Key Stats for PM Stock

- Current Price: $169.46

- 52-Week Range: $142.11 to $191.30

- Street Mean Target: ~$192

- TIKR Model Target Price: ~$240

- Implied Upside (TIKR): ~42%

- Dividend Yield: 3.6%

Assess whether Philip Morris stock’s current price already capitalizes on its smoke-free transition by modeling cash flow scenarios on TIKR for free →

The Quarter Was Strong. One Data Point Made It Historic.

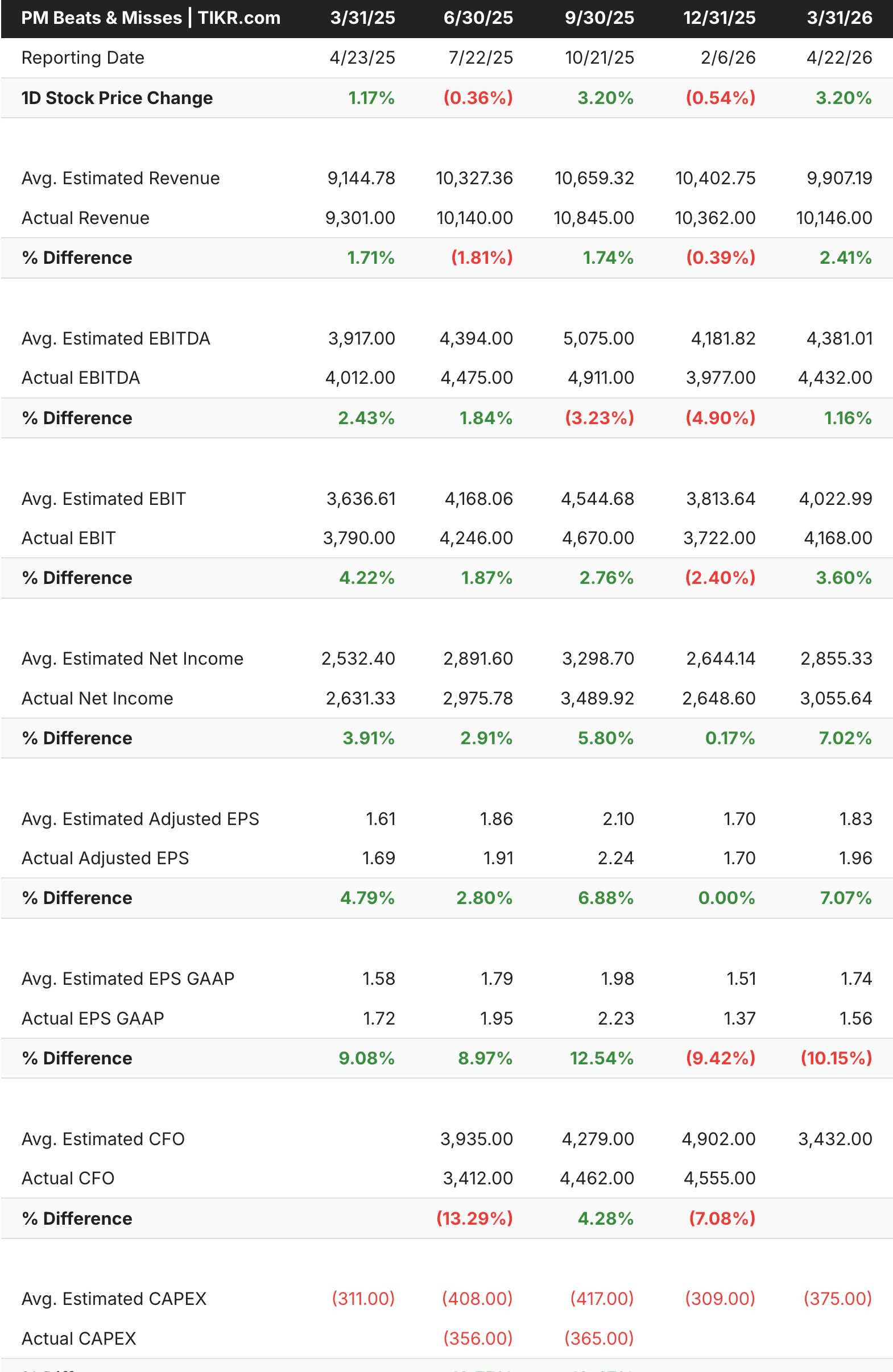

Philip Morris (PM) reported Q1 2026 results on April 22nd that came in well ahead of Street expectations. Revenue of $10.1 billion grew 9.1% year over year and beat estimates by around 2%. Adjusted EPS of $1.96 grew 16% versus the prior year and beat by around 7%. The company raised full-year adjusted EPS guidance to $8.36 to $8.51, implying growth of roughly 11 to 13% versus 2025. The stock rose over 3% on the day.

