Key Stats for Gartner Stock

- Past-Week Performance: -29%

- 52-Week Range: $139 to $536

- Valuation Model Target Price: $217

- Implied Upside: 43%

Value your favorite stocks like Gartner with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Gartner stock fell about 29% this week, ending near $152 per share, as investors reacted to a sharp post-earnings repricing and a wave of analyst price target cuts. The decline unfolded rapidly after the earnings release, with shares opening near $148 early in the week before stabilizing in the low-to-mid $150s as selling pressure eased.

The stock moved lower because management’s 2026 outlook came in more conservative than the market had been pricing in, despite a solid fourth-quarter earnings beat.

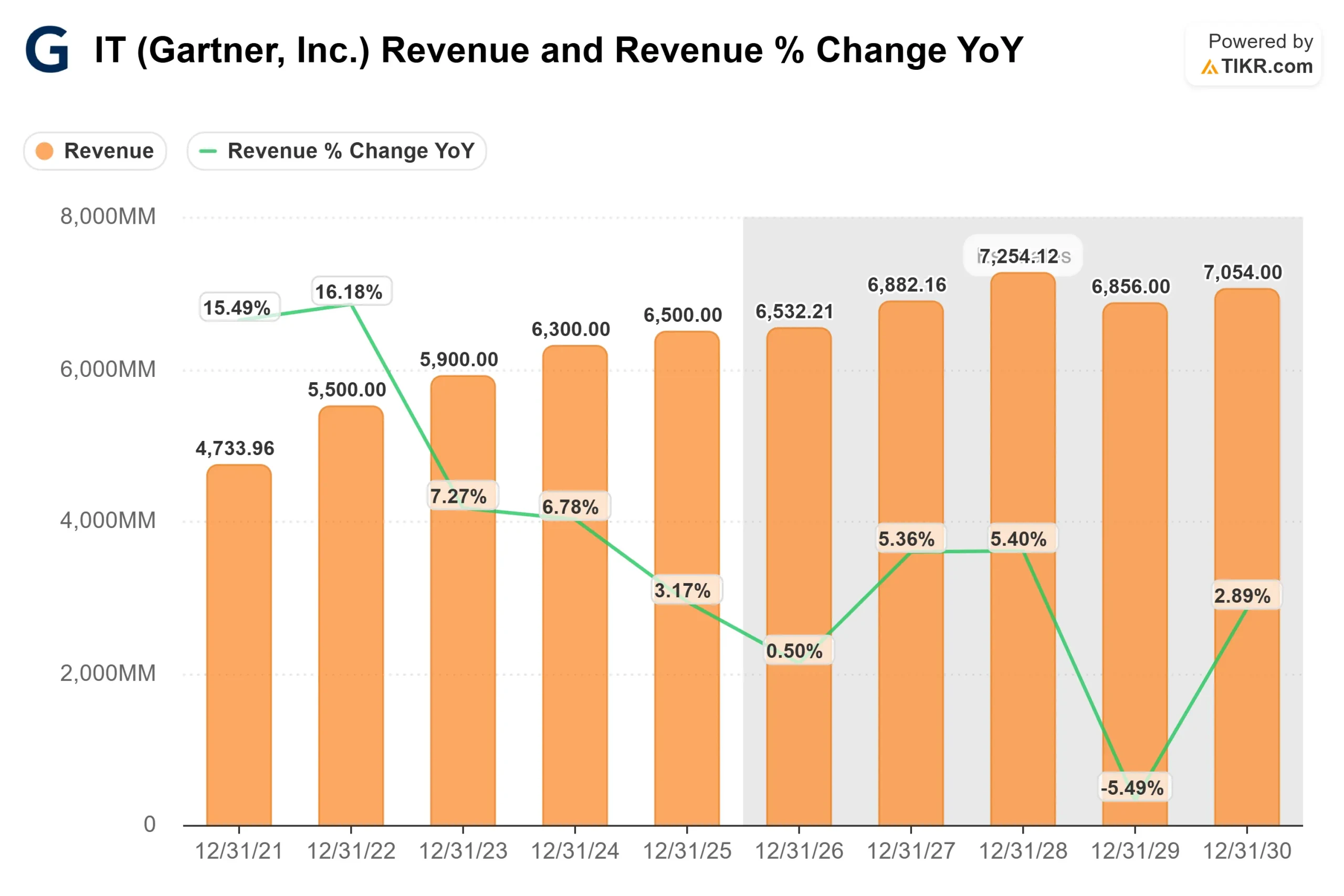

Gartner reported Q4 revenue of $1.8 billion, adjusted EPS of $3.94, and strong profitability, but guidance pointing to slower revenue growth and lower earnings in 2026 shifted investor focus toward continued caution in enterprise IT spending and longer decision cycles.

Last week’s earnings call reinforced that mixed picture. Management said fourth-quarter results exceeded expectations, with full-year EBITDA margins reaching 24.8% and free cash flow totaling $271 million in Q4, but guided to 2026 revenue of $6.455 billion or more, FX-neutral growth of about 2%, and adjusted EPS of $12.30 or more.

CEO Gene Hall emphasized confidence in the longer-term setup, stating that “we’re well positioned to accelerate CV growth throughout 2026,” even as clients remain cautious in the near term.

Analyst actions added pressure during the week. Morgan Stanley cut its price target to $200 from $275 and maintained an Equal Weight rating, while Wells Fargo lowered its target to $150 from $218 and assigned an Underweight rating.

Institutional activity was mixed, with Allianz Asset Management increasing its stake by 28.9% and Bessemer Group raising its position by 23.1%, while AustralianSuper reduced its holding by more than 90%, highlighting diverging views as the market reset expectations.

See analysts’ growth forecasts and price targets for Gartner (It’s free) >>>

Is Gartner Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 3.7%

- Operating Margins: 19.5%

- Exit P/E Multiple: 13x

Gartner’s growth profile reflects a business operating through a slower enterprise spending environment rather than a breakdown in its subscription-based model, with revenue anchored by recurring research contracts and high renewal rates.

Revenue growth has moderated, which places greater emphasis on margin durability, pricing discipline, and contract value expansion rather than aggressive top-line acceleration.

This setup means future returns depend more on earnings quality and recurring revenue than on a rapid rebound in enterprise IT budgets. Gartner’s ability to maintain strong contribution margins in its Insights segment allows incremental revenue to convert efficiently into earnings even in a low-growth environment.

Several business developments could support results over the next year. Demand for AI strategy, data governance, and efficiency-driven advisory work continues to deepen client engagement, supporting renewals and contract expansions even as discretionary spending remains tight.

Management’s multi-year transformation focused on improving insight impact, timeliness, and user experience is designed to lift engagement levels, which historically translate into stronger renewal rates and gradual contract value acceleration.

Capital allocation adds another layer of support. Gartner generated about $1.2 billion in free cash flow in 2025 and repurchased roughly $2 billion of stock, enhancing per-share earnings even in a slower growth environment.

Based on these inputs, the model estimates a target price of about $217, implying roughly 43% total upside over approximately 2.9 years, indicating the stock appears undervalued at current prices.

At current levels, Gartner appears undervalued, with expected returns driven by margin resilience, recurring revenue, and continued share repurchases rather than a rapid rebound in enterprise IT spending.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>