Key Takeaways:

- Figma remains a leading collaborative design software platform, but investors are reassessing how quickly it can convert strong revenue growth into durable profits.

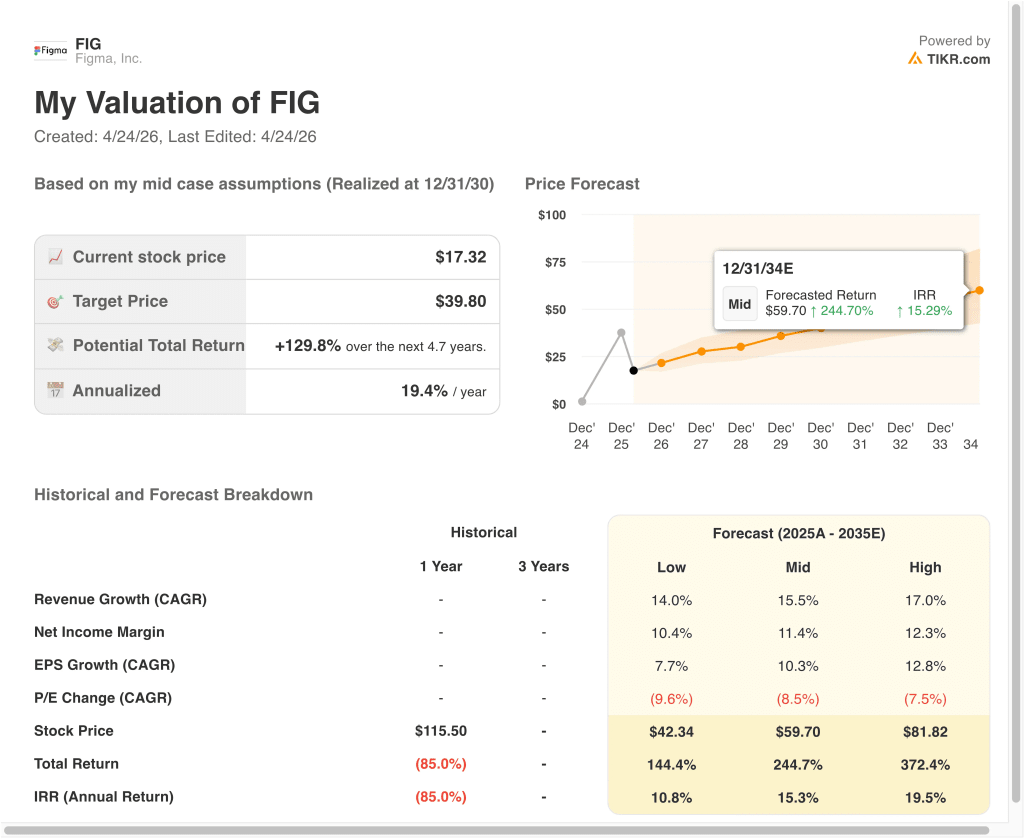

- FIG stock could reasonably reach $25 per share by December 2028, based on our valuation assumptions.

- This implies a total return of 45.5% from today’s price of $17, with an annualized return of 14.9% over the next 2.7 years.

What Happened?

Figma (FIG) has been under pressure in recent months as investors rotated away from richly valued software names and questioned how quickly newer public companies can grow into their valuations. Shares closed at $17 on April 23, 2026, well below earlier post-listing levels. That decline reflects changing sentiment more than a collapse in the underlying business.

The company still posted strong Q4 2025 results. Revenue came in at $303.8 million, ahead of Reuters-cited estimates of $293.2 million, showing enterprise demand for design collaboration tools remained solid. That matters because Figma’s products are embedded in workflows used by designers, developers, and product teams.

Investors also appear focused on competition and AI product cycles. Reuters noted shares slid after Anthropic unveiled Claude Design, which likely raised fresh questions around how generative AI could reshape software creation tools. Markets often reprice platform companies quickly when new AI entrants emerge.

Another overhang has been supply-related events, such as insider selling disclosures and the January lock-up expiration. Those events do not automatically change fundamentals, but they can weigh on short-term trading sentiment.

Here’s why Figma stock could recover if growth remains healthy, AI products gain traction, and profitability improves over time.

What the Model Says for Figma Stock

We analyzed the upside potential for Figma stock using valuation assumptions based on continued enterprise adoption, recurring subscription revenue, and improving monetization across newer products like developer tools, content management, and AI-assisted workflows.

Based on estimates of 18% annual revenue growth, 9.7% operating margins, and a normalized P/E multiple of 74.5x, the model projects Figma stock could rise from $17 to $25 per share.

That would be a 45.5% total return, or a 14.9% annualized return over the next 2.7 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for Figma stock:

1. Revenue Growth: 18%

Figma grew revenue from $749 million in 2024 to $1.06 billion in 2025, a 41% year-over-year increase. That is still rapid expansion for a company already above the $1 billion revenue mark. It shows continued demand across enterprise seats, team collaboration, and workflow expansion.

The company benefits from product-led adoption. Designers often start inside teams, then usage spreads to developers, marketers, and management. That creates natural expansion opportunities without relying only on new customer wins.

Based on analysts’ consensus estimates, we use an 18% forecast. That assumes growth moderates from earlier hyper-growth levels but remains strong as larger customers standardize on the platform.

2. Operating Margins: 9.7%

Figma’s reported operating margin remains negative today, largely because stock-based compensation and aggressive investment spending have weighed on reported earnings. LTM EBIT margin was around -122%, which highlights how expensive the current growth phase has been.

However, gross margin was still a strong 82.4%, which is a key software indicator. High gross margins often give companies room to improve operating leverage once hiring and go-to-market costs normalize.

Based on analysts’ consensus estimates, we use 9.7% operating margins. That reflects a path toward healthier scale economics as revenue grows faster than overhead over time.

3. Exit P/E Multiple: 74.5x

Figma trades in a premium software category where investors often pay for durable growth, sticky recurring revenue, and category leadership. Design infrastructure can be deeply embedded in customer workflows, which can support higher valuation multiples than slower-growth software peers.

At the same time, premium multiples require execution. If growth slows sharply or competition rises, markets can compress valuation quickly, which software investors have seen repeatedly.

Based on analysts’ consensus estimates, we use a 74.5x exit multiple. That assumes Figma remains viewed as a strategic growth platform rather than a mature software vendor.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for FIG stock through 2030 show varied outcomes based on AI execution, enterprise seat expansion, and valuation discipline (these are estimates, not guaranteed returns):

- Low Case: Growth slows faster than expected, and margins remain pressured → 10.8% annual returns

- Mid Case: Core subscriptions expand steadily, and monetization improves across products → 15.3% annual returns

- High Case: AI tools gain traction, enterprise adoption accelerates, and margins scale faster → 19.5% annual returns

The next move in Figma stock likely depends on whether investors view it as a temporary de-rating story or a durable software compounder. Upcoming Q1 2026 earnings in May could be an important catalyst. If revenue stays strong and losses narrow, sentiment could improve meaningfully.

See what analysts think about Figma stock right now (Free with TIKR) >>>

Should You Invest in Figma, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up FIG, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track FIG alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Figma stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!