Key Takeaways:

- FedEx Corporation is a global courier and logistics company that is spinning off its FedEx Freight division into a separately traded public company while transforming its cost structure under the DRIVE program.

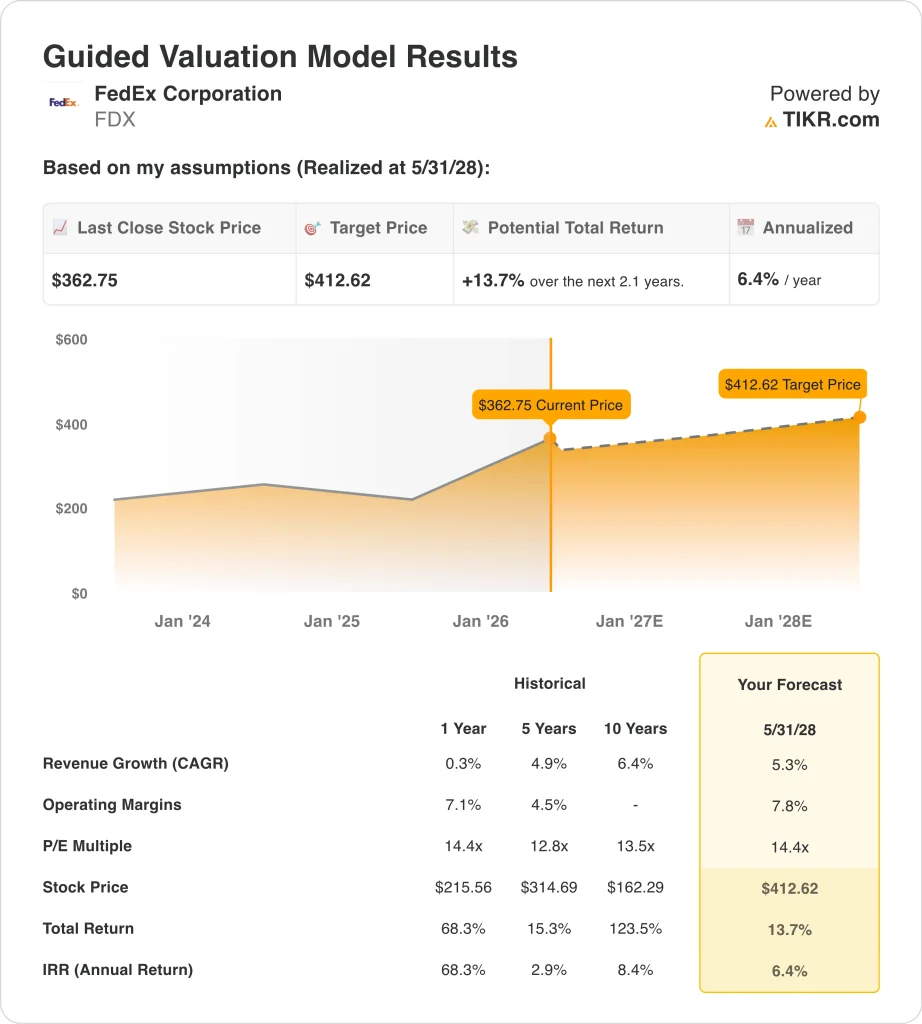

- FDX stock trades near $363, up about 71% over the past year, with a street consensus target of around $402.

- FDX stock could rise from $363 to around $413 per share by May 2028, based on 5.3% annual revenue growth, 7.8% operating margins, and a 14.4x P/E multiple.

- That would be a 13.7% total return, or around 6.4% annualized over the next 2.1 years.

What Happened?

FedEx Corporation (FDX) is a global courier and delivery services company with operations across express, ground, and freight segments. The company announced in 2024 that it would spin off its FedEx Freight division, a less-than-truckload (LTL) trucking unit, into a separately traded public company.

FedEx Freight filed its Form 10 registration statement in January 2026 and established its own board of directors ahead of the separation. The spin-off is central to FedEx’s broader DRIVE transformation, a multi-year cost reduction and network simplification program that management has pursued since fiscal 2023.

A new competitive threat emerged in early May 2026. Amazon opened its logistics network to third-party businesses, directly challenging UPS and FedEx for commercial delivery contracts. FDX and UPS shares fell on the news, but both companies responded quickly by pledging to return tariff refunds to customers.

FedEx also announced a new FedEx SameDay Local service and a collaboration with ServiceNow for AI-powered supply chain procurement. So the company continued investing in new capabilities even as competitive pressure grew.

FedEx reported Q3 fiscal year 2026 net income of $1.06 billion. FedEx Freight separately outlined medium-term revenue growth guidance of 4% to 6% CAGR ahead of the spin, providing investors with a clearer standalone financial picture.

CFO John Dietrich announced he will step down on June 1, 2026, adding a leadership transition for investors to monitor ahead of the Q4 FY2026 earnings report on June 23. Management maintained its full-year revenue growth guidance of 5% to 6% year over year, reflecting confidence in the core business.

