Key Stats for Upstart Holdings Stock

- 52-Week Range: $24 to $87

- Current Price: $35

- Street Mean Target: $44

- Street High Target: $80

- TIKR Model Target (Dec. 2030): $181

What Happened?

Upstart Holdings (UPST), the AI-powered lending marketplace that matches borrowers with banks and credit unions across personal, auto, and home loan products, crossed $1 billion in annual revenue for the first time in 2025 while Upstart stock traded near its 52-week low of $23.97.

The stock’s most structurally significant development came on March 10, when Upstart announced it would apply to the OCC and FDIC to establish Upstart Bank, N.A., an insured national bank, and simultaneously apply to the Federal Reserve to become a bank holding company.

BTIG upgraded Upstart stock to “buy” from “neutral” on March 17, setting a $43 price target and arguing that the bank charter application directly addresses what the firm considered the single most important downside risk: Upstart’s exposure to private credit funding availability during a liquidity crisis.

The Q4 earnings report, which preceded the charter announcement, showed the depth of the business recovery: total originations grew 52% year-over-year, net income flipped from negative $2.8 million a year earlier to positive $19 million, and full-year adjusted EBITDA expanded from $11 million in 2024 to $230 million.

Dave Girouard, Co-Founder and outgoing CEO, stated on the Q4 earnings call that “we grew originations by 86% and revenues by 64% while growing headcount just 18%, a ratio any business would die for, and we reestablished Upstart as a strongly profitable business,” the first time Upstart has described itself in those terms since the post-COVID funding collapse of 2022 and 2023.

Upstart also announced April 22 that it had secured a $1.2 billion, 24-month forward-flow agreement with Centerbridge Partners to purchase consumer loans originated on the Upstart platform, the latest in a series of large committed capital arrangements that also included a $1 billion agreement with Eltura Ventures and Aperture Investors in March and a $200 million auto finance deal with Wafra in February.

Looking forward, management guided 2026 revenue to approximately $1.4 billion, a 35% increase, and projected a 35% compound annual growth rate in a macro-neutral environment through 2028, by which point the company expects adjusted EBITDA margins of approximately 25%.

Wall Street’s Take on UPST Stock

The bank charter application changes the risk profile of UPST stock at a structural level: deposit funding would replace reliance on private credit markets during periods of stress, addressing the exact vulnerability that contributed to Upstart’s 2022 funding collapse and the Model 22 underwriting disruption in late 2025.

UPST’s normalized EPS inflected from ($0.56) in 2023 through ($0.20) in 2024 to $1.89 in 2025, a recovery driven by the 86% growth in origination volume, operating leverage that held fixed cost growth to 5% against 64% revenue growth, and the maturation of auto and HELOC funding partnerships that reduced on-balance sheet loan exposure by 20% in Q4 alone; consensus now expects EPS to reach around $2 in 2026 and approximately $3 in 2027, growth rates of around 21% and around 40% respectively.

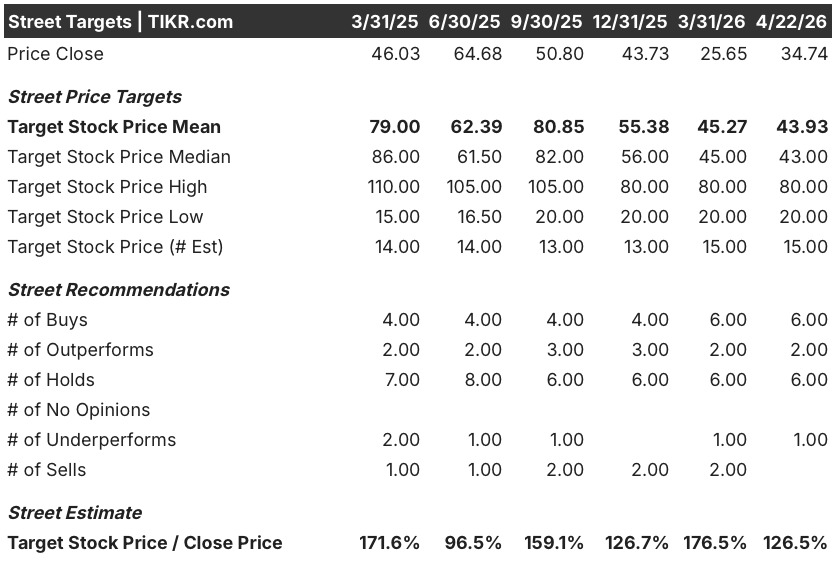

Eight of 15 analysts covering Upstart stock rate it “buy” or “outperform,” with 6 “holds” and 1 “underperform,” and the mean price target of $43.93 implies roughly 26% upside from current levels, a figure that does not yet fully reflect the optionality introduced by the bank charter application.