The headline number was strong, but one detail stood out above all else: IQOS, Philip Morris’s heated tobacco device, surpassed Marlboro to become the number-one nicotine brand by volume in the markets where both compete. IQOS now holds about 77% of the global heat-not-burn category, and in Q1 it reached nearly 11% of combined cigarette and heated tobacco industry volumes in its key markets.

That is not a rounding error in a product transition. It is a structural shift in what the business actually is.

Adjusted EPS has beaten estimates in every single quarter shown in the table, with the beat widening from around 5% a year ago to over 7% in the most recent period. Revenue has been more mixed, though Q1 2026 delivered the strongest beat in the trailing five quarters.

The one area of noise was the US smoke-free segment, where ZYN shipments declined 23.5% to 2.3 billion pouches due to distributor-level inventory normalization. Underlying consumer demand, measured by Nielsen offtake, still grew around 10% in the quarter. Management expects the shipment comparison to normalize in the second half of the year.

Compare Philip Morris stock’s valuation assumptions against British American Tobacco and Altria using consistent margin inputs on TIKR for free →

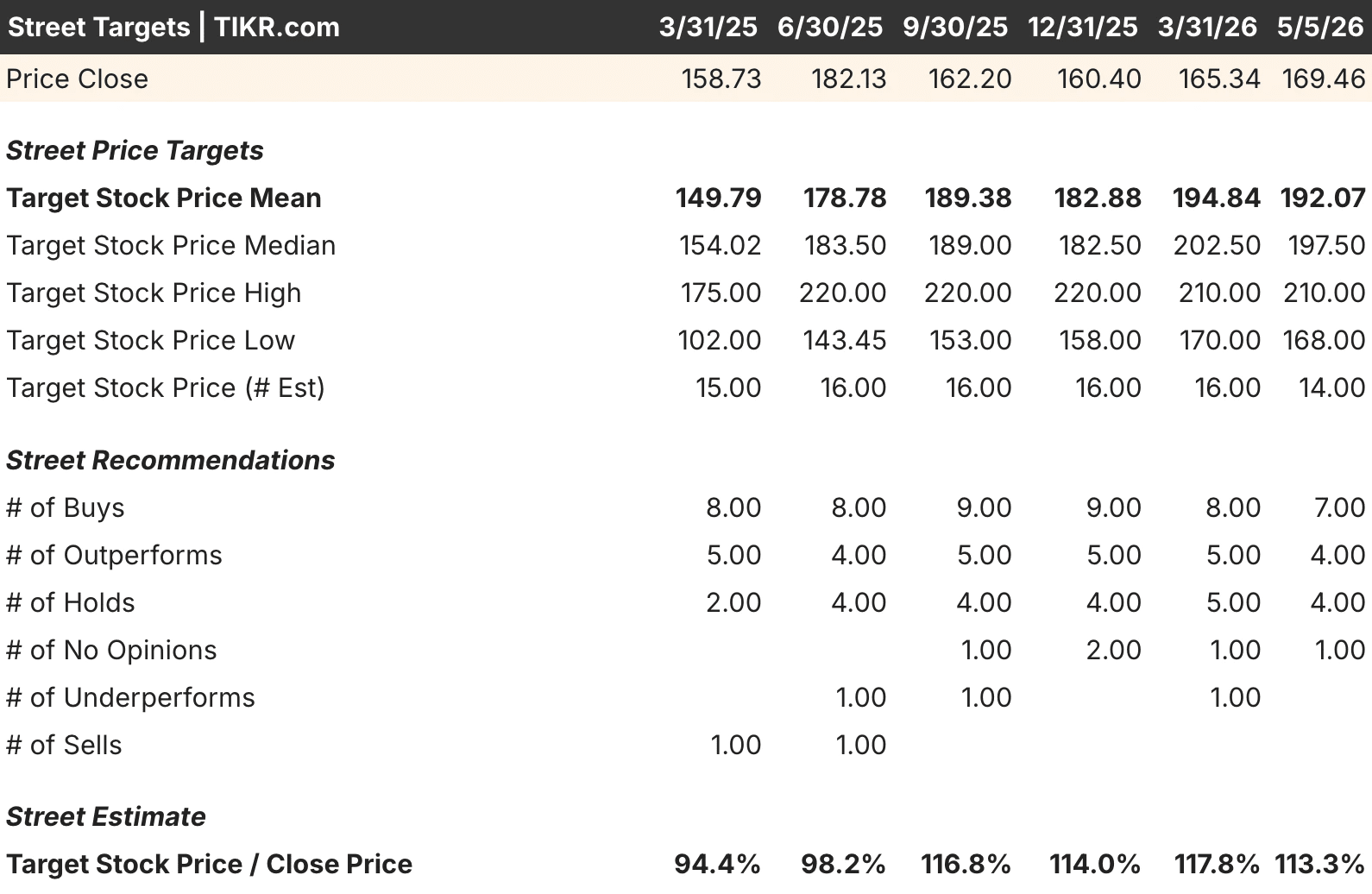

Eleven of Fourteen Analysts Are Bullish, The Stock Still Trades Below Their Mean Target

With 7 buys, 4 outperform, and 4 holds among the 14 analysts currently covering PM, the community is broadly positive on Philip Morris. The mean price target sits around $192 against a current price of $169, a gap of roughly 13% just to street consensus. For a mega-cap consumer staples company, that kind of discount to analyst consensus is not common.

What makes the street targets table particularly useful here is the trajectory. The mean target has moved from around $150 a year ago to $192 today as IQOS volumes and ZYN penetration have continued building, and Q1 results did nothing to dent that trend.

The low target for the current period is $168, essentially where the stock is trading, which means even the most cautious analyst on the Street sees minimal further downside. The high target of $210 reflects what the bull case looks like if the smoke-free transition continues compounding at its current rate.

