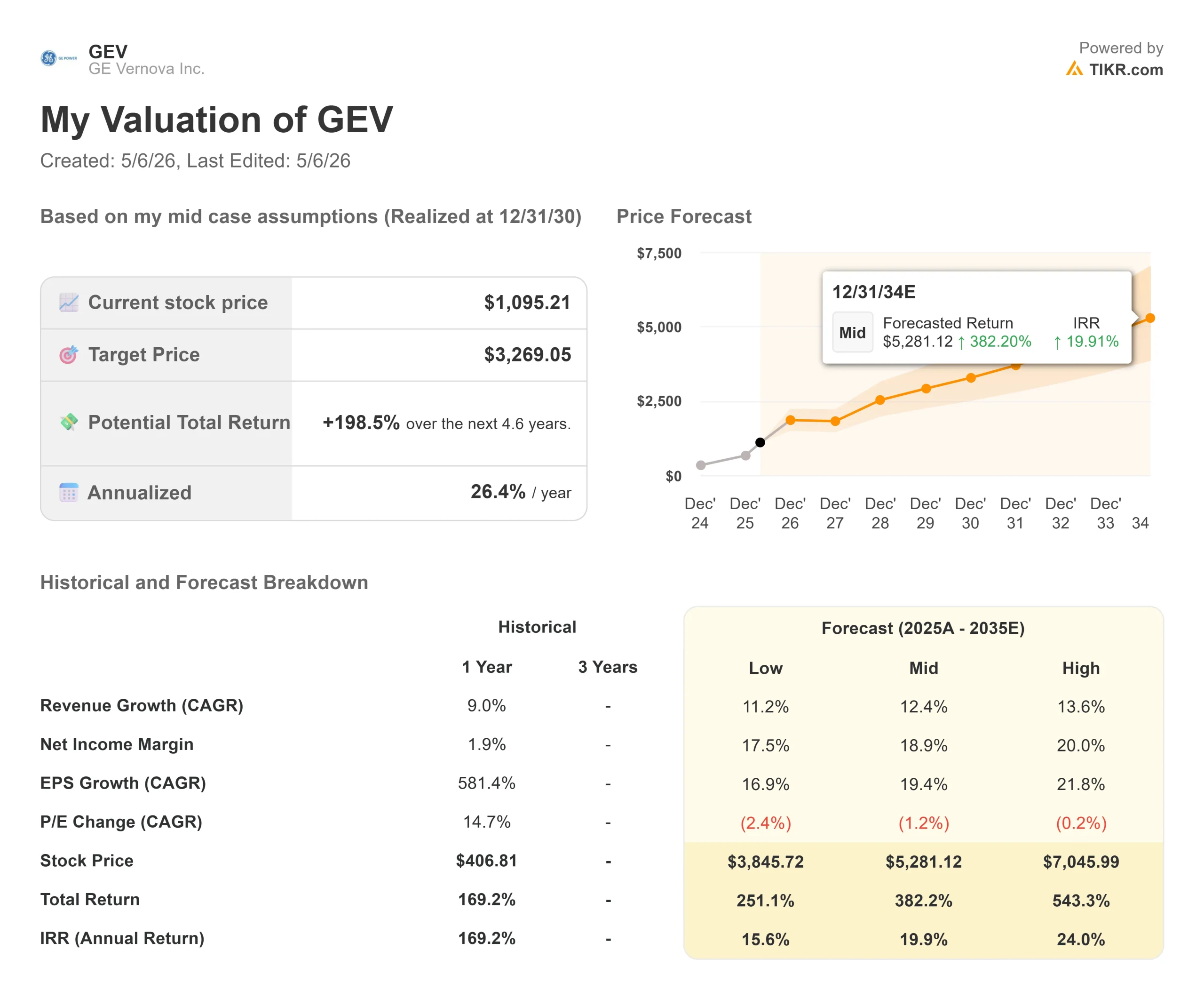

Key Stats for GE Vernova Stock

- Current Price: $1,095.21

- Target Price (Mid): ~$3,269

- Street Target: ~$1,207

- Potential Total Return: ~199%

- Annualized IRR: ~26% / year

- Earnings Reaction: +1.95% (April 22, 2026)

