Key Stats for Centene Stock

- 52-Week Range: $25 to $64

- Current Price: $42

- Street Mean Target: $43

- Street High Target: $70

- Consensus: 3 Buys, 2 Outperforms, 13 Holds, 1 Underperform, 1 Sell

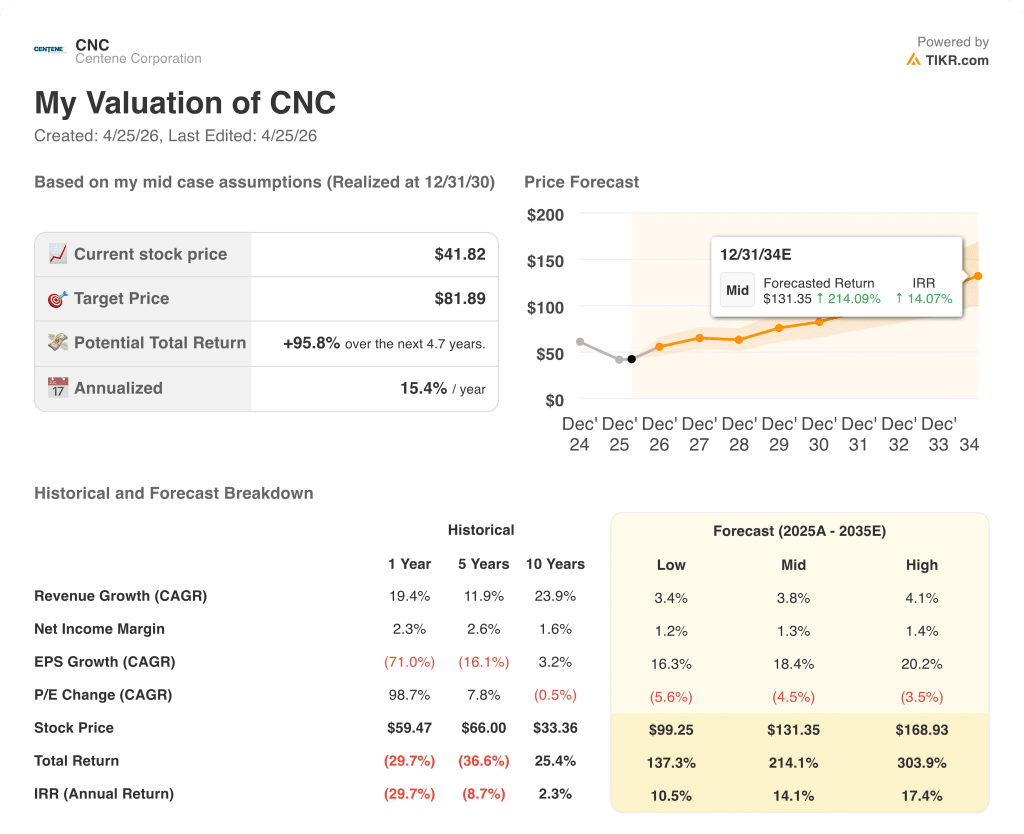

- TIKR Model Target (Dec. 2030): $82

What Happened?

Centene Corporation (CNC), America’s largest Medicaid managed care organization, closed 2025 with adjusted EPS of $2.08 and guided Wall Street to greater than $3 for 2026, a more than 40% year-over-year increase that resets expectations after one of the most turbulent years in managed care history.

The Q4 2025 earnings beat was the headline: Centene reported a Q4 adjusted EPS loss of $1.19, beating the Street estimate of -$1.22, on revenue of $49.725 billion, which exceeded estimates of $48.354 billion by roughly $1.4 billion and represented 21.86% year-over-year growth.

The operational story beneath those numbers matters more than the beat: Centene’s Medicaid Health Benefits Ratio (HBR, the share of premium revenue paid out in medical claims) improved to 93% in Q4 from a peak of 94.9% in Q2, representing 190 basis points of sequential improvement driven by aggressive fraud and utilization management across 29 states.

On April 6, the Centers for Medicare and Medicaid Services finalized a 2.48% Medicare Advantage payment rate increase for 2027, well above the 0.09% proposed in January and adding more than $13 billion in industry-wide payments, a sector-wide tailwind that sent Centene stock up roughly 5% on the day.

CEO Sarah London stated on the Q4 2025 earnings call that “we expect full year 2026 adjusted EPS to be greater than $3, representing more than 40% year-over-year growth and marking important progress toward restoring the enterprise’s embedded earnings power.”

Centene’s multi-year recovery path rests on three named pillars: Medicaid stabilization through mid-4% net trend assumptions and rate advocacy with state partners, Marketplace margin recovery toward a forecasted ~4% pretax margin (vs. a ~1% loss in 2025), and a Medicare Advantage trajectory toward breakeven by 2027 as the newly finalized CMS rate increase improves the business case.

