Key Stats

- Current Price: $11 (May 5, 2026)

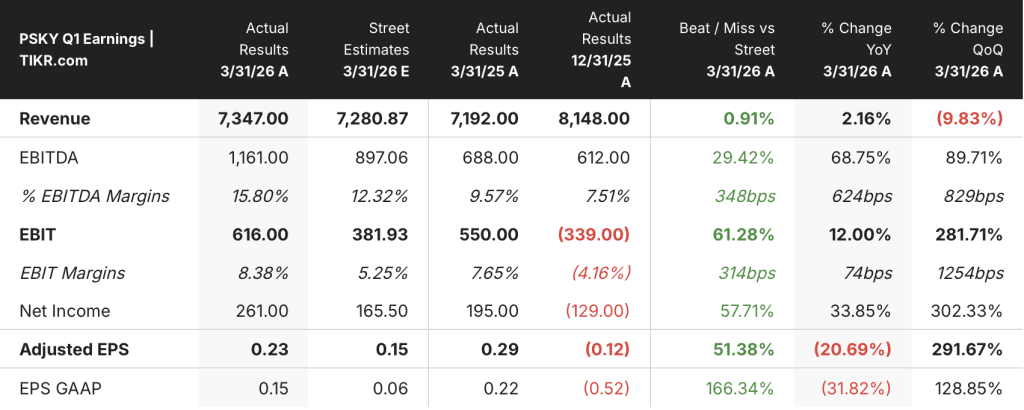

- Q1 2026 Revenue: $7.3B, up 2% YoY

- Q1 2026 Adjusted EPS: $0.23, down 21% YoY

- Q1 2026 EBITDA: $1.2B, up 69% YoY

- Paramount+ Revenue Growth: up 17% YoY (per CFO Dennis Cinelli on the Q1 2026 earnings call)

- Paramount+ Subscriber Adds: approximately 2 million underlying subscribers added in Q1

- Full-Year Revenue Guidance: second-half weighted growth; no specific full-year figure disclosed

- TIKR Model Price Target: $14

- Implied Upside: ~28%

Paramount Skydance Q1 2026 Earnings Breakdown

Paramount Skydance Corporation stock (PSKY) posted Q1 2026 revenue of $7.3B, up 2% year over year, while adjusted EPS of $0.23 came in ahead of internal expectations despite falling 21% from $0.29 in the prior-year quarter.

EBITDA of $1.2B surged 69% year over year, with EBITDA margin expanding to 16% from 10% in Q1 2025, as expenses ran lighter than planned on slower hiring pace and content timing shifts.

Paramount+ was the headline growth driver, with revenue up 17% year over year, according to CFO Dennis Cinelli on the Q1 2026 earnings call, driven by a 14% increase in ARPU from a January price increase and improvement in subscriber mix.

Underlying subscriber additions reached approximately 2 million in the quarter, though net reported adds of 700,000 reflect the deliberate exit of more than 1 million low-value international hard bundle subscribers, which Cinelli noted carried average ARPU below $1.

Studio revenue grew 11% in Q1, according to Cinelli on the Q1 2026 earnings call, supported by the theatrical release of Scream 7, which became the highest-grossing film in the franchise’s 30-year history, and continued build-out of the third-party TV studio.

UFC content on Paramount+ drew more than 10 million households watching over 100 million hours in the quarter, according to CEO David Ellison on the Q1 2026 earnings call, with new UFC subscribers averaging 15 years younger than the broader Paramount+ viewer base.

Overall advertising declined 3% in Q1, though management said the D2C advertising business returned to growth in the quarter, and Cinelli stated the expectation that total company ad revenue will return to growth in the back half of 2026.