Here’s why FedEx stock could still deliver returns as the Freight spin-off completes and the DRIVE program advances.

What the Model Says for FedEx Stock

We analyzed the upside potential for FedEx stock based on its ongoing cost transformation program, the value unlock expected from the FedEx Freight spin-off, and its global logistics network that continues to scale despite new competition from Amazon.

Based on estimates of 5.3% annual revenue growth, 7.8% operating margins, and a normalized P/E multiple of 14.4x, the model projects FedEx stock could rise from $363 to around $413 per share.

That would be a 13.7% total return, or a 6.4% annualized return over the next 2.1 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for FDX stock:

1. Revenue Growth: 5.3%

FedEx guided for fiscal year 2026 revenue growth of 5% to 6% year over year. The 1-year historical revenue growth is only 0.3%, but management’s transformation program and new services like FedEx SameDay Local support a better forward trajectory. Based on analysts’ consensus estimates, we used 5.3% revenue growth, consistent with the low end of the company’s own guidance.

The forward two-year revenue CAGR sits near 5.6% by analyst consensus, aligned with our model assumption. FedEx Freight’s own medium-term revenue CAGR guidance of 4% to 6% supports the idea that the broader network grows in a similar range. And new strategic partnerships, including the Viettel Post alliance in Vietnam, add diversified volume sources across international corridors.

The Amazon logistics threat is a near-term overhang, but FedEx maintains a global air network that Amazon cannot replicate quickly or economically. So the 5.3% revenue growth assumption is achievable even accounting for some commercial package volume competition from Amazon Logistics over the next two years.

2. Operating Margins: 7.8%

FedEx’s LTM EBIT margin is 7.9%, and the DRIVE program specifically targets cost consolidation and network optimization to sustain and improve this level. The company’s LTM gross margin of 27.6% reflects the asset-heavy nature of global logistics, but DRIVE-driven efficiencies have already lifted the EBIT margin materially from the 4.5% five-year average. Based on analysts’ consensus estimates, we used 7.8% operating margins, essentially flat with current levels as cost savings offset new competitive pressures.

A 7.8% margin is achievable but requires consistent execution as new competitive dynamics from Amazon unfold. The Freight spin-off will also clarify the margin profile of the remaining express and ground network, which could improve the optics of the core business for investors. And the AI-powered procurement partnership with ServiceNow may further reduce supply chain costs over time.

The CFO transition in June 2026 introduces some uncertainty around cost discipline continuity. But DRIVE is an institutional program rather than an individual effort, so the margin improvement trajectory should be durable. Investors should watch Q4 FY2026 earnings on June 23 for the first post-CFO data point on margins.

3. Exit P/E Multiple: 14.4x

FedEx trades at a next twelve-month P/E of 17.2x, above our 14.4x exit assumption. The five-year historical P/E of 12.8x and 10-year P/E of 13.5x show that FedEx has historically traded below 15x earnings. Based on analysts’ consensus estimates, we maintained a 14.4x exit P/E multiple, consistent with the long-run average and reflecting the ongoing transformation story without assuming a significant premium re-rating.

The 14.4x multiple implies some compression from today’s elevated LTM P/E of 19.3x as current strong sentiment moderates. But the combination of cost efficiency and global network scale could support sustained mid-to-high-teen multiples if execution continues. So the 14.4x is a grounded assumption that does not overstretch the valuation.

A 6.4% annualized return at the base case is below the 10% threshold many investors seek. But the high case scenario at 11.4% annual returns reflects the meaningful upside if DRIVE delivers above expectations and the Freight spin-off creates incremental unlocked value. And the FedEx brand and global infrastructure represent durable competitive assets that underpin the long-term investment case.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for FDX stock through 2030 show varied outcomes based on DRIVE transformation progress and competitive dynamics from Amazon (these are estimates, not guaranteed returns):

- Low Case: Amazon gains significant commercial market share and cost savings stall near current levels → 5.4% annual returns

- Mid Case: DRIVE program delivers sustained efficiency gains and Freight spin-off creates incremental value → 8.6% annual returns

- High Case: Cost transformation exceeds targets and new services scale faster than expected → 11.4% annual returns

Going forward, FedEx’s stock will be shaped by three concurrent stories: the completion and market reception of the FedEx Freight spin-off, the impact of Amazon’s logistics network on commercial package volumes, and the Q4 FY2026 earnings report in June that will set the tone for fiscal 2027 guidance.

The 71% gain over the past year already reflects strong sentiment, so the bar for positive surprises is elevated. Even in the mid case, returns near 8.6% annually are below what many investors target, suggesting FDX may appeal most to investors who value a stable global logistics franchise with a steady transformation story.

See what analysts think about FDX stock right now (Free with TIKR) >>>

Should You Invest in FedEx?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up FDX, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track FDX alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze FedEx stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!