding 100,000 GPU connections.

On April 7, Rosenblatt Securities upgraded Arista Networks stock to “buy” from “neutral”, raising its price target to $180 and citing XPO (eXtra-dense pluggable optics, Arista’s new AI data center interconnect standard delivering 4x density improvement over prior-generation optics) as a meaningful differentiator.

Jayshree Ullal, Chairperson and CEO, stated on the Q4 2025 earnings call that “with our ever-increasing AI momentum, we anticipate a diversified customer base in 2026, including one, maybe even 2 additional 10% customers,” pointing to a demand profile that is broadening rather than concentrating.

Arista Networks stock is positioned to compound through three reinforcing growth engines over the next three to five years: AI center networking scaling toward a $3.25 billion annual target, a cognitive campus and branch initiative targeting $1.25 billion by year-end 2026, and a software and subscription layer now contributing 17% of revenue with 3,000 cumulative CloudVision (Arista’s centralized network management platform) customers.

Wall Street’s Take on ANET Stock

Arista beating Q4 estimates by $106 million and raising 2026 guidance to $11.25 billion converts a narrative about AI potential into a documented demand backlog, shifting the forward earnings debate from “if” to “how fast.”

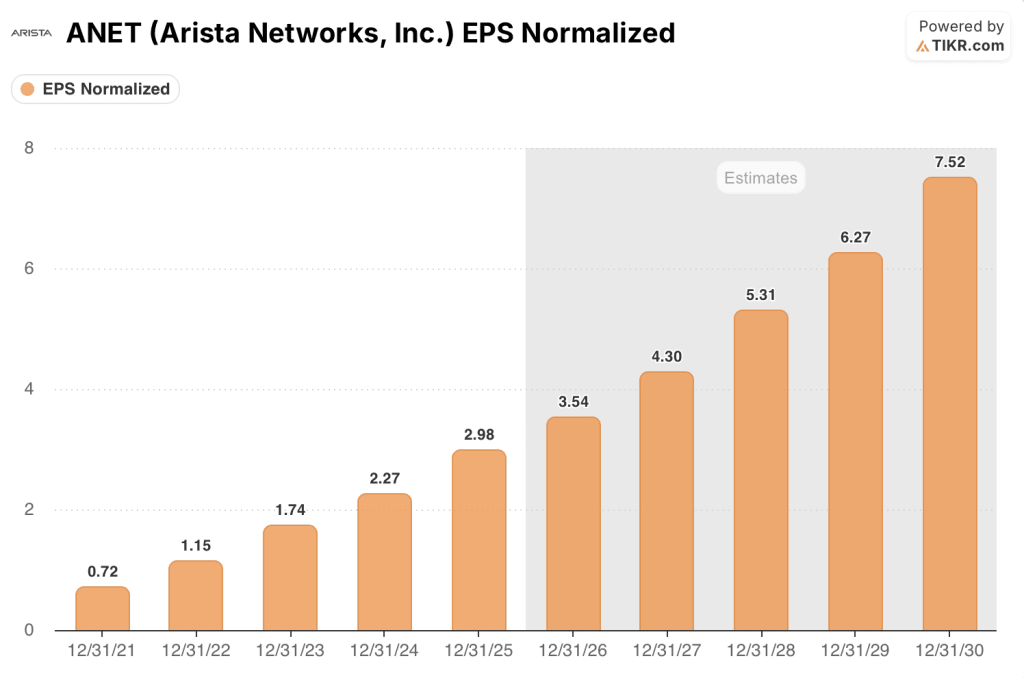

ANET’s normalized EPS grew 28.4% in 2025 to $2.98, and backed by the $3.25 billion AI networking target, consensus now projects around $3.54 for 2026, with growth re-accelerating toward around $4.30 in 2027 as campus and AI revenue scale together.

Twenty-seven of 30 analysts covering Arista Networks stock rate it buy or outperform, with a mean price target of around $179, essentially in line with the current price; the Street is not waiting for a discount here, it is positioned for execution on the $11.25 billion 2026 guide.

Target spreads from $140 to $220 reflect a genuine debate: bears anchor to memory cost inflation compressing margins below the 62% floor, while bulls at $220 are pricing in one or two new 10% customers materializing by year-end and full recognition of the $3.25 billion AI networking target.

Trading at roughly 50x forward 2026 earnings against a consensus EPS growth rate decelerating from 31% to around 19%, Arista Networks stock appears fairly valued as the multiple tracks historical levels while the growth rate normalizes, leaving limited room for multiple expansion without an upside earnings surprise.

Memory cost inflation has worsened materially into 2026, and if gross margins compress below the 62% floor, the operating leverage story that underpins the $3.54 EPS estimate breaks down.

Q1 2026 results on May 5 will reveal whether Arista can convert $2.6 billion in guided revenue while holding the 62-63% gross margin range; any confirmation of a new 10% customer would change the valuation math immediately.

What Does the Valuation Model Say?

The TIKR model’s mid-case target of $325 per share over the next 4.7 years assumes a revenue CAGR of around 17% and a net income margin of around 40%, inputs grounded in Arista’s 2025 actual margins of 42.3% and the $11.25 billion 2026 guide that management has raised twice in six months.

At around 13.7% annualized returns to reach $325 in the mid case, with the low-case floor at $370 implying a double from current prices over the same horizon, ANET is fairly valued at today’s price when framed against near-term earnings, but the TIKR model suggests the medium-term compounding case remains compelling for patient capital.

The entire argument for owning Arista Networks stock at $178 rests on a single question: can the $3.25 billion AI networking target prove conservative rather than aspirational, and can margins hold above 62% while memory costs escalate?

What Has to Go Right

- AI networking revenue reaches or exceeds the $3.25 billion 2026 target as all four large AI customers scale past 100,000 GPU deployments and at least one new 10% customer is confirmed by year-end.

- Gross margin holds within the 62-64% guided range despite memory cost headwinds, preserving the operating leverage that drives consensus EPS of around $3.54 for 2026.

- Campus revenue reaches the $1.25 billion 2026 target, with VeloCloud (the SD-WAN provider acquired in July 2025) integration accelerating enterprise attach rates and widening the addressable market beyond hyperscalers.

- The XPO optics MSA, debuted at OFC 2026 with 12.8 Tbps capacity and 4x density improvement over prior-generation optics, drives design wins in AI data center scale-across deployments where Arista has less incumbent competition.

What Could Go Wrong

- Memory supply constraints worsen beyond management’s current purchase commitments, forcing gross margins below the 62% floor and breaking the EPS model that justifies a 50x forward multiple.

- Deferred product revenue of $5.4 billion as of Q4 2025 does not convert as expected, delaying recognized revenue into 2027 and creating a muted 2026 growth print relative to the $11.25 billion guide.

- One or more of the four large AI customers pauses deployment timelines due to power or permitting constraints, reducing the $3.25 billion AI networking target and triggering analyst downgrades.

- The ESUN Ethernet scale-up specification, expected to finalize in Q4 2026, slips into 2027, leaving InfiniBand competitors holding scale-up network positions longer than anticipated.

Should You Invest in Arista Networks, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ANET stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Arista Networks, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ANET stock on TIKR for Free →