Key Takeaways:

- Chevron shares have climbed about 22% in 2026 as energy prices, LNG recovery, and geopolitical risk supported oil stocks.

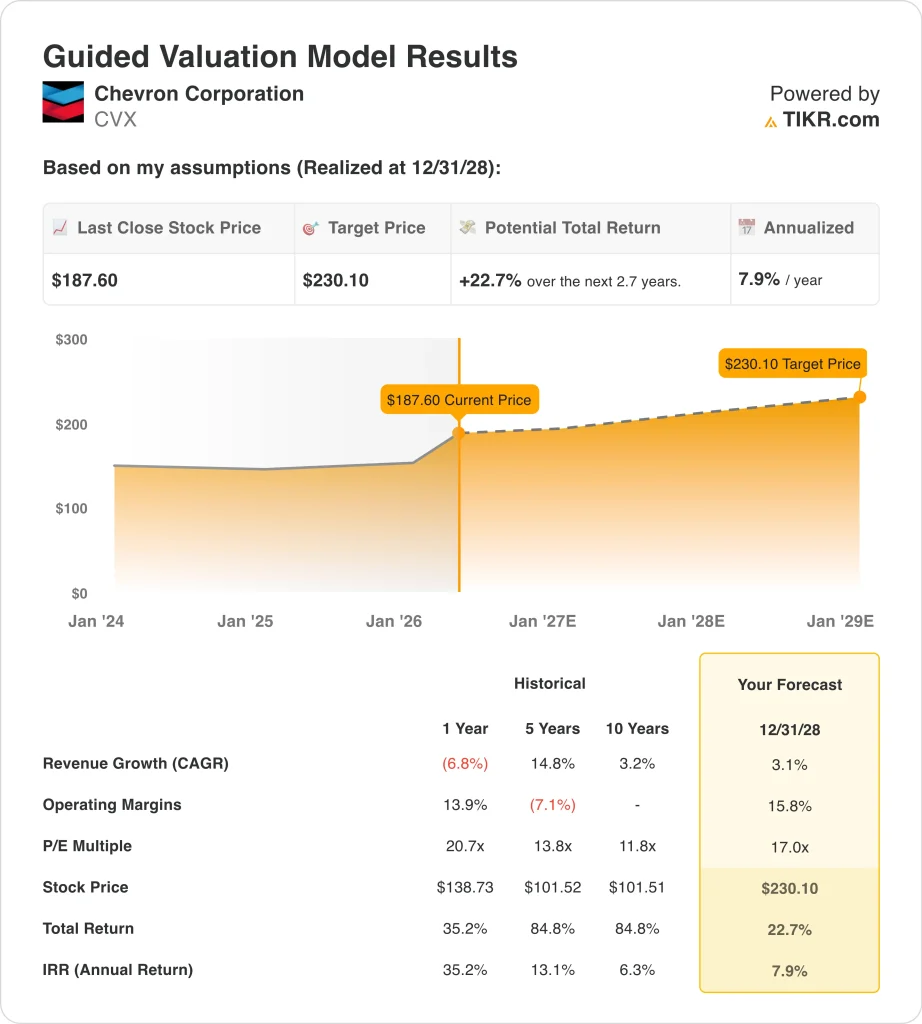

- CVX stock could reasonably reach $230 per share by December 2028, based on our valuation assumptions.

- This implies a total return of 22.7% from today’s price of $188, with an annualized return of 7.9% over the next 2.7 years.

What Happened?

Chevron Corporation (CVX) has benefited from stronger investor interest in energy stocks as oil markets react to geopolitical risk and supply uncertainty. CVX is up about 22% in 2026, but recent updates have been mixed. Investors are weighing higher commodity prices against near-term operational and cash flow headwinds.

Chevron recently said timing effects are expected to reduce Q1 earnings and cash flow from operations, excluding working capital, by about $2.7 billion to $3.7 billion after tax. That matters because investors often value oil majors on cash flow durability, not just reported earnings. These effects are expected to mainly affect Downstream, which includes refining and marketing.

