Key Takeaways:

- Okta has returned to profitability, with fiscal 2026 revenue up 11.8% to $2.9 billion and LTM free cash flow margins reaching 30%.

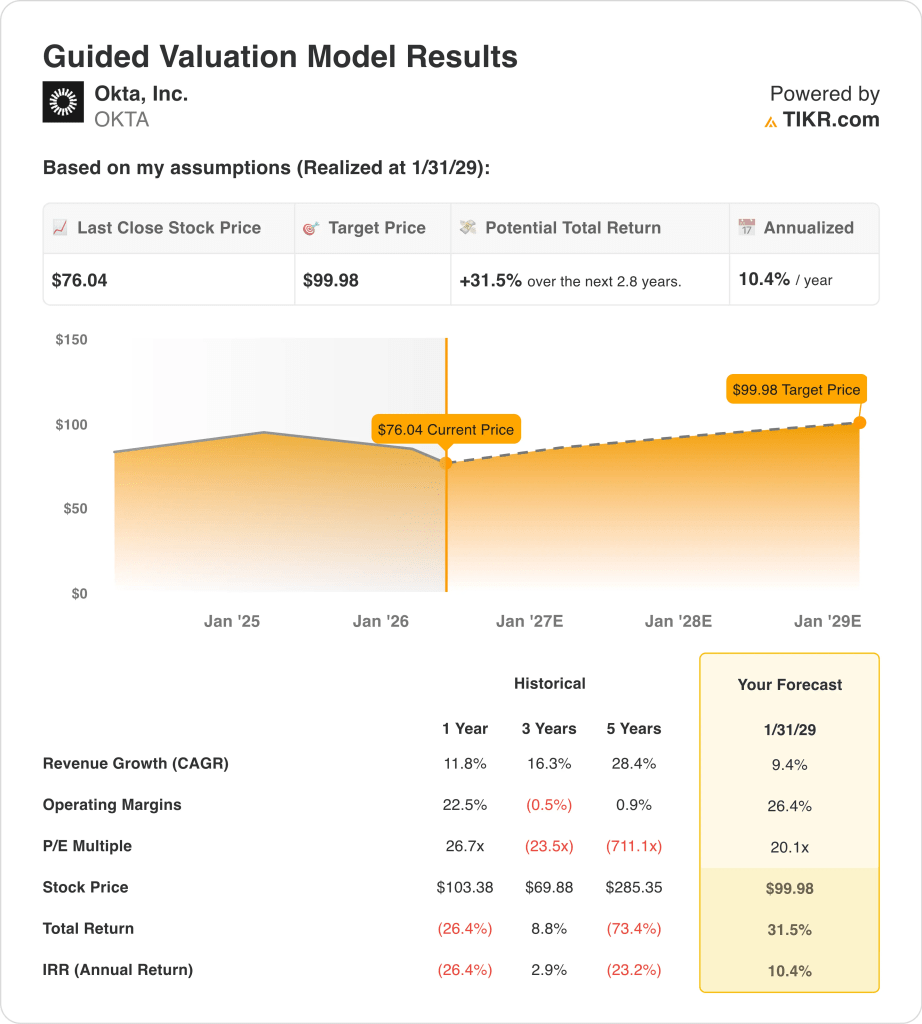

- OKTA stock could reasonably reach $100 per share by January 2029, based on our valuation assumptions.

- This implies a total return of 31.5% from today’s price of $76, with an annualized return of 10.4% over the next 2.8 years.

What Happened?

Okta (OKTA) has been under pressure over the past year as investors weighed slower software growth against improving profitability. The company’s stock is down about 23% over the past year, even though its margins and free cash flow have strengthened. That split shows investors are still debating whether Okta is a mature identity software company or a beneficiary of the next AI security cycle.

Okta reported Q4 fiscal 2026 revenue of $761 million, up 11% year-over-year, while subscription revenue also grew 11%. Remaining performance obligations grew 15%, and free cash flow reached $252 million for the quarter, showing the business is still adding contracted revenue while generating cash.