- Max Drawdown: 17.54% (November 4, 2025)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

GE Vernova (GEV) delivered one of the strongest quarters in its short history as a public company, and investors responded. The stock rose +1.95% on April 22, the day earnings dropped, then gained roughly 14% over the full week, touching an all-time high of $1,181.95 on April 23 before pulling back to $1,095.21. Bulls point to a $163 billion backlog growing faster than analysts expected, with pricing accelerating and a free cash flow profile that already outpaced all of 2025 in a single quarter. Bears point to a stock trading at 40x NTM EV/EBITDA, more than double the sector median, where any execution slip carries real valuation risk. The central question: Is the backlog repricing fast enough to justify that premium today?

What Q1 2026 Actually Delivered

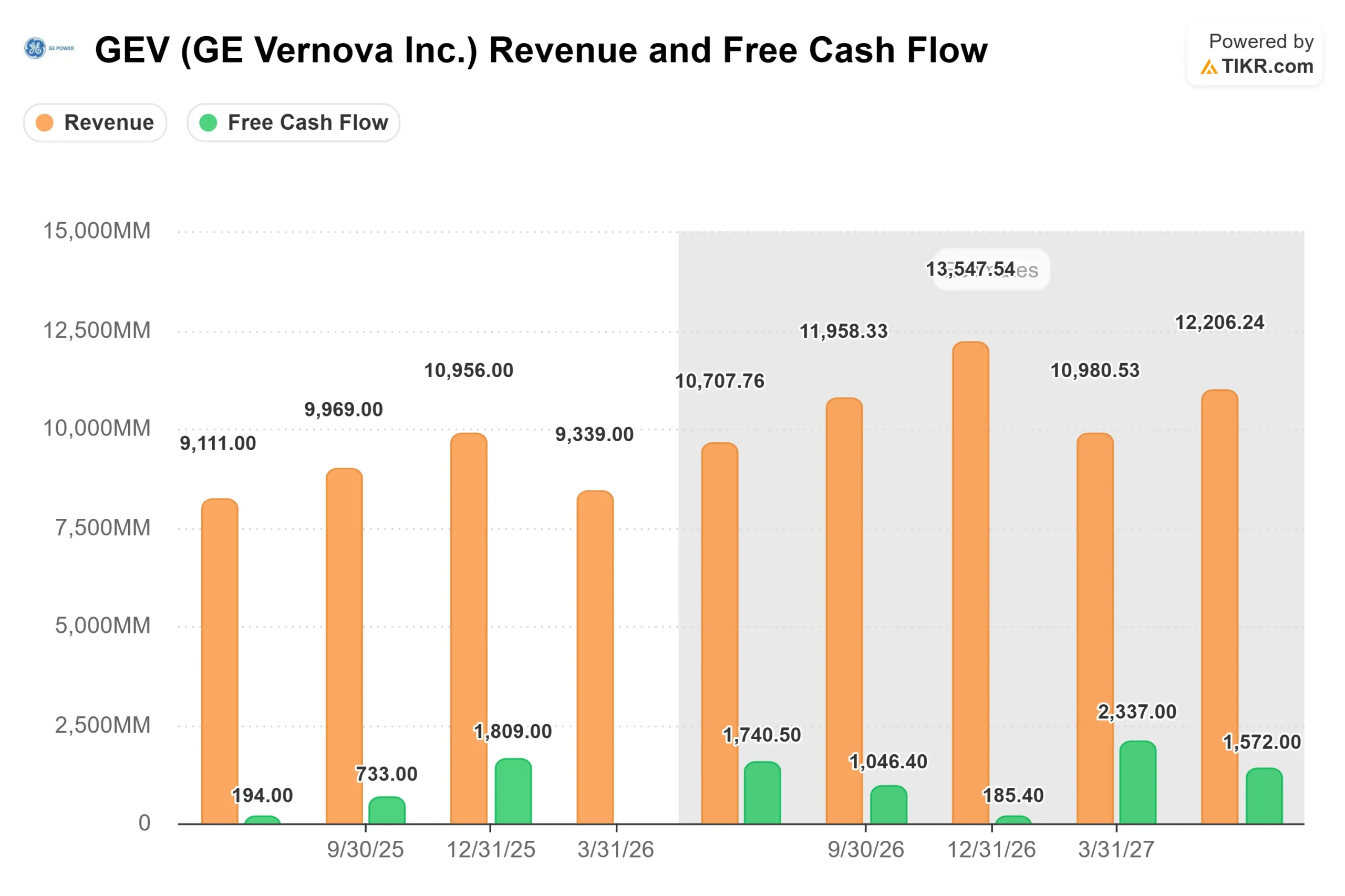

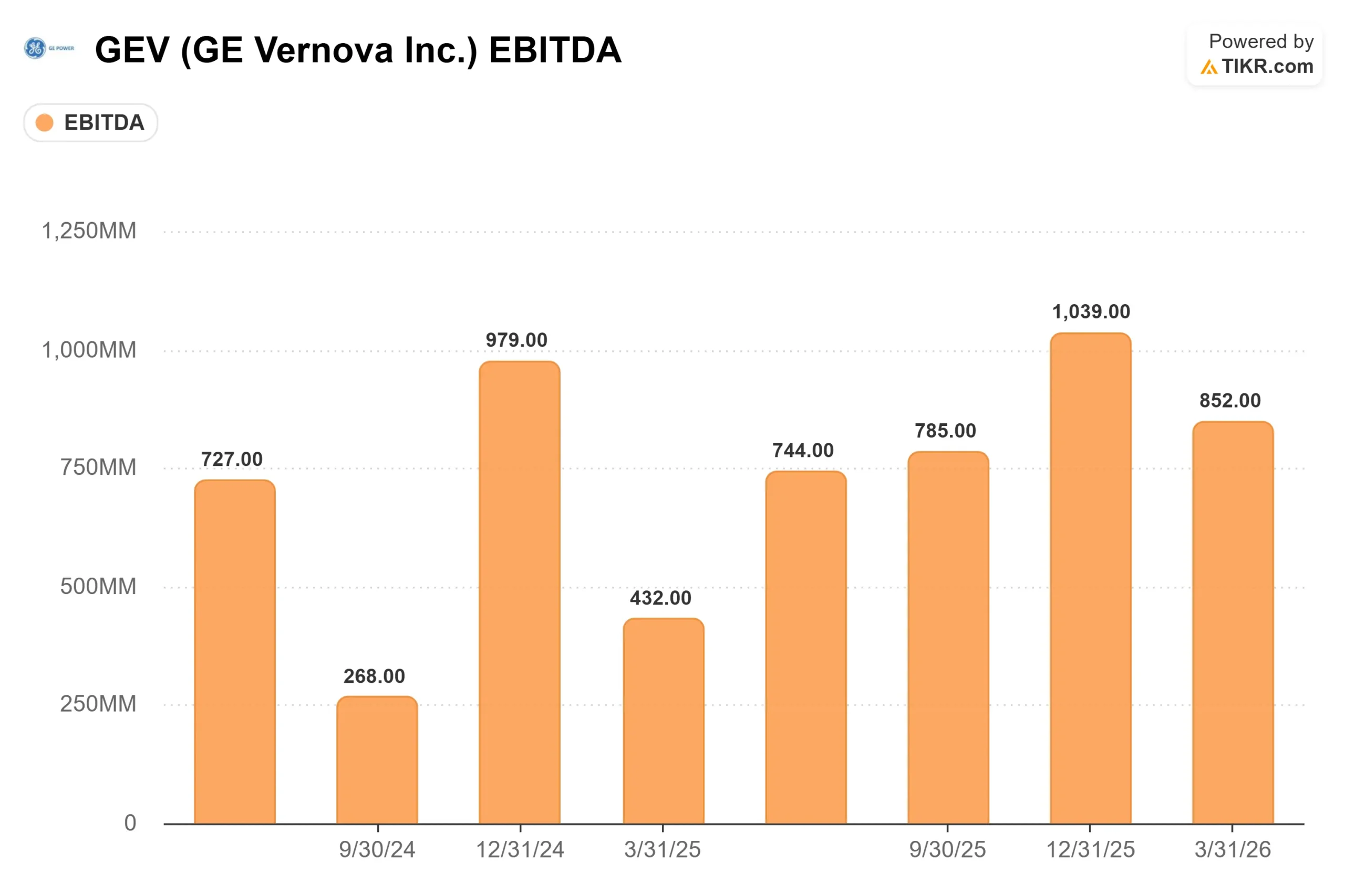

Revenue came in at $9.339 billion against a $9.251 billion consensus estimate. Adjusted EPS of $2.01 beat the $1.67 estimate by 20.4%. Adjusted EBITDA grew 87% year-over-year to $896 million, with margins expanding 390 basis points.

The standout figure was free cash flow: GE Vernova produced $4.8 billion in Q1 alone, exceeding the $3.7 billion it generated in all of fiscal 2025. That result was driven primarily by down payments on surging equipment orders and slot reservation agreements (SRAs) deposits customers pay upfront to secure future turbine delivery slots.