The target range spans from $20 on the low end to $80 on the high end, a spread that reflects genuine disagreement about whether Upstart’s funding model is permanently de-risked or still exposed to private credit cycle volatility, a question the bank charter application is specifically designed to answer.

Trading at roughly 15x 2026 consensus EPS estimates of around $2 while guiding to a 35% revenue CAGR through 2028 and with normalized EPS forecast to roughly double from 2025 to 2027, Upstart stock appears undervalued against a profitability recovery that the current multiple has not caught up with.

The bank charter itself is a signal worth isolating: BTIG’s upgrade framing explicitly called the charter a solution to private credit exposure risk, and a charter approval would give Upstart access to deposit funding, a materially lower-cost capital source than institutional credit funds.

If origination volumes soften meaningfully in 2026 and the UMI (Upstart Macro Index), the company’s proprietary measure of consumer credit risk, rises above its current 1.4-to-1.5 range, the contribution margin compression that management has already flagged would deepen faster than the operating leverage build can offset.

Q1 2026 origination volumes, which the company now publishes monthly, are the first number to watch: management guided for a seasonally soft Q1 and expects acceleration through the year, so any deviation from that pattern would immediately reprice the 2026 revenue guide.

What Does the Valuation Model Say?

TIKR’s mid-case model, anchored to around 21% revenue CAGR through 2030 and net income margins expanding toward roughly 34%, produces a price target of around $280 by December 2030, implying an annualized return of approximately 27% from current levels.

A forward P/E of roughly 15x on a business guiding to 35% revenue growth, expanding EBITDA margins, and a newly disclosed path to deposit-funded capital leaves Upstart stock appearing undervalued: the gap between the current multiple and the business’s stated growth trajectory is wider than at any point in the company’s profitable history.

The central question for Upstart stock is not whether the company’s AI lending model works. The data shows it does. The question is whether the funding architecture is resilient enough to sustain high origination volumes through the next credit cycle.

Bull Case

- The $1.2B Centerbridge deal, $1B Eltura/Aperture agreement, and $200M Wafra auto arrangement represent over $2.4 billion in committed forward-flow capital signed in 2026 alone, reducing near-term funding reliance on spot markets.

- A bank charter approval would give Upstart access to FDIC-insured deposits, converting the most significant structural risk in the bear case into a competitive advantage that peers cannot easily replicate.

- Auto originations grew 340% year-over-year in Q4 and 56% sequentially, with 70% of Q4 funding coming from third parties; management expects new secured product fee revenue to exceed $100 million in 2026.

- Management’s 35% CAGR target through 2028 implies roughly $2.5 billion in annual revenue by 2028, and the company grew headcount only 18% against 64% revenue growth in 2025, showing operating leverage is already compressing the fixed cost base.

Bear Case

- Model 22 underwriting errors in Q3 2025 reduced borrower approvals and triggered a securities fraud investigation by the Pomerantz Law Firm, and a repeat model failure in a tightening credit environment could erode capital partner confidence at a critical juncture.

- Contribution margins declined to 53% in Q4 from 57% the prior quarter, and management expects further compression as Upstart deliberately prices toward customer lifetime value rather than upfront take rate, creating a margin trajectory that may lag the revenue narrative longer than consensus expects.

- The UMI held at approximately 1.4-to-1.5 throughout 2025, but Upstart’s 2025 results surpassed its 2021 peak despite borrowers being statistically 43% more likely to default at current UMI levels than in 2021; any sustained rise in the UMI would compress both approval rates and contribution economics simultaneously.

- The bank charter application is subject to OCC, FDIC, and Federal Reserve approval with no committed timeline, leaving the most structurally important catalyst entirely outside management’s control.

Should You Invest in Upstart Holdings, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up UPST stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Upstart Holdings, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze UPST stock on TIKR for Free →