Key Stats

- Current Price: ~$89

- Q1 2026 Total Revenue: $6.5B, up 16% YoY

- Q1 2026 Adjusted EPS: $1.43 (record), up 38% YoY

- Core Net New Assets: $158B (Q1 record)

- New Brokerage Accounts Opened: 1.3M, up 10% YoY

- Total Client Assets: $11.8T

- 2026 EPS Outlook: Tracking above prior $5.70–$5.80 scenario; full update at July business update

- TIKR Model Price Target: $159 (mid case, target date 12/31/30)

- Implied Upside Over ~5 Years: ~79%

Charles Schwab Stock Posts Record Revenue and EPS as Client Engagement Hits New Highs

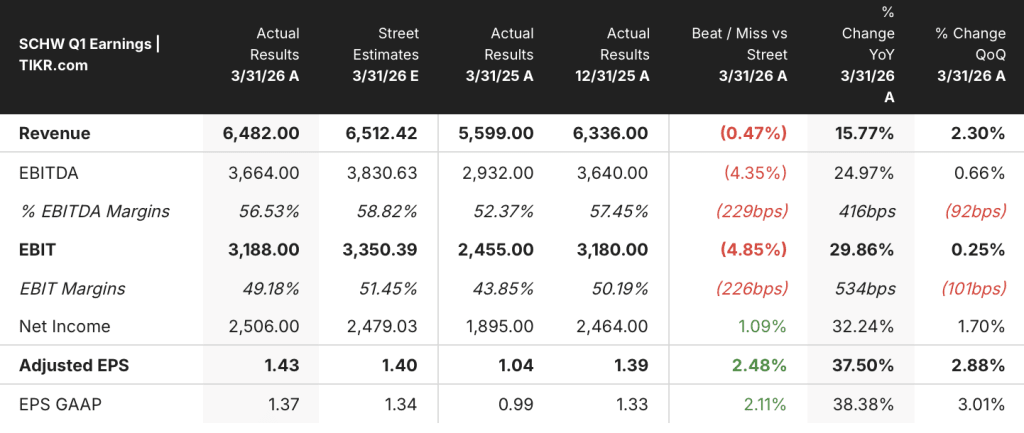

Charles Schwab stock (SCHW) delivered a clean record quarter in Q1 2026, with adjusted EPS of $1.43 beating the prior-year period by 38% and total revenue reaching $6.5B, up 16% year-over-year, according to CFO Mike Verdeschi on the Q1 2026 earnings call.

Every major revenue line grew at double-digit rates in the quarter.

Net interest revenue rose 16% year-over-year, aided by the continued reduction of higher-cost borrowings and increased utilization of lending solutions by clients.

Asset management and administration fees grew 15% year-over-year to a record $1.8B, driven by strong asset gathering and client interest in wealth and asset management offerings, according to CFO Verdeschi on the Q1 2026 earnings call.

Trading revenue rose 20% year-over-year as the firm’s retail platform supported a record 9.9 million daily average trades.

Bank deposit account fees also increased 20% year-over-year as lower-yielding fixed-rate obligations continued maturing into higher yields.

Schwab attracted $158B in core net new assets in Q1, a first quarter record, bringing total client assets to $11.8T.

Managed investing net flows rose 46% to an all-time high, with Schwab Wealth Advisory alone generating a record $10B in net flows, up 90% year-over-year, according to CEO Rick Wurster on the Q1 2026 earnings call.

Clients opened 1.3 million new brokerage accounts in the quarter, up 10% over last year.

Adjusted expenses grew 5% year-over-year, producing an adjusted pretax profit margin of 51.4%.

Schwab repurchased $2.4B of common shares during Q1 and raised its common stock dividend by 19%.

On the outlook, CFO Verdeschi stated the firm is now tracking above the $5.70–$5.80 EPS scenario shared in January, which excluded the impact of buybacks and the Forge acquisition, citing a more favorable rate environment and strong client engagement; a comprehensive 2026 scenario update will follow at the July business update.

On the product front, Schwab’s employee pilot for spot crypto (Bitcoin and Ether) is underway, with a phased client rollout beginning in the coming weeks at 75 basis points per trade.