Paramount Skydance Stock: What the Income Statement Shows

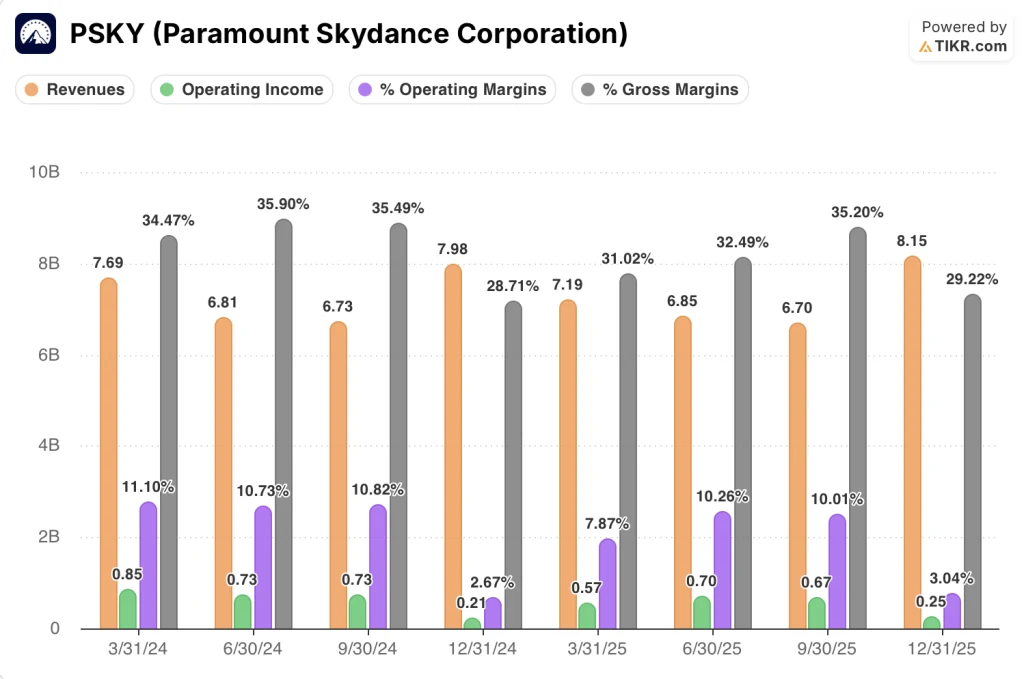

Paramount Skydance stock’s income statement reflects a recovery arc after six quarters of revenue pressure, with operating leverage now catching up to the top-line stabilization.

Revenue peaked at $7.7B in Q1 2024 before declining through Q2 and Q3 2024, briefly recovering to $8.0B in Q4 2024, then sliding again to $6.7B in Q3 2025, the weakest quarter in the trailing eight-period window.

Q1 2026’s $7.3B represents the clearest YoY growth quarter since Q4 2024, and the sequential recovery from $6.7B in Q3 2025 suggests the trough is behind the business.

Operating income bottomed at $210M at a 3% operating margin in Q4 2024, recovered to $570M in Q1 2025, then compressed again through Q3 and Q4 2025 before rebounding to $616M in Q1 2026 at an 8% operating margin.

The EBITDA trajectory confirms the direction: $688M in Q1 2025 rising to $1.2B in Q1 2026, a 69% year-over-year gain driven by lighter-than-planned hiring costs and favorable content timing, according to CFO Dennis Cinelli on the Q1 2026 earnings call.

Gross margin has tracked the same pattern, expanding from 31% in Q1 2025 to a high of 35% in Q3 2025 before compressing to 29% in Q4 2025 on heavier content costs.

What Does the Valuation Model Say?

The TIKR model prices Paramount Skydance stock at $13.69, implying roughly 28% upside from the current price of approximately $11.

The mid-case assumptions are conservative: revenue CAGR of 2.5% through 2035 and a net income margin of 3.7%, reflecting a business that is expected to grow slowly while gradually rebuilding profitability after years of margin erosion.

Q1’s EBITDA outperformance and the UFC subscriber data give early credibility to the monetization side of the model, but the 21% YoY decline in adjusted EPS and the continued YoY operating income near-stagnation suggest the net income margin recovery will take time.

The investment case is modestly stronger after this quarter: Paramount+ is scaling, the balance sheet work for the Warner Bros. Discovery transaction is done, and cost discipline is showing up in the numbers.

Q1 showed tangible operational momentum, but the investment argument for Paramount Skydance stock ultimately depends on whether the Warner Bros. Discovery combination closes on schedule and delivers the scale economics management is projecting.

Near-Term

- Q1 EBITDA of $1.2B at a 16% margin beat expectations and showed meaningful progress from $688M and a 10% margin in Q1 2025

- Paramount+ underlying subscriber adds of approximately 2 million were achieved despite exiting low-ARPU international bundles, demonstrating healthy organic demand

- UFC advertising exceeded expectations in Q1, adding a high-margin revenue stream that did not exist in the prior-year base

- Platform convergence of Paramount+, Pluto, and BET+ is on track for mid-2026, which should reduce technology costs and improve personalization metrics

Long-Term

- Revenue CAGR of 2.5% in the TIKR mid case reflects a business with limited organic growth potential; the upside model depends on post-WBD scale efficiencies and subscriber acceleration that have not yet been demonstrated

- Adjusted EPS of $0.23 in Q1 2026 fell 21% from $0.29 in Q1 2025, despite revenue growth, indicating that content and tech investment is still dilutive to per-share earnings

- The WBD transaction is projected to close by September 2026 per Ellison on the Q1 2026 earnings call, but integration of two large media companies carries execution risk that could pressure margins beyond the model’s 3.7% net income margin assumption

- Q4 2025 operating income fell to $250M at a 3% operating margin before the Q1 recovery, a reminder that seasonality and content timing can compress results sharply even in improving businesses

Should You Invest in Paramount Skydance Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Paramount Skydance Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Paramount Skydance Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze PSKY stock on TIKR for Free →