Key Stats for Fabrinet Stock

- Past-30-Day Performance: 26%

- 52-Week Range: $190 to $732

- Valuation Model Target Price: around $840

- Implied Upside: about 20%

Analyze your favorite stocks like Fabrinet with TIKR (It’s free) >>>

What Happened?

Fabrinet stock rose about 26% over the past 30 days, recently trading near $686 per share, as investors leaned into one of the market’s biggest themes right now: the rapid buildout of AI data centers that require faster and more complex optical networking hardware. This reflects a broader shift across AI infrastructure, where demand for connectivity between servers is becoming just as important as computing power itself.

The stock moved higher primarily because Fabrinet delivered record earnings and showed that AI-related demand remains strong, which led investors to reprice the company as a key supplier to next-generation data center infrastructure.

At the same time, the stock has started to stabilize in recent sessions as much of the near-term upside has already been priced in following the sharp run, with investors waiting for the next catalyst to push shares higher.

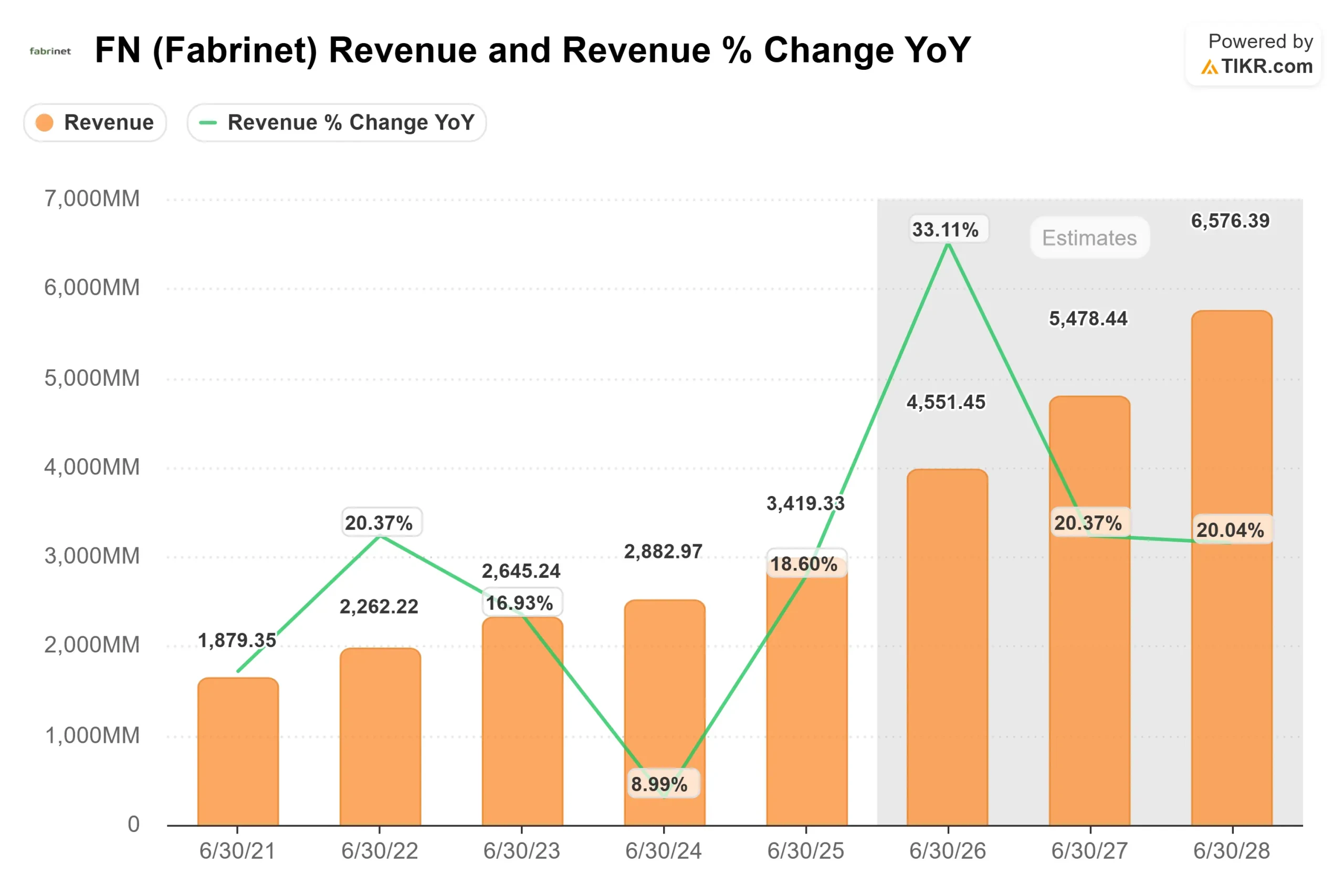

The company reported revenue of $1.13 billion, up 36% year over year and 16% sequentially, with non-GAAP EPS reaching $3.36. CEO Seamus Grady said the company delivered an “excellent second quarter,” driven by strong telecom demand, with that segment rising 59% year over year to $554 million, while high-performance computing revenue, which supports AI workloads inside large-scale data centers, surged to $86 million from $15 million in the prior quarter.

That strength reflects broader momentum across the optical networking industry, where companies like Lumentum Holdings, Coherent Corp., and Applied Optoelectronics are also benefiting from rising demand tied to AI-driven data center upgrades. Fabrinet stands out in this group because it manufactures components for multiple customers rather than competing directly with them, allowing it to capture growth across the ecosystem as spending accelerates.

Recent institutional filings added to the story and show how investors are repositioning around that trend. Baillie Gifford reduced its stake by 16% to 464,564 shares, while Vaughan Nelson Investment Management cut its position by 64.9% and Wedge Capital Management reduced its stake by 37.3%.

