Key Takeaways:

- Exact Sciences Entry: Abbott stock reflects a $3 billion-plus Exact Sciences acquisition that adds a 15% growth cancer diagnostics platform to Abbott’s Diagnostics mix.

- Nutrition Reset: Abbott stock now discounts a 2026 Nutrition reset built on Q4 price actions and at least 8 new product launches over 12 months.

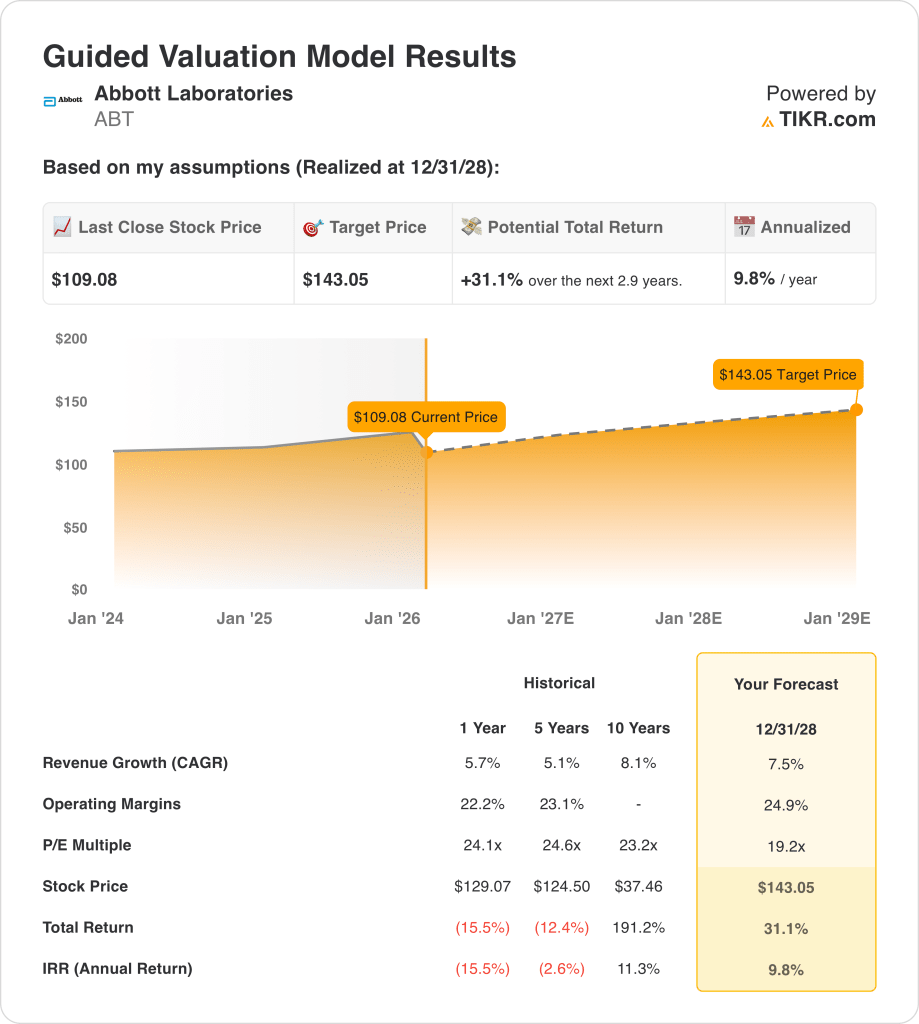

- Model Price Path: Abbott stock could reach $143 by 2028 on 8% revenue growth, 25% operating margins, and a 19x exit multiple.

- Return Math: From $109 today, Abbott stock implies 31% upside and a 10% annualized return through 2028.

Abbott (ABT) sells healthcare products across 4 segments, with revenue anchored in Diagnostics, Medical Devices, Nutrition, and Established Pharmaceuticals serving hospitals, clinics, and consumers at global scale.

ABT stock posted $44 billion of 2025 revenue and $25 billion of gross profit, offset by $17 billion of operating expenses that produced $8 billion of operating income and a 19% operating margin.