Wall Street’s Take on CNC Stock

The 2025 collapse in Centene stock was real — the HBR deterioration, the Marketplace losses, and the Medicare drag were not invented — but the Q4 2025 recovery data shifts the forward picture in a way the current price has not yet absorbed.

CNC’s adjusted EPS of $2.08 in full-year 2025 is set to grow to greater than $3 in 2026, a more than 40% increase backed by three confirmed operational developments: Medicaid HBR sequential improvement from 95% to 93%, a mid-30% Marketplace repricing for 2026, and Medicare Advantage trending toward breakeven in 2027.

Seventeen analysts cover Centene stock, with 3 buys, 2 outperforms, 13 holds, 1 underperform, and 1 sell; the mean price target sits at $43.47, just 4% above the current price — a consensus that reflects waiting for proof on the Q1 2026 print scheduled for April 28, not a verdict on the full-year recovery.

The $32 to $70 target range among analysts reveals a genuine debate: the $70 bull camp assumes the Medicaid trend initiatives annualize as planned and the Marketplace margin recovery lands at the guided ~4% pretax, while the $32 bear camp prices in a scenario where Q1 2026 shows HBR re-acceleration and CMS rate finalization disappoints.

Trading at roughly 14x its guided 2026 EPS, Centene stock appears undervalued against a backdrop of accelerating per-share earnings growth in a sector where peers with equivalent or slower EPS trajectories routinely command 15x to 18x forward multiples.

At the Barclays Global Healthcare Conference on March 10, London reaffirmed greater than $3 adjusted EPS guidance with all three core business lines tracking to plan through February, adding a layer of in-year confirmation the initial guidance lacked.

If Medicaid HBR re-accelerates in Q1 2026 due to behavioral health or high-cost drug trends reversing the Q3-Q4 improvement, the 40% EPS growth thesis breaks and Centene stock re-rates toward the low end of the analyst range.

The April 28 Q1 2026 earnings release is the single confirmation event: a Medicaid HBR at or below 93.7% and an adjusted EPS figure tracking to the full-year >$3 target will signal that the recovery is structural, not seasonal.

What Does the Valuation Model Say?

With Centene’s guided 2026 adjusted EPS of greater than $3 representing a recovery from $2.08 in 2025, and the stock trading at roughly 14x that forward figure, the TIKR model’s implied target above current levels reflects the gap between a sector that has historically valued profitable MCO earnings at 15x to 18x and a price that still carries the discount of the 2025 crisis.

At 14x a confirmed greater-than-$3 earnings year, with Medicaid stabilizing, Marketplace recovering toward ~4% pretax margins, and Medicare Advantage trending toward 2027 breakeven, Centene stock is undervalued relative to the earnings power the operational data now supports.

The thesis hinges on one thing: whether the Q1 2026 Medicaid HBR confirms the sequential improvement is structural, or reveals that behavioral health and high-cost drug trends have not actually bent.

Bull Case

- Medicaid HBR at or below 93.7% in Q1 2026 would confirm the 190 basis point improvement from Q2 to Q4 2025 is carrying forward, not reversing

- The ABA task force, clinical management programs, and fraud detection initiatives deployed in H2 2025 are expected to annualize in 2026, representing trend mitigation that does not require additional state rate increases to deliver

- CMS finalized a 2.48% Medicare Advantage rate increase for 2027 (vs. 0.09% proposed in January), improving the economics for Centene’s path to MA breakeven and reducing the sector headwind that weighed on CNC stock throughout 2025

- Carolina Complete Health’s merger with WellCare of North Carolina, approved in April 2026, creates a provider-led organization serving 980,000 members and expands Centene’s dual-eligible footprint in a high-complexity, high-margin-recovery segment

- New leadership appointments (Daniel Finke as Group President, Markets and Commercial; Michael Carson as Group President, Medicare and Specialty) signal organizational investment in the two segments most critical to the 2026 earnings recovery

Bear Case

- 13 of 17 covering analysts hold-rated Centene stock as of April 24 — Wall Street is not positioned ahead of the recovery; any Q1 miss resets the narrative and triggers downside to the $32 analyst low target

- Marketplace membership is tracking down roughly 40% year-over-year to approximately 3.5 million members by end of Q1, and Bronze plan enrollment rising from 19-24% historically to over 30% introduces utilization uncertainty that won’t be resolved until Wakely claims data arrives in June

- Medicaid member months are guided down 5% to 6% in 2026, including the Florida CMS contract rolling off October 1, creating revenue headwinds that narrow the margin for error on the HBR recovery

- The No Surprises Act IDR litigation that added ~100 basis points to the Q4 2025 Marketplace HBR remains unresolved, and Centene has acknowledged taking an accrual for 2025 dates of service without full clarity on the forward exposure

- OB3 Medicaid work requirements, set to take effect January 2027, introduce a state-by-state eligibility contraction risk for the Medicaid population that makes 2027 membership assumptions highly uncertain, with meaningful visibility expected only in H2 2026

Should You Invest in Centene Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CNC stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Centene Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CNC stock on TIKR for Free →