Charles Schwab Stock Financials: Operating Leverage Continues to Build

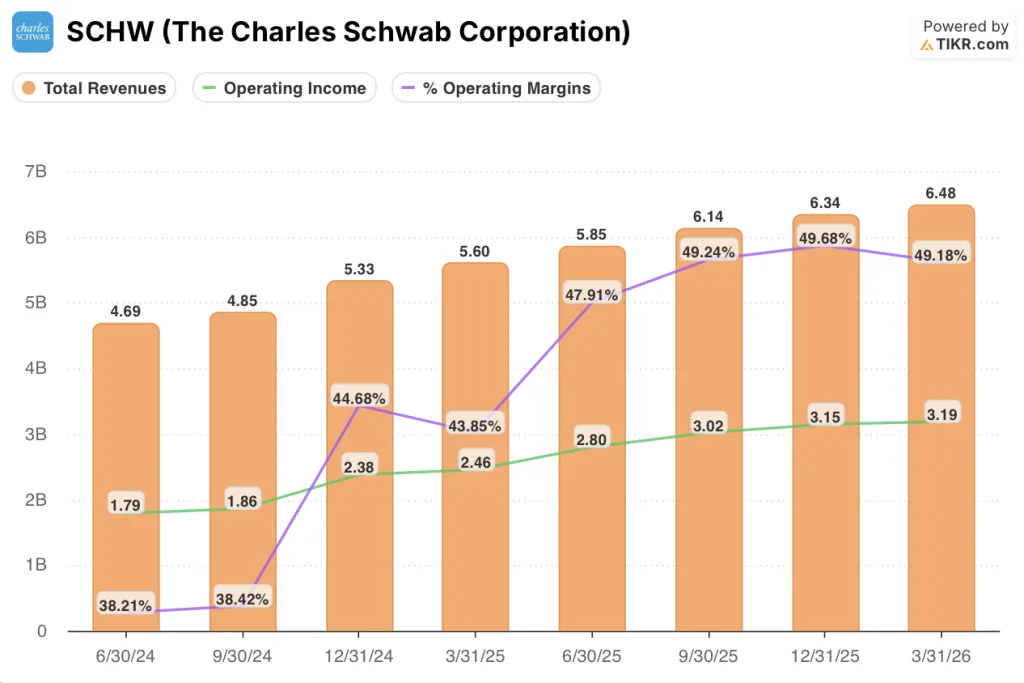

Charles Schwab stock is in a sustained operating leverage story, with revenue compounding faster than costs across every quarter in the trailing eight-period window shown on the TIKR income statement.

Total revenues rose from $4.69B in the June 2024 quarter to $6.48B in the March 2026 quarter, with year-over-year growth accelerating from 2.9% in June 2024 to a peak of 26.6% in the September 2025 quarter before moderating to 15.8% in Q1 2026.

Operating income followed the same arc, climbing from $1.79B in June 2024 to $3.19B in March 2026, representing 30% year-over-year growth in the most recent quarter.

Operating margin expanded sharply over the period, from 38% in the June 2024 quarter to a peak of 50% in the December 2025 quarter, settling at 49% in Q1 2026.

The slight sequential margin step-down from 49.7% to 49.2% reflects Q1 seasonality in compensation expense and increased investment in strategic initiatives including AI and new product launches, per CFO Verdeschi on the Q1 2026 earnings call.

Net interest income, the largest revenue component, peaked at $3.17B in Q4 2025 and came in at $3.14B in Q1 2026, a modest sequential dip that CFO Verdeschi attributed to normal Q1 cash seasonality; he expressed confidence in a continued upward trajectory through the year.

What Does the Valuation Model Say?

The TIKR model prices Charles Schwab stock at a target of $159 under mid-case assumptions, implying approximately 79% upside from the current price of ~$89, to be realized by December 2030.

The mid-case model assumes a revenue CAGR of 6.7% and a net income margin of 41%, with EPS growing at an 11.6% annualized rate.

Q1 2026’s record EPS and 51% adjusted pretax profit margin strengthen the credibility of those assumptions: the firm is already converting revenue at a rate that puts 41% net income margins firmly within reach as the balance sheet continues to normalize.

Charles Schwab stock looks meaningfully undervalued at current levels, and a rate environment now pricing in fewer Fed cuts than the January scenario would only add to the upside from here.

The central tension in Charles Schwab stock after Q1 2026: every operating metric is running ahead of plan, but the bull case depends on whether the sweep cash revenue model holds as AI-enabled competitors reduce friction around client cash optimization.

Bull Case

- Revenue grew 16% to a record $6.5B and adjusted EPS hit $1.43, already tracking ahead of the prior $5.70–$5.80 full-year EPS scenario with buybacks and Forge contributions not yet included

- The lending engine is compounding fast: bank loan balances reached $61B, up 29% year-over-year, with pledged asset line balances at all-time records, diversifying revenue beyond net interest income at healthy spreads

- Managed investing net flows hit an all-time record with Schwab Wealth Advisory posting $10B in Q1 alone, up 90% year-over-year, building a growing fee-based revenue stream structurally less sensitive to rate movements

- Spot crypto launching in coming weeks at 75bps per trade, the Forge acquisition closed, and AI-powered client capabilities rolling out in May and June 2026 represent incremental revenue vectors not reflected in the current model scenario

Bear Case

- Operating margin dipped sequentially from 49.7% in Q4 2025 to 49.2% in Q1 2026, and if client cash in sweep accounts migrates to higher-yielding alternatives, net interest income faces structural pressure even in a favorable rate environment

- Daily average trades hit a record 9.9 million, but revenue per trade declined as clients traded smaller equity positions with less conviction rather than higher-revenue derivatives; a calmer market could produce fewer trades without recovering per-trade economics

- The “tracking above $5.70–$5.80” commentary explicitly excludes buyback contributions and Forge, meaning management has not yet issued a formal upward revision, and the July scenario update could reset expectations in either direction

- Cash sweep competition is intensifying: JPMorgan’s low-friction brokerage cash product was addressed directly on the call, and management’s defense rests on client inertia and one-click optimization tools that well-resourced competitors can replicate

Should You Invest in The Charles Schwab Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up SCHW stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track The Charles Schwab Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze SCHW stock on TIKR for Free →