Key Stats for Danaher Stock

- 52-Week Range: $172 to $243

- Current Price: $175

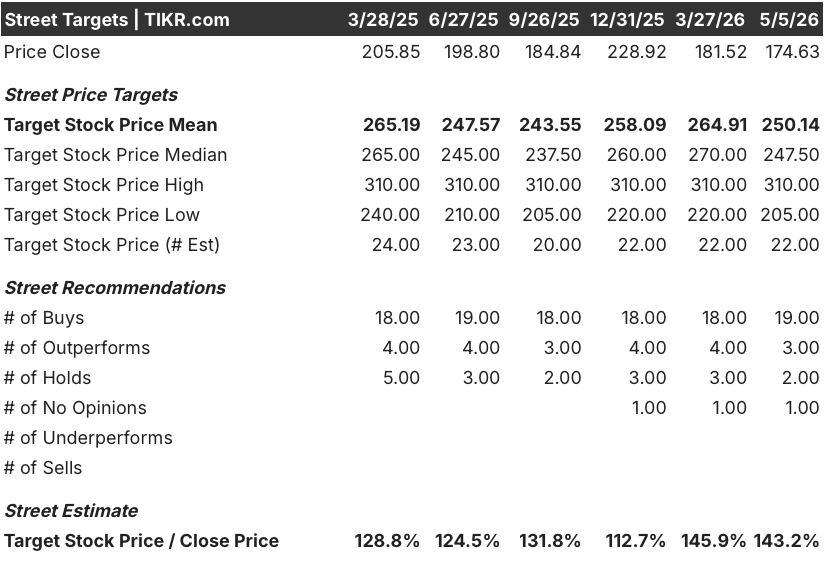

- Street Mean Target: $250

- Street High Target: $310

- Analyst Consensus: 19 Buys / 3 Outperforms / 2 Holds / 0 Underperforms / 0 Sells

- TIKR Model Target (Dec. 2030): $249

What Happened?

Danaher Corporation (DHR) is a Washington, D.C.-based life sciences and diagnostics company that designs and manufactures the instruments, consumables, and software used by pharmaceutical companies to develop, test, and manufacture drugs at scale.

Danaher stock moved higher in pre-market trading on April 21 after the company reported Q1 2026 adjusted EPS of $2.06, beating the consensus estimate of $1.94 by 6.2%.

The beat was not broad-based: revenue came in at $5.95 billion, a touch below the $6 billion consensus, with a 2.5 percentage point headwind from a lighter-than-typical respiratory season at Cepheid, its molecular diagnostics unit.

Strip out respiratory, and the underlying business grew core revenue approximately 3% year-over-year, with bioprocessing (the segment that supplies equipment and consumables for commercial biologics manufacturing) delivering high single-digit core growth.

The standout figure was equipment orders in bioprocessing, which grew more than 30% year-over-year in Q1, marking the first quarter of positive year-over-year equipment order growth in nearly two years.

CEO Rainer Blair framed the orders inflection directly on the Q1 2026 earnings call: “We’ve seen three quarters of sequential order growth. In the fourth quarter, we saw actual sales growth in equipment. And we’re encouraged by that, and we want to see that trend continue.”

The company also raised the upper end of its full-year adjusted EPS guidance to $8.35 to $8.55, from $8.35 to $8.50 previously, citing Q1 momentum and cost discipline that is flowing through at a rate of 35% to 40% incremental margin on every dollar of incremental revenue.

Layered on top of the quarter is the pending $9.9 billion acquisition of Masimo Corporation, a provider of pulse oximetry and patient monitoring devices used in acute care settings, announced in February and approved by Masimo shareholders on May 4.

Wall Street’s Take on DHR Stock

The Q1 beat on earnings matters less than what the equipment order book is signaling: after 24 months of underinvestment in biologic manufacturing capacity, the cycle is turning, and Danaher stock is the most direct institutional bet on that inflection.

DHR’s EBITDA reached $1.988 billion in Q1 2026, up 5.7% year-over-year, with EBITDA margins expanding to 33.4% from 32.75% a year earlier, driven by cost discipline outpacing the respiratory revenue drag and setting up stronger fall-through as growth accelerates in the second half.

Twenty-two analysts currently cover DHR, with 19 rated Buy or Outperform and a mean price target of around $250, implying roughly 43% upside from current levels; the median target of $248 and a Street high of $310 reflect strong conviction even after the Masimo deal introduced new leverage and strategic uncertainty.

The $250 mean target is anchored to a second-half growth ramp: management guided core revenue up low single digits in Q2 and expects to exit Q4 in the mid-single-digit range as the three headwinds (China diagnostics policy, weak respiratory, Life Sciences comps) collectively fade by roughly 300 basis points from the first half into the second.