At the same time, Jackson Square Capital increased its stake by 449.8% to 11,403 shares, Fred Alger Management boosted its holdings by 139.6% to 42,625 shares, and Allspring Global Investments trimmed its position by 2.3% but still holds over 79,000 shares, showing mixed positioning but continued high institutional ownership of about 97%.

Looking ahead, Fabrinet is set to report fiscal Q3 2026 results on May 4, with management guiding for revenue of $1.15 billion to $1.20 billion and EPS of $3.45 to $3.60. The company is also expanding capacity through additional automated production lines, 120,000 square feet of new space at Pinehurst, and 250,000 square feet of Building 10 expected to come online midyear, positioning it to meet sustained demand from hyperscalers and networking companies building AI infrastructure.

Value Fabrinet instantly (Free with TIKR) >>>

Is Fabrinet Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): around 24%

- Operating Margins: around 11%

- Exit P/E Multiple: around 33x

Fabrinet’s growth is increasingly tied to demand for optical components used in AI data centers, where higher-speed networking upgrades like 800G and 1.6T transceivers are becoming necessary to handle rising data traffic.

Unlike peers such as Lumentum and Coherent that design and sell their own optical products, Fabrinet operates as a manufacturing partner, which allows it to benefit from industry growth without taking on the same product risk. This positioning allows Fabrinet to serve multiple customers across the ecosystem without directly competing with them.

See analysts’ growth forecasts and price targets for Fabrinet (It’s free) >>>

A key driver over the next 12 months is backlog conversion and capacity expansion, as customers secure long-term supply and Fabrinet ramps production through new facilities and automated lines, directly supporting revenue growth.

At the same time, a mix shift toward higher-value optical and high-performance computing products can support margin expansion, especially as AI-related demand becomes a larger portion of total revenue.

At current levels, Fabrinet appears modestly undervalued, with future performance driven by execution in scaling capacity, converting backlog into revenue, and sustained demand from AI infrastructure buildouts.

How Much Upside Does Fabrinet Stock Have From Here?

Investors can estimate Fabrinet’s potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value Fabrinet in under 60 seconds with TIKR (It’s free) >>>