Orders told the bigger story. GE Vernova booked $18.3 billion in Q1, up 71% year-over-year, with equipment orders more than doubling and a book-to-bill ratio of approximately 2x, meaning it is booking twice as much business as it is shipping. Total backlog grew to $163 billion from $116 billion at the time of the company’s spin from General Electric in April 2024.

CEO Scott Strazik stated on the April 22 earnings call: “In the last 90 days, we’ve added $13 billion to our total backlog and now expect to reach $200 billion in backlog in ’27 versus our previous expectation of ’28.” That pulled a key milestone forward by a full year. Management raised full-year 2026 guidance: revenue to $44.5–$45.5 billion (up $500 million from prior guidance), adjusted EBITDA margin to 12%–14% (up 1 point at both ends), and free cash flow to $6.5–$7.5 billion (up from $5.0–$5.5 billion).

See historical and forward estimates for GE Vernova stock (It’s free!) >>>

Three Segments, Two Engines Firing

Power delivered EBITDA margin expansion of 500 basis points to 16.3% in Q1, with revenue up 10% and 25 gas turbines shipped, a 32% increase year-over-year. Gas Power now has 100 gigawatts under contract across 90 customers in 24 countries, with 20% directly tied to data centers. Orders signed in the first half of 2026 are priced 10 to 20 percentage points higher on a dollar-per-kilowatt basis than the Q4 2025 backlog. That pricing uplift has not yet appeared in revenue; it will as those orders convert through 2027 and 2028. For Q2 2026, management guided Power revenue growth of 15%–17% and EBITDA margin of approximately 17%–18%.

Nuclear added two concrete catalysts. At OPG’s Darlington site in Canada, the first SMR (small modular reactor a compact, faster-to-build nuclear plant) under construction in North America cleared a key regulatory milestone, with installation of the foundational 2-million-pound base mat approved to begin. Separately, the U.S. and Japanese governments announced up to $40 billion in support for GE Vernova Hitachi to build BWRX-300 SMRs in Tennessee and Alabama, part of a broader $550 billion bilateral investment framework. No U.S. SMR has yet been connected to the grid, and timelines remain subject to regulatory and financing risk. GE Vernova also expects the Nuclear Regulatory Commission to issue a construction license for the Clinch River site in Tennessee as soon as the second half of 2026.

Electrification generated the most investor attention. Orders hit $7.1 billion, up 86% year-over-year, with North American and Asian equipment orders roughly tripling. The key data point: the Electrification segment booked $2.4 billion in data center-related equipment orders in Q1 alone, more than its entire 2025 data center total in a single quarter. EBITDA margin expanded 590 basis points to 17.8%. The Prolec GE transformer acquisition, which closed in February 2026, contributed nearly $500 million in revenue at just over 20% EBITDA margin, with Prolec’s backlog growing 25% since the transaction was announced, to $5 billion.

