Key Stats for GE Stock

- Past week’s performance: Consolidating

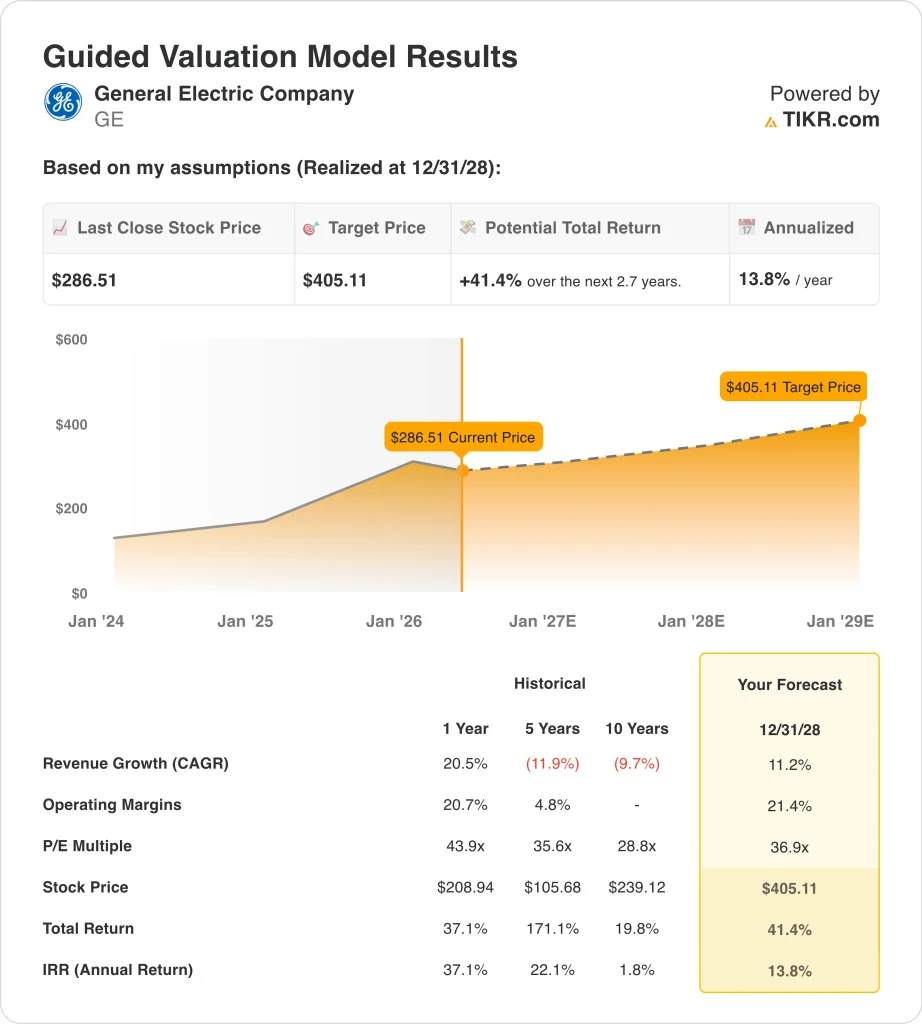

- 52-week range: $206 to $348

- Valuation model target price: $405

- Implied upside: 41.4% over 2.7 years

Value your favorite stocks like GE with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

General Electric Company, now operating as GE Aerospace (GE), designs and manufactures jet engines, propulsion systems, and aviation technology for commercial airlines and military customers worldwide. The company delivered a strong Q1 2026 earnings beat, reporting adjusted EPS of $1.86 per share against the analyst consensus of $1.60.

Management also confirmed it is holding full-year guidance and trending toward the high end of its forecast range. That double-positive update initially sent the stock higher, but investors then pivoted toward concerns about Iran war-driven fuel cost surges slowing airline growth.

The fuel cost concern matters directly for GE Aerospace because airlines are the primary buyers of its engines. Higher fuel costs slow airline capacity expansion, which in turn reduces demand for new engine orders. United Airlines and other major carriers have already signaled caution on growth plans through the rest of 2026.