Abbott’s 2026 setup leans on Medical Devices growth and Diagnostics normalization, while Nutrition resets toward volume after inflation-era pricing pressured demand, with management planning at least 8 new Nutrition products over the next 12 months.

CEO Robert Ford of Abbot in earnings call last January 22 said, “We expect 2026 to be another year powered by innovation, operational excellence and strategic execution,” framing a 7% organic sales midpoint and 10% adjusted EPS growth intent.

ABT stock now trades near a 24x earnings reference while the model assumes a 19x exit multiple, creating tension between 8% growth expectations and $143 valuation support by 2028.

What the Model Says for ABT Stock

Abbott’s scale and defensive healthcare positioning support steady performance, though capital intensity constrains return expectations despite competitive strength.

However, the model assumes 8% revenue growth, 25% margins, and a 19x exit multiple driving a $143 target price.

Therefore, the modeled 31% total upside and 10% annualized return offer limited opportunity cost compensation versus equity risk.

The model signals a “Sell”, as the 10% annualized return falls below equity hurdle thresholds, indicating insufficient risk-adjusted compensation.

With a modeled 10% annualized return below a typical equity hurdle, the valuation emphasizes capital preservation over appreciation, indicating insufficient risk-adjusted compensation and justifying a Sell under disciplined capital-allocation logic.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for ABT stock:

1. Revenue Growth: 7.5%

Abbott’s revenue base spans Medical Devices, Diagnostics, Nutrition, and Established Pharmaceuticals, with 10-year revenue growth of 8.1% setting a demanding long-cycle reference.

Current execution shows Medical Devices up 10.5% and EPD up 7%, while Diagnostics declines 3.5% from planned COVID testing runoff.

Forward catalysts include Volt and TactiFlex Duo approvals, CMS coverage for TriClip and CardioMEMS, and an Exact Sciences close path with a February 20 shareholder vote.

According to consensus analyst estimates, 7.5% revenue growth breaks first if Nutrition stays negative past 2 quarters, leaving the valuation dependent on fewer segments, and this is above the 1-year historical 5.7%, so slippage quickly weakens outcomes.

2. Operating Margins: 24.9%

Abbott’s 1-year operating margin of 22.2% and 5-year level of 23.1% reflect a portfolio that historically supports steady efficiency gains.

Current profitability shows a 25.8% adjusted operating margin in Q4 and a stated annual improvement range of 50 to 70 basis points.

Margin support comes from Medical Devices scale, Core Lab momentum outside China, and disciplined spend levels even as Nutrition resets price and promotion.

Based on street consensus estimates, 24.9% margins fail first if Nutrition price actions cut mix and tariffs persist, forcing reinvestment that compresses earnings, and this is above the 1-year historical 23.2%, so execution discipline must hold.

3. Exit P/E Multiple: 19.2x

Abbott’s 1-year P/E multiple of 24.1x contrasts with a more conservative terminal multiple that assumes less re-rating by 2028.

The 19.2x exit multiple capitalizes earnings durability after the model already embeds 7.5% growth and 24.9% margins.

That multiple treats end-period outcomes as market-normalized for a mature large-cap, limiting valuation reliance on sentiment rather than fundamentals.

In line with analyst consensus projections, 19.2x is unforgiving if growth or margins miss, since disappointment typically compresses multiples further, and this is below the 1-year historical 24.1x, indicating the model assumes valuation compression.

What Happens If Things Go Better or Worse?

Abbott stock outcomes depend on medical device adoption, diagnostics normalization, and portfolio execution discipline, setting up a range of possible paths through 2030.

- Low Case: If device momentum slows and diagnostics remain uneven, revenue grows around 7% and margins stay near 20% → 6% annualized return.

- Mid Case: With devices and nutrition stabilizing as expected, revenue growth near 7% and margins improving toward 22% → 10% annualized return.

- High Case: If device launches exceed expectations and efficiency improves, revenue reaches about 8% and margins approach 23% → 15% annualized return.

How Much Upside Does It Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!