Key Stats

- Current price: ~$93

- Q1 2026 total revenue: $14.6B (+10.6% YoY)

- Q1 2026 adjusted EPS: $1.19 (+31% YoY)

- Q2 2026 EPS guidance: $1–$2

- Full-year 2026 EPS guidance: $7–$11

- 2027 pretax margin target: at least 10%

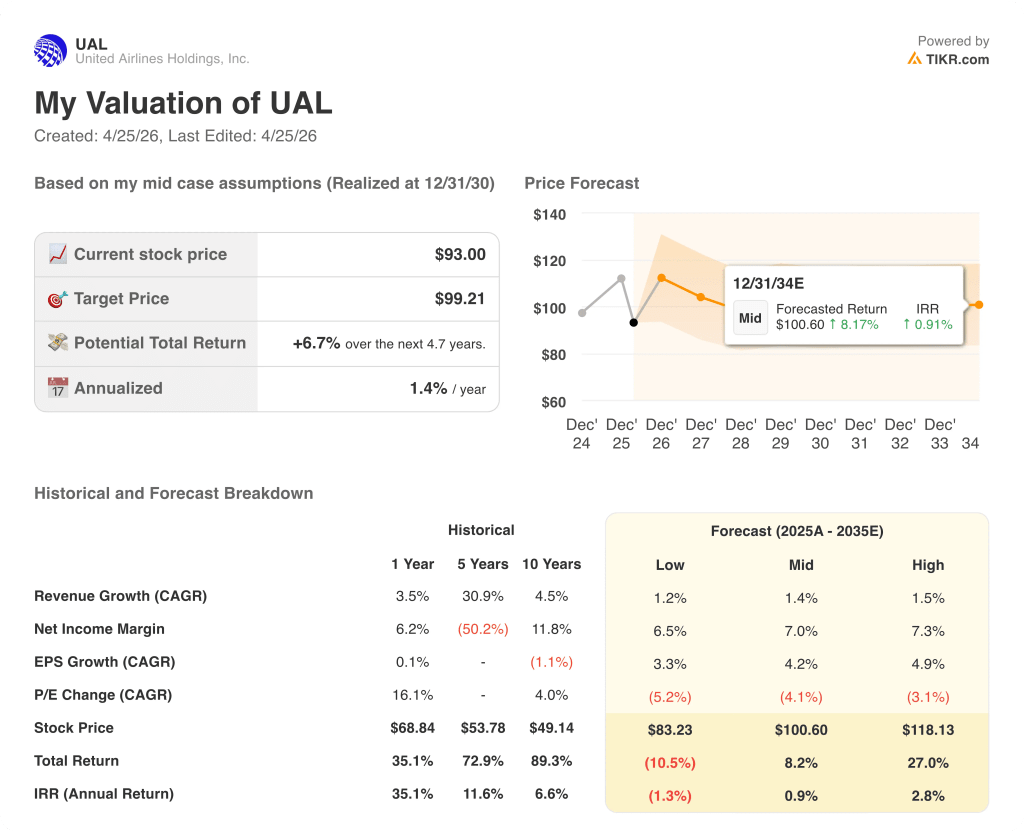

- TIKR model price target: ~$99 (mid-case)

- Implied upside over ~5 years: ~7%

United Airlines Stock Q1 2026: Revenue Hits Record $14.6B as Fuel Costs Bite Into Margins

United Airlines stock (UAL) opened Q1 2026 with a record quarterly revenue result even as a surging fuel bill compressed margins and forced management to rethink the back half of the year.

Total revenue reached $14.6B in the March quarter, up 10.6% year-over-year, according to CCO Andrew Nocella on the Q1 2026 earnings call.

Adjusted EPS came in at $1.19, up 31% year-over-year and within management’s initial guidance range of $1.00–$1.50, according to CFO Mike Leskinen on the Q1 2026 earnings call.

The outperformance came despite a $340M higher fuel bill in the quarter, which CFO Leskinen attributed to the run-up in jet fuel prices following the Iran conflict.

Premium demand was the standout driver: premium revenues rose 13.6% on only 4.4% higher capacity, with premium RASM up 8.9% year-over-year, outpacing the main cabin by 4 points, according to CCO Nocella on the Q1 2026 earnings call.

Business travel revenue grew 14% year-over-year with broad-based strength across all verticals, according to CCO Nocella.

Loyalty revenue outperformed as well, up 13% in the quarter, supported by MileagePlus program updates and healthy card spend, according to CCO Nocella.

United implemented five broadly successful price increases late in Q1, along with higher baggage fees, as management moved to offset elevated fuel costs, according to CCO Nocella.

Selling yields accelerated sharply through the quarter: up 4% in January and February, rising to 12% in the first half of March, then 18% in the second half of March, according to CCO Nocella.

As of the most recent week in April, selling yields for all future travel were up 20% year-over-year, according to CCO Nocella.

For Q2 2026, management guided EPS to $1.00–$2.00, anchored by an assumed all-in fuel price of approximately $4.30 per gallon, per CFO Leskinen.

Full-year 2026 EPS guidance was set at $7.00–$11.00, with management expecting to recover 40–50% of elevated fuel costs in Q2, 70–80% in Q3, and 85–100% by Q4, per CFO Leskinen.

In response to the fuel environment, United proactively cut approximately 5 points of planned capacity for the rest of 2026, targeting Q3 and Q4 at flat to up 2% year-over-year, per CCO Nocella.

On the balance sheet, United paid down more than $3.1B in debt during the quarter and generated $2.9B in free cash flow, according to CFO Leskinen.

UAL Stock Financials: Margin Compression Returns as Fuel Costs Weigh

United Airlines stock is navigating a familiar tension: revenue accelerating while margin structure softens under cost pressure.