GE Aerospace’s CFM International joint venture with Safran is the dominant supplier of engines for single-aisle aircraft. But demand for new engines depends on how aggressively airlines order new planes. A slowdown in airline expansion could soften the order outlook even as current service demand remains robust.

On the positive side, GE Aerospace’s engine services business generates recurring revenue regardless of new aircraft order rates. Airlines must service their fleets whether they are expanding or cutting capacity.

France’s Safran reported stronger-than-expected Q1 jet engine revenue, suggesting MRO (maintenance, repair, and overhaul) demand remains healthy. Copa Airlines also just placed a large Boeing 737 Max order, which means more CFM LEAP engines will require delivery and long-term servicing contracts.

If GE follows through on its guidance trajectory, the full-year earnings should meaningfully exceed current consensus estimates and support a higher stock price.

See analysts’ growth forecasts and price targets for GE (It’s free) >>>

Is General Electric Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 11.2%

- Operating Margins: 21.4%

- Exit P/E Multiple: 36.9x

Based on these inputs, the model estimates a target price of $405, implying 41.4% total upside from the current share price and a 13.8% annualized return over the next 2.7 years.

The Street consensus target is $350, which sits above the current price of $287 but below the model’s $405 target. The difference lies mainly in the exit P/E assumption.

GE Aerospace currently trades at roughly 35.6 times trailing earnings, so the model’s 36.9 times exit multiple is close to where the stock trades today. That means most of the 41.4% upside must come from earnings growth rather than multiple expansion.

Revenue growth of 11.2% per year is supported by a strong engine order backlog and growing aftermarket services. GE Aerospace has signed large long-term engine service contracts with flydubai, Avolon, and Riyadh Air.

Those contracts provide revenue visibility well beyond 2028 and reduce the risk that near-term airline weakness hurts the top line significantly. The aftermarket business compounds as more engines age into their service cycles, and GE Aerospace has the world’s largest installed commercial engine base.

Operating margins of 21.4% represent a modest step up from the current LTM EBIT margin of 20.3%. That improvement is consistent with GE Aerospace’s operational efficiency programs and the ongoing shift toward higher-margin aftermarket revenue.

At roughly 37 times forward earnings, the stock is not cheap in absolute terms. But the quality and visibility of GE Aerospace’s earnings, backed by long-term service contracts, typically justifies a premium multiple relative to industrial peers.

What’s Driving GE Stock Going Forward?

The engine services backlog is the most visible and durable growth driver. GE Aerospace’s CFM International holds one of the largest commercial engine backlogs in aviation history. Recent deals include Pegasus Airlines signing for up to 300 LEAP-1B engines and Riyadh Air ordering 120 CFM LEAP-1A engines for Airbus A321neos.

Those orders generate decades of service revenue and reduce dependence on any single airline or region. Even if new aircraft deliveries slow in the near term, the existing installed base provides a steady and growing service revenue floor.

GE Aerospace’s partnership with Singapore for next-generation aviation technologies, announced in February 2026, opens international collaboration in Asia’s fastest-growing aviation market. Singapore is a major MRO hub, and that relationship could help GE Aerospace expand its services footprint in the region over the coming years.

The annual general meeting on May 5 is also an opportunity for management to reaffirm full-year guidance and address investor concerns about the fuel cost environment. Any clarity on the earnings trajectory should reduce near-term uncertainty.

Defense is a growing and underappreciated contributor to GE Aerospace’s revenue. While commercial aviation gets most of the attention, GE Aerospace also supplies propulsion systems for military aircraft.

Rising global defense budgets benefit engine development programs and government service contracts. The company’s investment in next-generation engine technology positions it well for future military procurement as governments upgrade aging fleets.

One key risk remains the Iran-related fuel shock and its ripple effect on airline expansion plans. Airlines that defer new aircraft orders slow the new engine delivery cycle. But GE Aerospace’s aftermarket revenue provides a meaningful cushion against that risk.

Management reaffirmed guidance even while acknowledging the fuel uncertainty, which is itself a positive signal. Investors comfortable with near-term noise may find the 41.4% model upside target at $287 per share a compelling entry point for a long-term hold.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in General Electric?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up GE, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track GE alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze General Electric stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!