Estimate a company’s fair value instantly (Free with TIKR) >>>

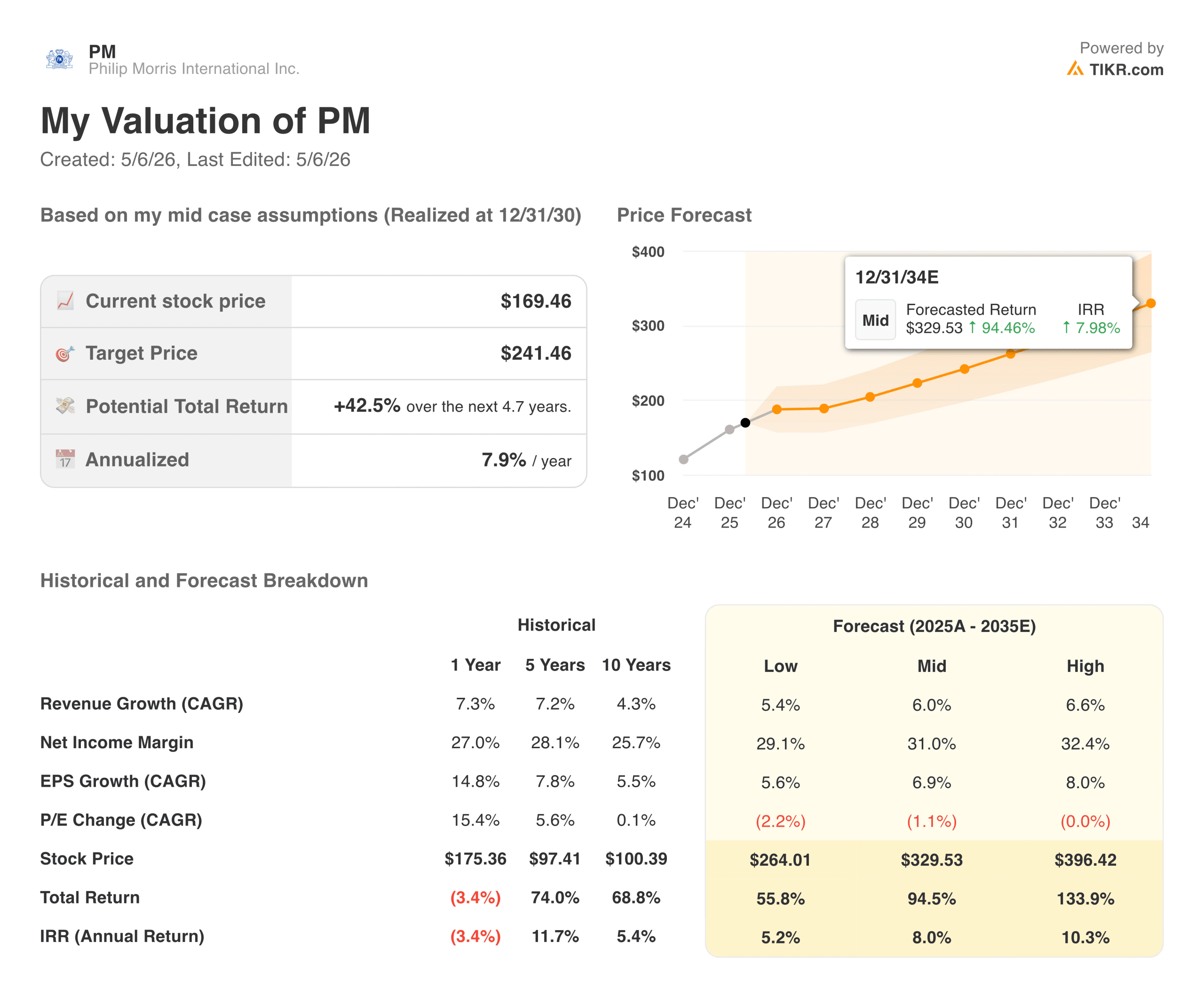

What Does the Path to $240 Actually Look Like From Here?

TIKR’s valuation model targets a PM stock price of around $240, implying a total return of roughly 42% over about five years, or about 8% annualized. Combined with the 3.6% dividend yield, the total annual return in the mid-case approaches 11-12% for a business with low cyclicality and genuine pricing power.

The assumptions behind that target are not aggressive. Revenue growing around 6% annually, net income margins expanding toward 31%, and EPS compounding near 7% per year. Mild P/E compression is built in, so the model is not relying on a re-rating. It is simply projecting a business that keeps doing what it has been doing.

What the Bulls Are Betting On:

- The smoke-free transition still has years of runway. Smoke-free products represented 43% of total Q1 revenues, up from a much smaller base just a few years ago. As that mix continues to shift, the margin profile of the consolidated business improves, since smoke-free products deliver more than twice the gross profit per unit than traditional cigarettes.

- IQOS is a genuinely dominant platform. Holding 77% of the global heat-not-burn category and now surpassing Marlboro in its key markets is the kind of competitive position that takes decades to replicate. The moat here is product differentiation, brand equity, and regulatory authorization in market after market.

- ZYN’s underlying demand is healthy. The Q1 shipment decline was a distributor-inventory story, not a consumer-demand story. Offtake grew around 10%, ZYN Ultra is pending FDA review, and management expects shipments to normalize in H2 2026 as comparisons ease.

- The dividend is durable and growing. With a 3.6% yield, a payout ratio of around 79%, and consistent free cash flow generation, PM offers one of the more reliable income streams in large-cap equities.

What the Bears Are Watching:

- Cigarette volume declines are structural. Even as smoke-free products grow, traditional cigarette volumes continue to decline across most markets. If that decline accelerates beyond what pricing can offset, the revenue trajectory softens.

