Key Takeaways:

- PepsiCo’s Q1 results beat expectations as price cuts and brand refreshes helped improve demand, especially in North American snacks.

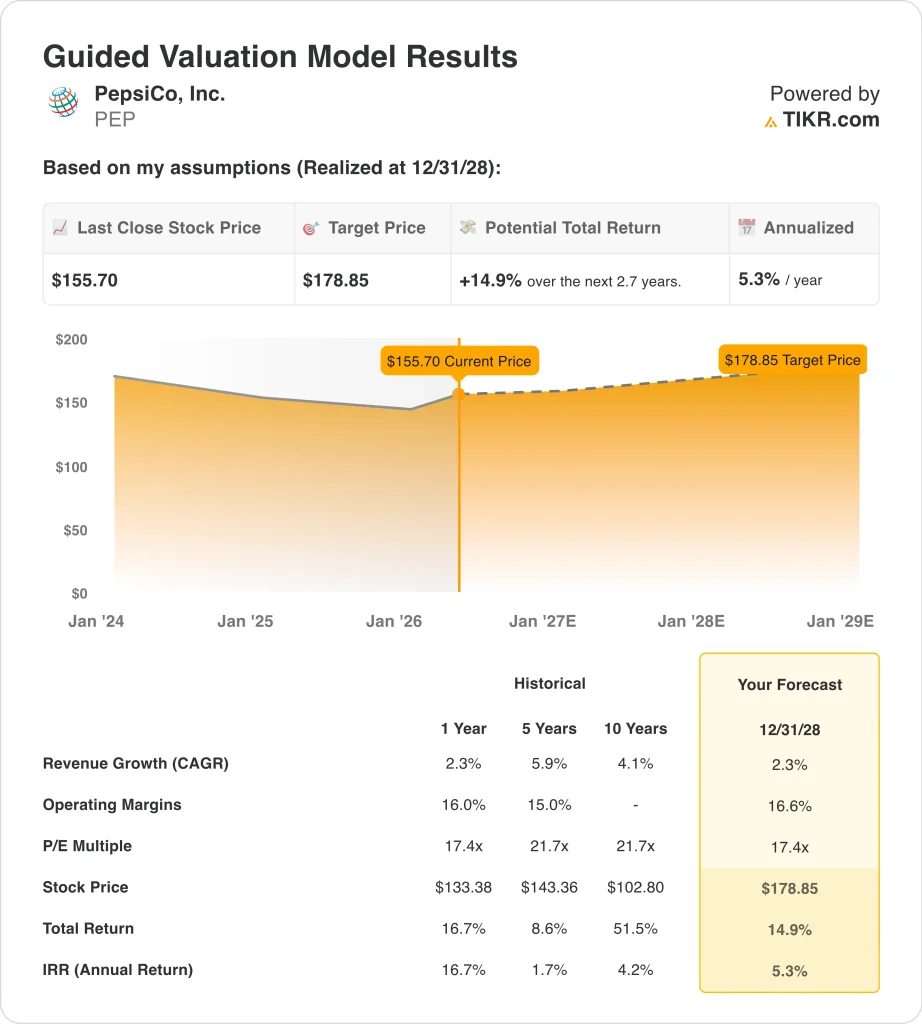

- PEP stock could reasonably reach $179 per share by December 2028, based on our valuation assumptions.

- This implies a total return of 14.9% from today’s price of $156, with an annualized return of 5.3% over the next 2.7 years.

What Happened?

PepsiCo (PEP) has regained some momentum after a difficult stretch for consumer staples stocks. Shares are up about 10% year-to-date, and investors are paying closer attention after the company’s Q1 2026 results beat expectations. The stock rose after PepsiCo reported Q1 revenue of $19.44 billion and core EPS of $1.61, both ahead of estimates.

The main story is that PepsiCo’s affordability push appears to be working. Reuters reported that the company cut prices on core U.S. snack brands such as Lay’s and Doritos by up to 15%, which helped its North American food business post its first volume growth in more than a year. That matters because investors had been worried that higher prices were pressuring demand.

