Key Takeaways:

- Profit Outlook Reset: Philip Morris raised 2026 EPS growth to 11% to 13% as smoke-free products exceeded 40% of revenue, reinforcing Philip Morris International’s shift away from combustible volume dependence.

- Category Pressure Signals: Philip Morris flagged rising competition in U.S. nicotine pouches as ZYN volumes rose 19% while revenue declined.

- Valuation Anchor: Based on 7% revenue growth, 41% operating margins, and a 20x exit multiple, Philip Morris International stock could reach $220 by December 2028.

- Return Math: From the current price of $183, Philip Morris International implies 20% total upside over 3 years, translating to a 7% annualized return under conservative valuation assumptions.

Philip Morris International Inc. (PM) generates revenue from cigarettes and smoke-free products across more than 100 markets, monetizing consumer demand through pricing power, scale, and a growing portfolio of reduced-risk alternatives.

Last year, Philip Morris generated $41 billion in revenue and $27 billion in gross profit.

Meanwhile, PM stock’s operating income reached $15 billion as margins recovered to 37% despite elevated investment.

Current management is also extending its multi-year transition strategy.

CEO Jacek Olczak on earnings call stated, “we are renewing these growth targets for the next 3 years,” framing capital allocation and innovation priorities through 2028.

The valuation model implies $220 value at 20x, but a 7% annualized return from $183 limits equity upside despite durable cash generation.

What the Model Says for PM Stock

Philip Morris International’s smoke free portfolio strength is offset by capital intensity that limits incremental growth and return expansion.

The valuation framework embeds 7.3% revenue growth, 40.7% operating margins, and a 19.5x exit multiple, translating into a $220.11 implied target price.

The resulting 20.4% total upside equates to a 6.6% annualized return, falling short of compensation typically required for equity risk.

The model delivers a Sell signal because a 6.6% annualized return does not meet risk adjusted return requirements.

A 6.6% annualized return versus a standard 10% equity hurdle favors capital preservation over appreciation, leaving valuation support insufficient and justifying a Sell under disciplined capital allocation logic.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for PM stock:

1. Revenue Growth: 7.3%

Philip Morris International has delivered consistent top line expansion as smoke free products offset cigarette volume decline, with 1 year revenue growth at 7.3% reflecting category mix improvement rather than cyclical rebound.

Current execution is supported by smoke free volume growth in the low teens and pricing discipline, sustaining a 7.3% revenue growth outlook despite competitive pressure in nicotine pouches and heated tobacco.

Forward performance depends on maintaining smoke free adoption rates and pricing power, while regulatory friction, inventory normalization, or share losses would quickly compress revenue growth below modeled levels.

According to consensus analyst estimates, revenue growth is in line with the 1 year historical rate of 7.3%, indicating the model assumes stable demand durability rather than acceleration, leaving limited buffer if smoke free momentum softens.

2. Operating Margins: 40.7%

Philip Morris International has historically generated strong profitability, with a 1 year operating margin of 38.8% reflecting premium pricing, scale benefits, and declining cost intensity from smoke free products.

Current margins are supported by mix shift toward higher margin smoke free categories and ongoing cost control, allowing operating margins to approach 40.7% despite continued commercial investment.

Sustaining margin expansion requires disciplined pricing, favorable mix, and controlled promotional spend, while competitive responses or regulatory costs would pressure profitability quickly.

Based on street consensus estimates, operating margins are above the 1 year historical level of 38.8%, indicating the model assumes incremental efficiency gains that leave valuation exposed if reinvestment needs rise.

3. Exit P/E Multiple: 19.5x

Philip Morris International has traded at elevated multiples during periods of earnings visibility, with a 1 year historical P/E of 21.0x reflecting confidence in smoke free transition and cash flow durability.

The selected 19.5x exit multiple capitalizes mature earnings with moderate growth, recognizing business stability while avoiding reliance on multiple expansion beyond current expectations.