- Regulatory risk is real and ongoing. Any meaningful shift in how governments regulate nicotine products, whether IQOS, ZYN, or e-vapor, can disrupt the growth assumptions embedded in the model. The FDA review process for ZYN Ultra is a near-term example.

- The balance sheet carries meaningful debt. With net debt of around $46.5 billion and 2.45x EBITDA, PM operates with more leverage than many of its large-cap peers. Dividends and organic investment take priority over debt reduction, so leverage remains elevated.

- The US ZYN business faces real competition. The nicotine pouch market is attracting aggressive competitors, and the gap between ZYN’s premium positioning and lower-priced alternatives is being tested. Management is committed to defending the premium, but the dynamic bears watching.

Should You Invest in Philip Morris

Philip Morris is a business in the middle of one of the more remarkable product transitions in consumer history, and Q1 2026 results suggest that transition is progressing faster than the stock price implies. The IQOS milestone alone, overtaking Marlboro in combined nicotine volume in its key markets, is the kind of inflection point that tends to look obvious in hindsight and underappreciated in real time.

At $169 with a 3.6% dividend, a street mean target around $192, and the TIKR model pointing toward $240 at roughly 8% annualized before dividends, the risk-reward here is genuinely interesting for patient investors. The ZYN shipment noise in Q1 will resolve itself as inventory normalizes, the IQOS growth trajectory is intact, and the full-year guidance raise signals management has real visibility into the back half.

The next earnings report arrives in late July, and the key things to watch are ZYN shipment recovery in the US as inventory headwinds clear, continued IQOS adjusted IMS growth, and whether organic revenue growth holds near the mid-single-digit range. If those trends stay on track, the gap between today’s price and what both the Street and the TIKR model value this business at will become increasingly hard to justify.

Benchmark Philip Morris stock’s expected returns against global consumer staples peers using identical growth and margin inputs on TIKR for free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!