Key Takeaways:

- Backlog Inflection: Oracle’s $523 billion RPO base and $68 billion quarterly expansion signal AI infrastructure demand translating into contracted revenue, with OCI already growing 66% and cloud revenue reaching $8 billion in the quarter.

- Capital And Legal Overhang: Oracle’s $25 billion note deal and a class action tied to AI CapEx intensity frame investor focus on balance sheet and cash conversion, after management lifted FY26 CapEx expectations by $15 billion.

- Target Price Framework: Oracle stock could reach $296 by 2028 as a $67 billion FY26 base scales under a 31% revenue CAGR, 39% operating margins, and a 19x exit P/E that anchors normalization after the buildout phase.

- Return Math: Oracle’s $296 target implies 117% upside from the $136 current price, translating into a 40% annualized return over roughly 2 years based on earnings growth and a steady 19x multiple.

Oracle (ORCL) generates revenue from enterprise software and cloud subscriptions across ERP, HCM, database, and infrastructure, serving large institutions through SaaS and support.

Oracle’s FY25 gross profit of $40 billion and EBIT of $25 billion imply about $15 billion of operating costs, supporting a 44% operating margin that positions the model to fund higher cloud investment.

ORCL stock’s Q2 cloud revenue reached $8 billion on 33% growth, while OCI rose 66% and GPU revenue rose 177% which tightens the link between infrastructure scale and application attach in a $16 billion cloud apps run-rate.

Oracle ended Q2 with $523 billion of RPO after a $68 billion increase, but cash generation tightened as free cash flow was negative $10 billion on $12 billion of CapEx tied to data center equipment.

CFO of Oracle Doug Kehring also stated, “we expect and are committed to maintaining our investment-grade debt rating,” as the company raised $25 billion of notes and faced a class action tied to AI spending discipline.

With Oracle modeled at a 19x exit P/E versus 31% revenue growth assumptions into 2028, the debate centers on whether margin durability near 39% offsets the capital intensity implied by a $15 billion CapEx step-up.

What the Model Says for ORCL Stock

Oracle’s accelerating cloud scale and heavy AI capital intensity elevate expectations while sustaining strong competitive enterprise positioning.

However, the model assumes 30.5% revenue growth, 38.6% margins, and an 18.9x exit multiple, producing a $295.96 target price.

Therefore, the 116.9% total upside and 39.6% annualized return materially exceed typical equity opportunity costs over 2.3 years.

The model signals a Buy, as a 39.6% annualized return decisively compensates for Oracle’s capital intensity and execution risk.

With a modeled 39.6% annualized return far above a typical 10% equity hurdle, Oracle’s valuation emphasizes capital appreciation, sufficiently compensating for AI driven capital intensity, supporting a Buy under disciplined exit multiple and margin assumptions.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for Oracle stock:

1. Revenue Growth: 30.5%

Oracle stock’s revenue rose from $40 billion in 2021 to $57 billion in 2025, with LTM at $61 billion, while gross margin fell from 81% to 69% as cloud infrastructure expanded.

In Q2, cloud revenue reached $8 billion with OCI up 66%, and RPO reached $523 billion after a $68 billion increase, pointing to capacity-backed demand converting into recognized sales.

This path requires rapid data center delivery, sustained GPU-related demand, and continued multicloud adoption, while higher CapEx and slower conversion of backlog to revenue compresses the growth path quickly.

According to consensus analyst estimates 30.5% growth sets a high bar where any delay in capacity monetization hits revenue first and weakens returns fast, and this is above the 1 year historical revenue growth of 8%, indicating an aggressive step-up.

2. Operating Margins: 38.6%

Oracle posted about $40 billion of gross profit in 2025 on $57 billion of revenue, with EBIT at $25 billion, showing a high profit base even as gross margins compressed to 71%.

Q2 total revenue reached $16 billion and operating income reached $7 billion, while cloud revenue formed about half of revenue, keeping scale benefits visible even during a heavy infrastructure buildout.

This margin profile depends on disciplined pricing, fast utilization of new capacity, and stable spend in applications, while CapEx-led cash pressure and mix shift toward infrastructure weigh on operating leverage.

Based on street consensus estimates 38.6% margins rely on tight execution where cost creep or slower utilization erodes earnings first and compresses valuation quickly, and this is below the 1 year historical operating margin of 44%, indicating the model prices in reinvestment pressure.