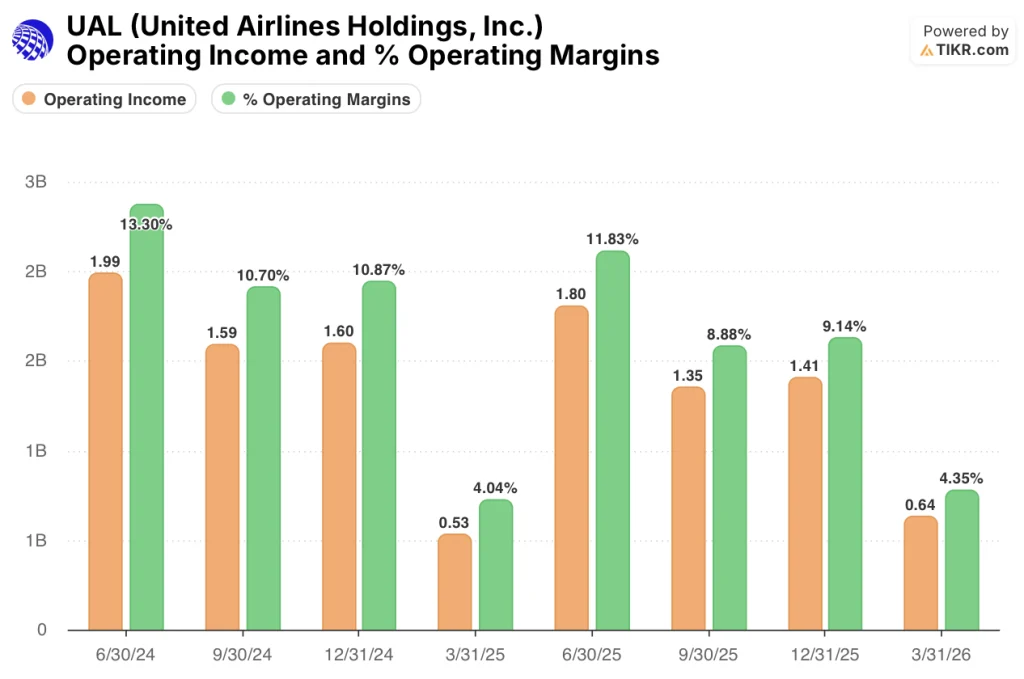

Gross profit in the March 2026 quarter was $4.46B, with gross margin at 30.5%, roughly flat with the year-ago quarter’s 30.9% and well below the 36.2% peak posted in the June 2025 quarter.

The gross margin compression from Q2 2025 through Q1 2026 (36.2%, 34%, 34.3%, 30.5%) reflects the progressive fuel cost build, not deteriorating demand.

Operating income came in at $640M, up 19% from $530M in the prior-year March quarter, driven by revenue outperformance partially offset by cost pressure.

Operating margin landed at 4.3%, up from 4% in Q1 2025 but well below the 9.1% and 11.8% posted in the two preceding quarters.

CASM-ex rose 5.9% year-over-year, pressured by close-in flight cancellations, storm-related disruptions, and the pullback from low-cost markets including Tel Aviv and Dubai, which together represented 1.5 points of capacity, according to CFO Leskinen.

Valuation Model Take: Limited Upside Priced In at Current Levels

The TIKR valuation model prices United Airlines stock at approximately $99 on mid-case assumptions, implying roughly 7% total upside from the current price of $93 over a 4.7-year horizon, an annualized return of just 1.4%.

The mid-case model assumes a revenue CAGR of 1.4%, a net income margin of 7.0%, and EPS growth of 4.2% annually through 2035.

Those assumptions embed a conservative read on United Airlines stock: a business that sustains profitability and marginally grows earnings but does not re-rate as the fuel environment normalizes.

After a Q1 that showed EPS up 31% on record revenue despite a $340M fuel headwind, the earnings quality argument is intact. But the valuation model reflects the wide uncertainty in the forward EPS range ($7–$11), not the upside scenario.

At current prices, United Airlines stock is not priced for a bull outcome. The investment case is roughly unchanged from pre-Q1: the stock needs sustained fuel cost recovery and margin expansion to justify a materially higher price.

The central tension: United posted a resilient Q1, but the full-year EPS range of $7–$11 means the stock’s fair value swings by nearly 40% depending on how quickly fuel costs are absorbed.

Bull Case

- Selling yields are already up 20% year-over-year as of the latest week in April, with management targeting 85–100% fuel cost recovery by Q4 2026.

- Premium revenue grew 13.6% on just 4.4% capacity growth in Q1, demonstrating pricing power that reads as structural, not cyclical.

- Seven commercial initiatives, including nested digital selling and 50 A321 Coastliners with lay-flat beds, represent what CCO Nocella described as hundreds of millions in annual revenue opportunity, independent of the fuel environment.

- The high-case TIKR scenario targets $118 per share, a total return of +27%, if the 2027 pretax margin target of at least 10% is achieved.

Bear Case

- The $4 gap between the $7 low-case and $11 high-case EPS guidance reflects genuine uncertainty about demand elasticity at yields up 20%, which management acknowledged has not yet materialized but expects to arrive per Econ 101.

- CASM-ex is already running up 5.9% year-over-year, and the 5-point capacity reduction planned for Q3 and Q4 will continue to pressure unit costs with no near-term relief.

- The low-case TIKR scenario implies a stock price of $83, a total return of negative 10.5% from current levels if fuel persists and demand eventually softens.

- United pre-sold 23% of Q2 capacity and 8% of Q3 capacity at lower price points before the fuel spike, capping near-term yield upside regardless of demand strength.

Should You Invest in United Airlines Holdings, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up UAL stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track United Airlines Holdings, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze UAL stock on TIKR for Free →