Future valuation depends on sustained earnings growth and regulatory clarity, while any disruption to smoke free economics would compress the multiple rather than support re rating.

As reflected in consensus expectations, the 19.5x exit multiple is below the 1 year historical multiple of 21.0x, indicating the model assumes valuation normalization consistent with a mature, cash generative business profile.

What Happens If Things Go Better or Worse?

Philip Morris International stock outcomes depend on smoke-free adoption pace, pricing discipline, and regulatory stability, setting up a range of possible paths through 2030.

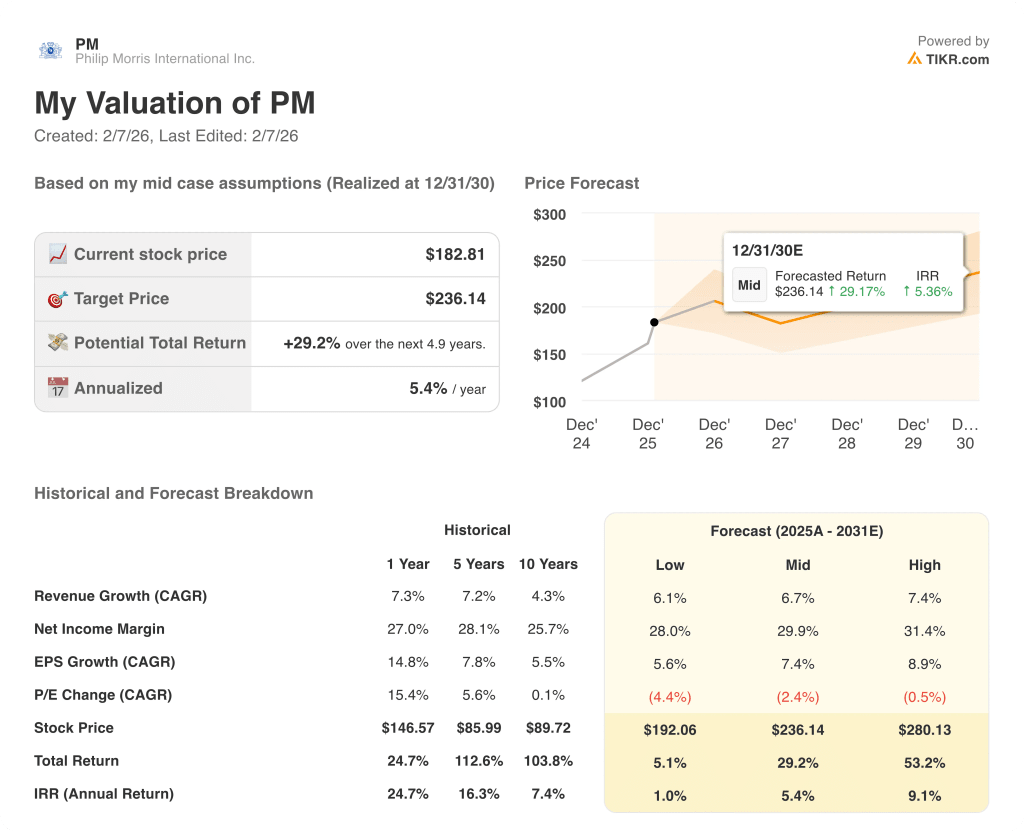

- Low Case: If competitive pressure persists and pricing offsets soften, revenue grows around 6.1% with net margins near 28.0% and valuation compresses → 1.0% annualized return.

- Mid Case: With smoke-free execution holding steady, revenue growth near 6.7% and margins improving toward 29.9% support stable valuation → 5.4% annualized return.

- High Case: If smoke-free momentum accelerates and pricing discipline strengthens, revenue reaches about 7.4% with margins approaching 31.4% as valuation stabilizes → 9.1% annualized return.

How Much Upside Does Philip Morris Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!