PepsiCo also shifted its European bottling strategy. Royal Unibrew shares fell sharply after PepsiCo decided not to renew parts of its northern Europe bottling license and instead expanded its partnership with Carlsberg beginning in 2029. This move does not change near-term earnings much, but it shows PepsiCo is still optimizing its route-to-market system.

The company is also investing in digital operations. PepsiCo announced a multi-year collaboration with Google Cloud to use Gemini Enterprise across supply chain management, go-to-market execution, and internal workflows.

Here’s why PepsiCo stock could deliver moderate returns through 2029 if pricing, productivity, and brand investment keep margins stable.

What the Model Says for PEP Stock

We analyzed the upside potential for PepsiCo stock using valuation assumptions based on its global snack and beverage brands, stable cash flows, and modest revenue growth profile.

Based on estimates of 2.3% annual revenue growth, 16.6% operating margins, and a normalized P/E multiple of 17.4x, the model projects PepsiCo stock could rise from $156 to $179 per share.

That would be a 14.9% total return, or a 5.3% annualized return over the next 2.7 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for PEP stock:

1. Revenue Growth: 2.3%

PepsiCo is a mature global consumer staples company, so growth is naturally steadier than faster-growing categories. Revenue rose 2.3% in 2025 to $93.9 billion, while LTM revenue reached $95.4 billion. That reflects a business driven by pricing, brand strength, international expansion, and everyday consumption.

The recent Q1 beat showed that volume can improve when pricing becomes more consumer-friendly. Price cuts and product refreshes helped support North American snack demand, which had been a key concern. Still, management reaffirmed full-year expectations for 2% to 4% organic revenue growth.

Based on analysts’ consensus estimates, we used a 2.3% forecast. That reflects PepsiCo’s slower but durable growth profile, supported by snacks, beverages, distribution scale, and emerging market demand.

2. Operating Margins: 16.6%

PepsiCo’s margin story is about balance. The company needs to reinvest in pricing, brands, and innovation while still protecting profitability. LTM operating margin was 16.2%, and the model assumes modest improvement to 16.6%.

Productivity savings remain important because consumers are still sensitive to pricing. PepsiCo’s Q1 release showed core operating profit growth and margin expansion, supported by productivity and mix benefits. That helps offset cost pressure from commodities, freight, and geopolitical volatility.

Based on analysts’ consensus estimates, we use 16.6% operating margins. That assumes PepsiCo can manage costs carefully while using price investments to support volume recovery.

3. Exit P/E Multiple: 17.4x

PepsiCo’s valuation reflects a defensive business with reliable cash flow, but not a high-growth profile. The stock trades near 18x forward earnings and offers a dividend yield of about 4%. That makes the multiple sensitive to interest rates, volume trends, and dividend confidence.

The current valuation is below PepsiCo’s longer-term 5-year and 10-year historical P/E levels shown in the model. That discount reflects slower growth and investor caution toward staples stocks. It also reflects concerns about higher costs and weaker U.S. snack demand.

Based on analysts’ consensus estimates, we maintain a 17.4x exit multiple. That assumes PepsiCo remains valued as a stable, mature compounder rather than a faster-growth consumer stock.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for PEP stock through 2030 show varied outcomes based on volume recovery, pricing discipline, and margin execution (these are estimates, not guaranteed returns):

- Low Case: Snack demand stays soft, and inflation limits margin recovery → 4.6% annual returns

- Mid Case: PepsiCo stabilizes volumes while productivity supports steady earnings → 7.0% annual returns

- High Case: Brand refreshes and price investments drive stronger volume growth → 9.0% annual returns

PepsiCo’s next move likely depends on whether Q1’s volume improvement continues. The May 6 annual meeting and future updates on pricing, margins, and international partnerships could shape sentiment. If PepsiCo keeps improving demand without sacrificing profitability, the valuation case could remain steady.

See what analysts think about PEP stock right now (Free with TIKR) >>>

Should You Invest in PepsiCo?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up PEP, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track PEP alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze PepsiCo stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!