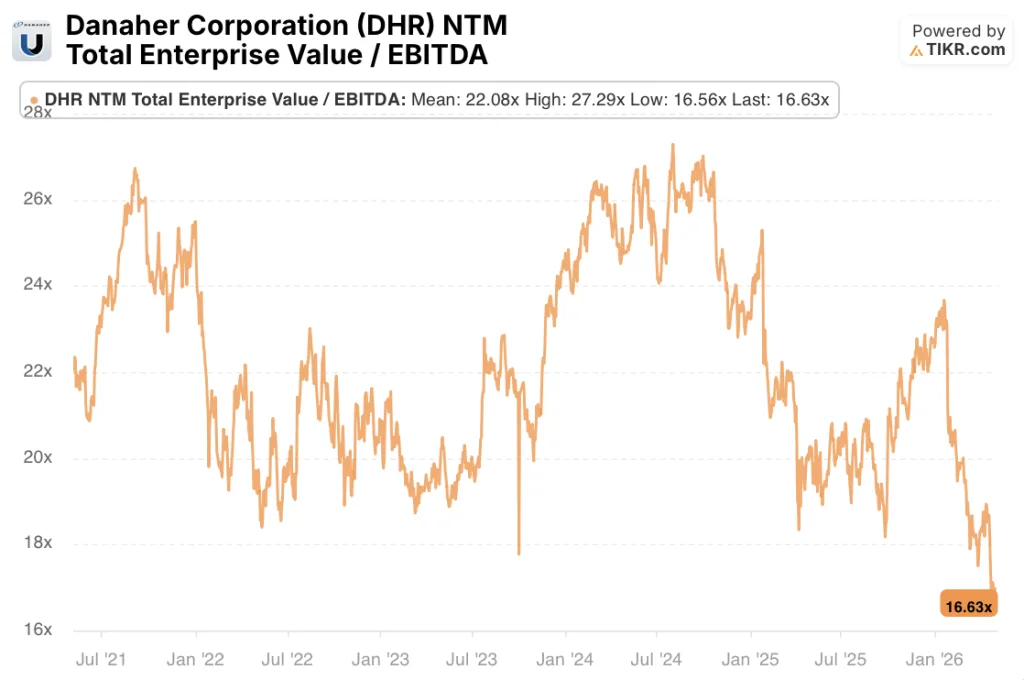

At 16.63x forward EV/EBITDA on a business where the EBITDA growth rate is accelerating from 6% to a projected 13% exit rate by Q4 2026, while the equipment cycle is in its first quarter of confirmed positive order growth after two years of contraction, Danaher stock is undervalued relative to the earnings power that the second-half ramp is positioned to unlock.

The one development that genuinely reframes perception here is the bioprocessing equipment order figure: 30%-plus year-over-year growth is not a bounce off a low base; it is the signal that pharmaceutical manufacturers have begun committing capital to capacity expansion rather than simply running existing lines harder.

If consumables growth stalls below high single digits, it would indicate that commercial biologic drug production volumes are weaker than the prescription data implies, which would undermine both the near-term revenue ramp and the long-term Masimo integration thesis.

The Q2 adjusted operating margin guide of approximately 27% is the number to watch: if Danaher delivers at or above that level while accelerating equipment order fulfillment, it confirms the fall-through model is intact heading into the second-half growth ramp.

Financials

Danaher’s Q1 2026 revenue of $5.95 billion grew 3.7% year-over-year, continuing the gradual recovery from the post-pandemic deceleration that pushed revenue growth negative in two of the prior eight quarters.

The gross margin line tells a cleaner story: DHR’s gross profit margin held at 60.3% in Q1 2026, matching the high end of the range over the past eight quarters and demonstrating that cost-of-goods discipline has not eroded even as the mix shifted toward a weaker respiratory season that typically carries above-average margins.

Operating income reached $1.37 billion in Q1 2026, up 5.7% year-over-year, with operating margins expanding to 22.9% from 22.5% a year ago, driven by SG&A declining to $1.84 billion from $1.86 billion in the comparable quarter while revenue grew.

The operating leverage story becomes more pronounced when examined in sequence: from Q3 2025 through Q1 2026, operating income grew from $1.15 billion to $1.52 billion to $1.37 billion, with the Q1 figure representing the highest year-over-year operating income growth rate in six quarters at 5.7%, despite the respiratory headwind.

What Does the Valuation Model Say?

TIKR’s mid-case model projects a target price of around $249, implying a 42% total return over the next 4.6 years at an annualized rate of around 8%, anchored to revenue growing at roughly a 4% CAGR through 2030 and net income margins expanding from 23.1% today toward around 25%.

The investment case for Danaher stock hinges on a single question: whether the bioprocessing equipment order inflection translates into recognized revenue at the pace and magnitude that underwrites the second-half growth ramp and eventual return to mid-single-digit core growth.

Bull Case: The Capacity Cycle Accelerates

- Bioprocessing equipment orders grew more than 30% year-over-year in Q1 2026, the first positive year-over-year print in nearly two years, signaling committed capital rather than inquiry activity

- Management guided equipment growth to flat in 2026 as a conservative baseline; any positive equipment revenue would lift core growth above the 3% to 6% range

- China bioprocessing delivered double-digit growth in Q1, recovering from prior contraction, as Chinese biotech companies monetize drug pipelines through licensing deals and Hong Kong IPOs

- The Masimo acquisition, closing in the second half of 2026, adds roughly 15 to 20 cents of adjusted EPS accretion in the first full year, with a projected $125 million in cost synergies by year 5

- Cepheid’s nonrespiratory business grew mid-teens in Q1, led by sexual health and hospital-acquired infection assays, with the newly cleared Xpert GI panel adding a new growth vector independent of seasonal respiratory demand

Bear Case: Execution Risk Accumulates

- The $9.9 billion Masimo acquisition adds roughly 2.5x net debt to EBITDA at close, constraining balance sheet flexibility and introducing integration risk outside Danaher’s core life sciences competency

- Revenue missed the Q1 consensus by about 0.7%, driven in part by factors (respiratory, China VBP) that the company controls less directly than equipment orders suggest

- The TIKR low-case model implies only a 3.5% annualized return through 2030 if revenue growth comes in at the bottom of the range and margins compress rather than expand

- Academic and government funding in the U.S. remains a headwind, and any further federal research spending cuts could extend the Life Sciences recovery timeline beyond management’s current expectations

- The Masimo deal includes $634 million in unresolved Apple litigation exposure and a contested patent portfolio, creating headline risk that could weigh on DHR sentiment regardless of operational progress

Should You Invest in Danaher Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Danaher Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Danaher Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DHR stock on TIKR for Free →