Key Stats for Emerson Electric Stock

- 52-Week Range: $103 to $165

- Current Price: $141

- Street Mean Target: $164

- Street High Target: $205

- Analyst Consensus: 15 Buys / 3 Outperforms / 9 Holds / 1 Underperform / 1 Sell

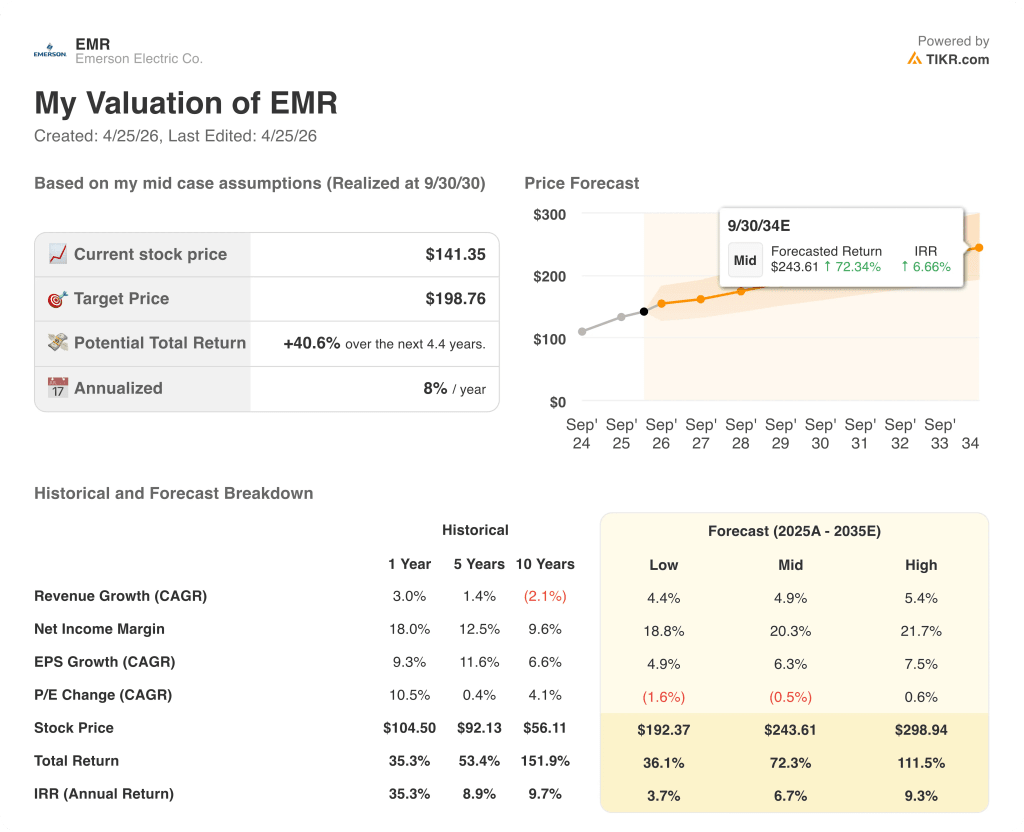

- TIKR Model Target (Sep.. 2030): $199

What Happened?

Emerson Electric stock (EMR) represents a company that spent five years dismantling a conglomerate and rebuilding itself as the world’s leading industrial automation business, making the control systems, sensors, valves, and software that run power plants, LNG terminals, life sciences facilities, and AI data centers.

The company’s fiscal first quarter ended December 31, 2025, and the headline result was a clean beat.

Adjusted EPS came in at $1.46 against a Street estimate of $1.41, a 5.8% year-over-year improvement, while net sales of $4.35 billion grew 4.1% and matched consensus almost exactly.

The number that actually mattered was orders: underlying order growth of 9% marked four consecutive quarters of acceleration, pushing the trailing twelve-month order rate to 6% and the backlog to $7.9 billion, up 9% year-over-year with a book-to-bill of 1.13.

The standout within that figure was Ovation, Emerson’s power generation control platform, which saw orders surge 74%, driven by behind-the-meter data center projects and utility fleet modernizations across the United States and Middle East.

CEO Lal Karsanbhai described the pipeline’s composition on Q1 2026 earnings call: “Emerson was chosen to automate on-site power generation for a new 1.7-gigawatt AI data center in the United States, helping to meet accelerated deployment timelines and mission-critical reliability.”

Emerson also won the automation contract for Sempra Infrastructure’s Port Arthur LNG Phase 2, which will add 13 million tons per annum of capacity to the U.S. Gulf Coast, selected specifically because DeltaV, Emerson’s flagship control system, runs more than 50% of every LNG installation on the planet.

Test and Measurement, the business built around the National Instruments acquisition, grew 11% in the quarter with orders up 20%, led by semiconductor, aerospace and defense, and the broad portfolio business, with three of four sub-segments growing 20% to 30% in orders.

Software annual contract value (ACV) grew 9% year-over-year to $1.6 billion, and management reiterated a 10% plus ACV growth target for the full year, a commitment held despite widespread investor anxiety about AI disrupting industrial software models.

The company raised the bottom and midpoint of its fiscal 2026 adjusted EPS guidance to $6.40 to $6.55 and completed $250 million of share repurchase in the quarter as part of a plan to return roughly $2.2 billion to shareholders this year.