3. Exit P/E Multiple: 18.9x

An 18.9x exit P/E capitalizes end-period earnings as a durability judgment rather than a price call.

Oracle’s model history shows a 1 year P/E of 30x and a 5 year P/E of 21x, placing today’s valuation context above the model’s terminal multiple even before factoring capital intensity.

The forecast uses an 18.9x exit multiple alongside 30.5% growth and 38.6% operating margins, meaning terminal value rests on earnings durability rather than a re-rating.

This multiple holds if Oracle sustains investment-grade discipline and converts AI backlog into repeatable profits, while legal overhang and balance sheet strain increase the chance of multiple compression.

In line with analyst consensus projections 18.9x leaves little room for disappointment because weaker margins reduce earnings and the market multiple compresses next, and this is below the 1 year historical P/E multiple of 30x, indicating conservative terminal valuation versus recent pricing.

What Happens If Things Go Better or Worse?

Oracle stock outcomes depend on cloud infrastructure utilization, AI backlog conversion, and cost discipline, setting up a range of possible paths through 2030.

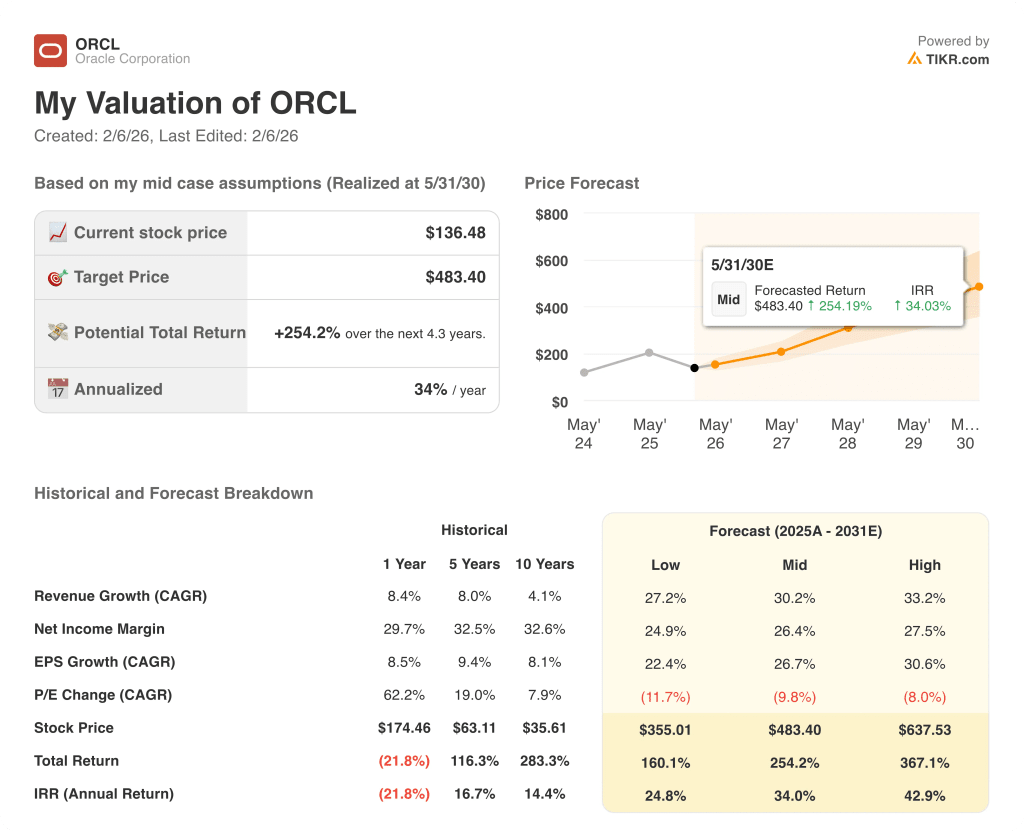

- Low Case: If AI capacity ramps unevenly and application growth slows, revenue grows around 27.2% and margins stay near 24.9% → 24.8% annualized return.

- Mid Case: With OCI expansion converting backlog steadily, revenue growth near 30.2% and margins improving toward 26.4% → 34.0% annualized return.

- High Case: If AI demand sustains rapid uptake and utilization tightens costs, revenue reaches about 33.2% and margins approach 27.5% → 42.9% annualized return.

How Much Upside Does Oracle Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!