Key Takeaways:

- AMD is benefiting from strong AI accelerator and data center demand, and 2025 revenue rose 34% while free cash flow increased to about $6.7 billion.

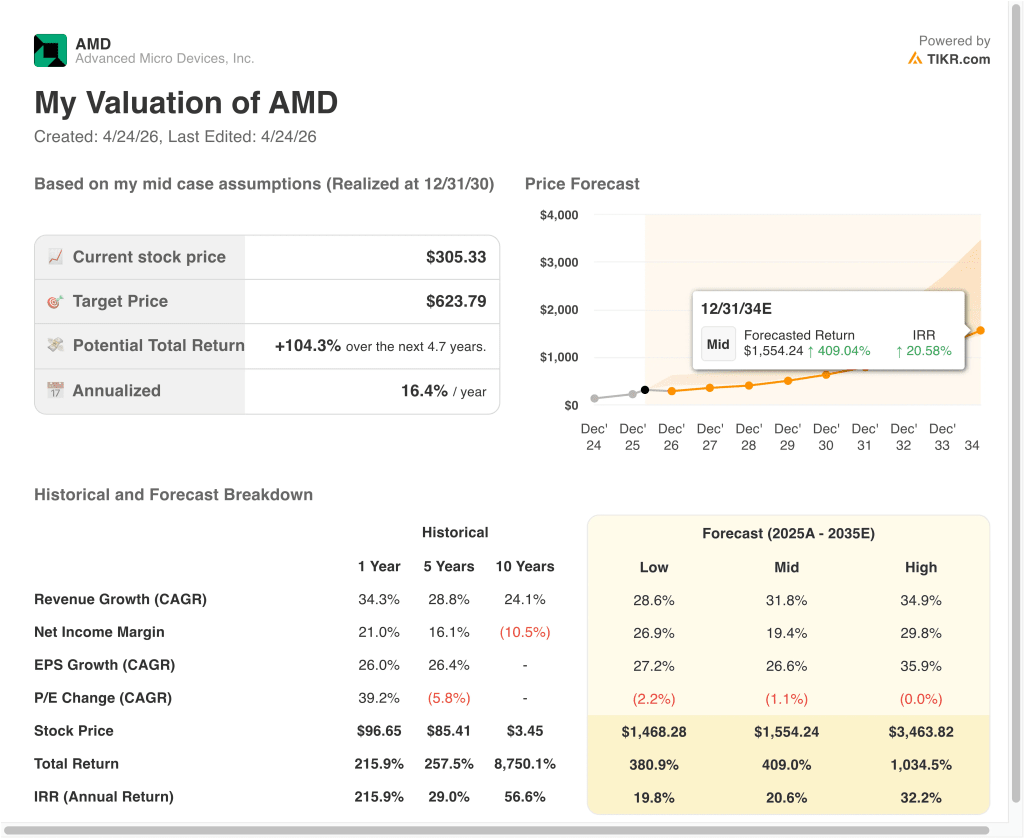

- AMD stock could reasonably reach $438 per share by December 2028, based on our valuation assumptions.

- This implies a total return of 43.4% from today’s price of $305, with an annualized return of 14.3% over the next 2.7 years.

What Happened?

Advanced Micro Devices (AMD) has become one of the market’s biggest AI chip stories. AMD is up about 238% over the past year as investors focus on AMD’s role in GPUs, server CPUs, and AI infrastructure. AMD reported record fourth-quarter revenue of $10.3 billion and full-year 2025 revenue of $34.6 billion.

The biggest recent catalyst was AMD’s expanded partnership with Meta. AMD said Meta will deploy 6 gigawatts of AMD GPUs, starting with the MI450 platform in the second half of 2026. That deal matters because it gives AMD a large hyperscale customer as it tries to compete more directly in AI accelerators.

AMD also announced a strategic partnership with Nutanix to support open enterprise AI platforms, adding another channel for AI adoption beyond hyperscale cloud customers. The company’s upcoming earnings call on May 5, 2026, will be important because investors will be watching whether AI demand is translating into revenue visibility. Strong AI spending across the semiconductor supply chain has also supported sentiment toward chip stocks.

Here’s why AMD stock could keep moving as AI GPU demand, execution on MI450, and margin improvement shape the next phase of the story.

What the Model Says for AMD Stock

We analyzed the upside potential for AMD stock based on its AI accelerator ramp, data center momentum, and improving earnings power.

Based on estimates of 34.0% annual revenue growth, 22.4% operating margins, and a normalized P/E multiple of 35.2x, the model projects AMD stock could rise from $305 to $438 per share.

That would be a 43.4% total return, or a 14.3% annualized return over the next 2.7 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for AMD stock:

1. Revenue Growth: 34%

AMD’s growth story is being driven by AI accelerators, server CPUs, and stronger data center demand. Revenue rose 34.3% in 2025 to $34.6 billion. That marks a major acceleration from 13.7% growth in 2024.

The market is pricing AMD as a serious AI infrastructure supplier. The Meta deal adds scale to that story because it ties AMD’s MI450 platform to a major long-term deployment. Investors are watching whether this converts into sustained data center revenue growth.

Based on analysts’ consensus estimates, we use a 34.0% revenue growth forecast. This reflects strong AI-related demand, but it still depends on AMD executing product ramps and competing effectively against Nvidia.

2. Operating Margins: 22.4%

AMD’s operating margin improved to 10.8% in 2025 from 8.1% in 2024. Gross margin stayed strong at 52.5%, showing that the business can generate attractive profitability even while investing heavily in R&D. R&D spending reached $8.1 billion, which reflects how aggressively AMD is funding future chip platforms.

The margin story depends on the mix. AI GPUs and server CPUs can support higher profitability, but product ramps, customer pricing, and supply-chain costs can still pressure results. Investors need evidence that AI revenue growth is improving operating leverage.

Based on analysts’ consensus estimates, we use a 22.4% operating margin forecast. This assumes AMD scales higher-value AI and data center products while keeping spending discipline.

3. Exit P/E Multiple: 35.2x

AMD’s valuation reflects high expectations for AI growth. The model uses a 35.2x P/E multiple, which is close to the 1-year historical multiple and below the unusually elevated 10-year historical figure. That keeps the valuation tied to recent earnings power rather than older cycle extremes.

The stock already trades at a premium because investors expect faster AI-related growth. At the same time, AMD must prove that its AI roadmap can convert into durable earnings. That makes the multiple sensitive to execution.

Based on analysts’ consensus estimates, we use a 35.2x exit P/E multiple. This reflects AMD’s stronger growth profile while still recognizing that semiconductor valuations can compress quickly if expectations cool.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for AMD stock through 2035 show varied outcomes based on AI infrastructure demand, margin execution, and valuation discipline:

- Low Case: AI GPU adoption grows, but valuation compression limits returns → 19.8% annual returns

- Mid Case: AMD scales AI accelerators and data center CPUs as expected → 20.6% annual returns

- High Case: AI demand remains exceptionally strong, and margins expand further → 32.2% annual returns

Even in the conservative case, Vertiv stock offers positive returns supported by its strong position in power and cooling infrastructure, rising free cash flow, and deep exposure to AI data center spending.

AMD’s next move will likely depend on whether the MI450 ramp supports the growth investors are already pricing in. The stock has already moved sharply, so revenue visibility and margin quality matter more from here. If AMD converts AI partnerships into sustained earnings growth, the valuation setup could remain compelling.

See what analysts think about AMD stock right now (Free with TIKR) >>>

Should You Invest in Advanced Micro Devices?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up AMD, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track AMD alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Advanced Micro Devices stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!