The newer catalyst is an AI agent identity. Okta announced that Okta for AI Agents would become generally available on April 30, 2026, giving enterprises a way to discover, govern, and secure non-human AI agents. That matters because AI agents can access software, data, and workflows, so companies need identity controls beyond traditional employee logins.

Market sentiment has been mixed. Software stocks sold off after concerns that advanced AI tools could disrupt cybersecurity vendors, but analysts have also highlighted identity security as a potential AI beneficiary.

Here’s why Okta stock could deliver solid returns through 2029 if AI agent security expands the identity market and margins continue improving.

What the Model Says for OKTA Stock

We analyzed the upside potential for Okta stock using valuation assumptions based on steady identity software demand, AI agent security adoption, and improving operating leverage.

Based on estimates of 9.4% annual revenue growth, 26.4% operating margins, and a normalized P/E multiple of 20.1x, the model projects Okta stock could rise from $76 to $100 per share.

That would be a 31.5% total return, or a 10.4% annualized return over the next 2.8 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for OKTA stock:

1. Revenue Growth: 9.4%

Okta’s revenue growth has moderated as the business has scaled. Revenue increased 11.8% in fiscal 2026 to $2.9 billion, down from much faster growth rates earlier in the company’s history. That shift is normal for a larger software platform, but it also means investors now care more about quality of growth.

The company still has structural demand behind it. Identity security remains critical as enterprises manage employees, contractors, customers, applications, and now AI agents. Okta’s new AI agent security products could help defend its relevance as access management becomes more complex.

Based on analysts’ consensus estimates, we used a 9.4% forecast. That reflects a maturing subscription business with continued expansion from workforce identity, customer identity, and AI-related security use cases.

2. Operating Margins: 26.4%

Okta has made a clear shift from growth at any cost toward profitable growth. Operating margin improved to 5.2% in fiscal 2026 after years of losses, while free cash flow margin reached 30%. That shows the company can generate cash even as GAAP profitability continues to build.

The margin story is important because Okta already has high gross margins. LTM gross margin was 77.4%, giving the company room to expand earnings if sales and marketing, R&D, and administrative costs grow slower than revenue. That operating leverage is the core reason the stock can work even with slower revenue growth.

Based on analysts’ consensus estimates, we use 26.4% operating margins. That assumes Okta continues scaling efficiently while investing in AI agent identity, partner channels, and enterprise go-to-market execution.

3. Exit P/E Multiple: 20.1x

Okta’s valuation has compressed from earlier software peaks. The stock now trades closer to a profitable software company than a hyper-growth cloud name. That lower multiple reflects slower growth, but it also gives investors a clearer earnings-based framework.

The company’s balance sheet helps support that valuation. Okta had net cash of about $2.1 billion, and the company announced a $1 billion share repurchase program in January 2026. That capital return can help offset dilution and signal confidence in cash generation.

Based on analysts’ consensus estimates, we maintain a 20.1x exit multiple. That reflects Okta’s improving profitability, strong free cash flow, and leadership in identity software, balanced against slower revenue growth.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for OKTA stock through 2031 show varied outcomes based on AI agent security adoption, margin execution, and valuation discipline (these are estimates, not guaranteed returns):

- Low Case: Identity software growth slows, and AI agent products take longer to scale → 4.6% annual returns

- Mid Case: Okta grows steadily while margins expand and AI security demand builds → 7.8% annual returns

- High Case: AI agent identity becomes a larger growth driver, and profitability scales faster → 10.8% annual returns

OKTA’s next move likely depends on whether investors see AI agents as a threat or a new identity security opportunity. The April 30 launch of Okta for AI Agents and the expected May Q1 update could shape that debate. If Okta keeps expanding margins while proving AI can increase demand for identity controls, the valuation case could strengthen.

See what analysts think about Okta stock right now (Free with TIKR) >>>

Should You Invest in Okta, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Okta, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Okta alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Okta stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!