GE Vernova is also moving inside the data center fence. It closed its first energy management system (EMS) order in Q1, combining substation equipment, gas power equipment, and software to manage power load requirements for a hyperscaler customer, and secured a second EMS order in April. Strazik described the strategy on the call: “When you are doing the power generation, the substation equipment, and you’re providing a lot of the software solutions to help the hyperscaler manage the load requirements they want with our equipment, it’s giving you the enablement to then attach more LEGO blocks.”

Wind remains a drag. EBITDA losses were $382 million in Q1, in line with management’s expectations, driven by lower onshore equipment deliveries and higher offshore contract losses. The U.S. onshore market is soft due to permitting delays and tariff uncertainty. For Q2, Wind revenue is expected to decline at a mid-teens rate, with EBITDA losses of $200–$300 million. Full-year Wind EBIT loss guidance of approximately $400 million held steady. Roughly 70% of 2026 onshore turbine shipments are expected in the second half of the year. On tariffs, CFO Ken Parks confirmed on the call: “Where we sit today, that outlook for $250 million to $350 million is fully built in our outlook.”

See how GE Vernova performs against its peers in TIKR (It’s free!) >>>

Is the Premium Justified?

GE Vernova trades at an NTMEV/EBITDA of 40.04x. On TIKR’s Competitors page, ABB trades at 22.91x, Siemens Energy at 19.69x, and Schneider Electric at 17.41x, with the sector median at approximately 17x. GE Vernova trades at more than double that median.

The bull case rests on two dynamics that the multiple alone does not capture. First, the backlog is repricing: orders booked in the first half of 2026 carry pricing 10 to 20 points above the existing backlog on a dollar-per-kilowatt basis, margin expansion that is already locked in through signed contracts, not forecasts. Second, services compound the upside. CFO Ken Parks confirmed on the earnings call that GE Vernova’s services backlog grew 12% year-over-year to $87 billion in Q1. GE Vernova holds the largest installed base of gas turbines of any OEM (original equipment manufacturer) in the world, and every turbine shipped today adds to a services book that compounds well into the 2030s.

The bear case is equally clear. At 40x NTM EV/EBITDA, there is limited tolerance for Wind losses to deepen, tariff exposure to breach $350 million, or the back-half gas turbine production ramp to slip. R&D and capital expenditures combined are expected to rise approximately 30% year-over-year in 2026. The company issued $2.6 billion in debt in Q1, though it maintains a strong investment-grade rating and roughly $10.2 billion in cash.

TIKR Advanced Model Analysis

- Current Price: $1,095.21

- Target Price (Mid): ~$3,269

- Potential Total Return: ~199%

- Annualized IRR: ~26% / year

See analysts’ growth forecasts and price targets for GE Vernova stock (It’s free!) >>>

The TIKR mid-case uses a revenue CAGR of approximately 12% through 12/31/30, driven by Gas Power equipment and services growth as production capacity scales toward 20 GW annually by mid-2026 and 24 GW by 2028, and by Electrification’s expanding data center and grid infrastructure backlog. Net income margin is projected to reach approximately 19% under the mid case, up from 1.9% in the trailing twelve months, as Wind losses shrink and Electrification achieves operating leverage on its $39 billion equipment backlog. The primary risk to this model is Wind: a full-year EBIT loss of approximately $400 million in 2026, and any deepening of offshore contract losses or tariff-driven erosion could pull the margin trajectory lower.

Conclusion

The metric to watch at GE Vernova’s next earnings report, expected July 23, 2026, is Gas Power equipment orders in gigawatts for Q2 2026. Management guided for 10 to 15 GW of contracts. If that range is met or exceeded, it confirms that pricing and demand are sustaining even as slot availability tightens into 2029 and 2030. If it falls short, the 40x multiple faces direct pressure. GE Vernova holds the largest gas turbine installed base, the deepest electrification backlog, and a nuclear pipeline backed by up to $40 billion in government support, but the price already reflects a great deal of that story.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in GE Vernova?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up GE Vernova, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track GE Vernova alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze GE Vernova on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!