Operations have also been in focus. Reuters reported that Chevron resumed full production at its Wheatstone LNG plant in Western Australia after repairs from cyclone damage. LNG, or liquefied natural gas, is important because it supports Chevron’s long-term gas growth strategy and global export earnings.

Chevron also agreed to a Venezuela asset swap that increases its exposure to heavy oil production in the Orinoco Belt. Reuters reported the deal raises Chevron’s Petroindependencia stake and adds a new oil area, while Chevron gives up offshore gas assets.

Here’s why Chevron stock could deliver moderate returns through 2029 if production improves, oil prices stay supportive, and cash returns remain steady.

What the Model Says for CVX Stock

We analyzed the upside potential for Chevron stock using valuation assumptions based on commodity prices, upstream production, LNG recovery, and capital returns.

Based on estimates of 3.1% annual revenue growth, 15.8% operating margins, and a normalized P/E multiple of 17.0x, the model projects Chevron stock could rise from $188 to $230 per share.

That would be a 22.7% total return, or a 7.9% annualized return over the next 2.7 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for CVX stock:

1. Revenue Growth: 3.1%

Chevron’s revenue fell 5.6% in 2025 to $184.7 billion as oil and gas pricing softened from earlier cycle highs. That shows how closely the business remains tied to commodity markets. Even strong production cannot fully offset weaker realized prices.

The company’s 2025 results still showed record worldwide and U.S. production growth. Chevron reported that 2025 worldwide production rose 12%, while U.S. production rose 16%. That gives the company a stronger volume base if commodity prices remain supportive.

Based on analysts’ consensus estimates, we used a 3.1% forecast. That reflects modest growth from production, LNG assets, and major projects, balanced against the cyclicality of oil and gas prices.

2. Operating Margins: 15.8%

Chevron’s LTM operating margin was 9.5%, down from stronger levels earlier in the cycle. Lower margins reflect softer commodity pricing, higher depreciation, and downstream volatility. The Q1 timing effects also show how refining and trading conditions can move short-term earnings.

The margin recovery case depends on better upstream profitability and fewer operational disruptions. Wheatstone’s restart helps because LNG assets can be meaningful contributors when running normally. Higher oil and gas prices would also improve operating leverage across Chevron’s production base.

Based on analysts’ consensus estimates, we use 15.8% operating margins. That assumes Chevron moves closer to mid-cycle profitability as production normalizes and commodity conditions remain reasonably supportive.

3. Exit P/E Multiple: 17x

Chevron trades at a premium to many cyclical energy names because of its scale, balance sheet, dividend history, and global asset base. The stock also offers a 3.8% dividend yield, which supports investor demand when rates and energy prices are stable.

Still, energy multiples can compress quickly when oil prices fall. Chevron’s LTM P/E is elevated because earnings have declined, while its forward P/E is closer to 16x. That means the market is already assuming some earnings recovery.

Based on analysts’ consensus estimates, we maintain a 17.0x exit multiple. That reflects Chevron’s quality premium, but also acknowledges that energy stocks rarely receive high multiples without stronger earnings growth.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for CVX stock through 2030 show varied outcomes based on oil prices, production execution, and valuation discipline (these are estimates, not guaranteed returns):

- Low Case: Oil prices soften, and margin recovery remains limited → 0.4% annual returns

- Mid Case: Production improves, and Chevron maintains steady cash returns → 5.8% annual returns

- High Case: Commodity prices stay supportive, but valuation compression offsets some gains → 4.8% annual returns

Chevron’s next move likely depends on Q1 earnings and management’s cash flow outlook. Investors will watch the May 1 earnings call for updates on timing effects, Wheatstone, capital spending, and shareholder returns. If Chevron shows cleaner cash flow and stronger production execution, the valuation case could look steadier.

See what analysts think about CVX stock right now (Free with TIKR) >>>

Should You Invest in Chevron Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CVX, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CVX alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Chevron stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!