Emerson’s project funnel held at $11.1 billion, replenished after $450 million in Q1 wins, with 80% of those wins coming from power, LNG, semiconductor, life sciences, and aerospace and defense.

The software contract renewal accounting dynamic, which reduces reported first-half revenue by about a point of growth, has been the source of most near-term investor skepticism, but management’s framing has been consistent: strip it out, and the underlying growth rate in Q1 was closer to 3% to 4%, and the second half is expected to accelerate to around 6%.

Wall Street’s Take on EMR Stock

The Q1 beat arrives as the Street is still discounting Emerson’s organic growth rate by roughly 2 points, because a software contract renewal accounting dynamic is compressing reported first-half sales growth from an underlying 4% to 5% run rate to an optics-level 2%, creating a valuation gap that is more accounting artifact than fundamental deterioration.

Of 27 analysts covering Emerson Electric stock, 18 rate it buy or outperform, 9 hold, and 2 underperform or sell, with a mean price target of around $164, implying roughly 16% upside; the Street is specifically watching for mid-single-digit order rates to hold through mid-2026 and for second-half backlog conversion to confirm the revenue ramp.

The spread between the $104 low target and the $205 high reflects a real debate: bears near the floor are skeptical of execution on the 2028 $8 EPS target in an environment of China and Europe softness, while Jefferies’ $175 buy thesis, initiated in late March, points to accelerating earnings growth, order momentum in secular growth verticals, and a resilient maintenance, repair, and operations (MRO) model that generates about 65% of revenue from recurring installed-base spend.

Priced at roughly 22x forward adjusted EPS on guidance management has already raised once this year, while the path to around $8 in adjusted EPS by fiscal 2028 implies a steep discount to the stock’s future earnings power, Emerson Electric stock appears undervalued against a backdrop of four consecutive quarters of order acceleration, a $11.1 billion funnel weighted 80% toward secular growth verticals, and software ACV growing at 9% to 10% annually.

At the Barclays Industrial Select Conference, Karsanbhai made the case that Emerson’s software carries three structural moats against AI disruption: vertical and deterministic architecture built on decades of domain expertise, mission-critical regulated industries where latency and hallucinations are unacceptable, and usage-based or perpetual pricing that is immune to seat-count reduction.

The core risk is whether the second-half revenue acceleration materializes: if North America order rates moderate faster than the modeled mid-single-digit pace or if China slips beyond the already-assumed low-single-digit decline, the backlog phasing that underpins the 6% second-half growth guide comes under real pressure.

On May 5, when Emerson reports fiscal Q2, the number to watch is Software and Systems underlying growth ex-renewals, guided flat for Q2 but up 4% for the full year, which will confirm whether ACV adoption is tracking toward the 10% plus target that the 2028 margin expansion model depends on.

What Does the Valuation Model Say?

The TIKR model’s mid-case target of around $199 per share is built on a revenue CAGR of roughly 5% and a net income margin expanding to around 20%, inputs that are actually conservative relative to management’s own 2028 framework calling for $21 billion in revenue and 30% adjusted segment EBITA margins, which would support a higher terminal value than the model currently assumes.

At roughly 22x forward EPS on a fiscal 2026 guide that management raised at the first opportunity, while the roadmap to around $8 EPS by 2028 implies earnings growth of roughly 24% from the midpoint of current guidance, Emerson Electric stock is undervalued for investors willing to hold through the software renewal accounting noise and the China/Europe drag that is masking the true organic run rate.

Emerson stock’s investment case hinges on a single transition: whether the second-half 2026 revenue acceleration from roughly 2% to roughly 6% in underlying growth actually materializes, or whether macro softness and backlog timing undercut the ramp management has guided with unusual specificity.

What Has to Go Right

- North America order rates hold in the high single-digit range, sustained by power generation, LNG, and nearshoring tailwinds that drove 18% North America order growth in Q1 and supported roughly $450 million in funnel wins

- Ovation converts its 74% Q1 order surge into H2 revenue, delivering on management’s mid-teens power growth guidance for fiscal 2026 and building backlog for 2027

- Software ACV reaches 10% plus growth for fiscal 2026, validating the path from $2.5 billion to $3.5 billion in software revenue by 2028 and supporting the multiple re-rating that the current price does not yet reflect

- Test and Measurement sustains high single-digit revenue growth through fiscal 2026, with book-to-bill above 1.0 building the backlog needed for a strong fiscal 2027 in semiconductor and aerospace

What Could Go Wrong

- China deteriorates beyond the modeled low-single-digit decline: 40% of Emerson’s roughly $1.8 billion China business is in chemical markets that have not recovered, and any further weakening compresses the segment margins that the 2028 roadmap depends on

- The software renewal accounting drag ($120 million full-year revenue headwind) combines with European project softness to push reported H1 growth below the level that sustains Street confidence in the H2 ramp, triggering multiple compression before the recovery reads through

- Middle East logistics disruption, flagged by COO Ram Krishnan at the JPMorgan Industrials Conference as a near-term watch item, extends into Q3 and delays project shipments from a region representing roughly 7% of total sales

- Margin execution disappoints: the 240 basis point EBITA margin expansion target by 2028 requires roughly 80 basis points of improvement per year, and any slippage in price/cost discipline or AspenTech synergy realization delays the path to the 30% margin target that justifies the 2028 EPS framework

Should You Invest in Emerson Electric Co.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up EMR stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Emerson Electric Co. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze EMR stock on TIKR for Free →