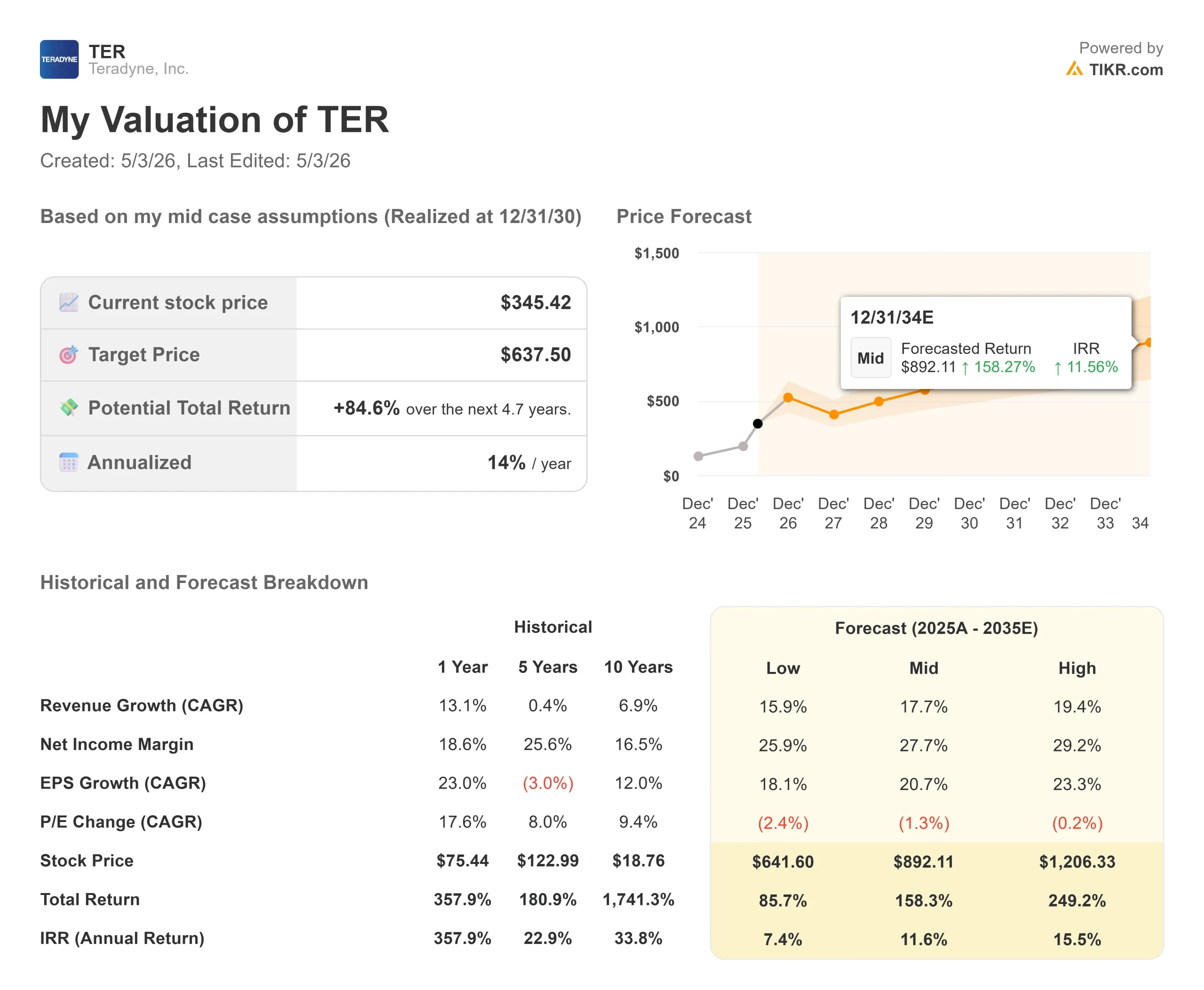

Key Stats for Teradyne Stock

- Current Price: $345.42

- Target Price (Mid): ~$638

- Street Target: ~$366

- Potential Total Return: ~85%

- Annualized IRR: ~14% / year

- Earnings Reaction: -19.41% (April 29, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Teradyne (TER) just posted the best quarter in its history, and the market answered with a 19.41% single-day drop. The stock has since recovered to $345.42, sitting about 18% below its 52-week high of $422.11. Bulls say the sell-off was an overreaction to guidance noise. Bears say the premium valuation and limited second-half visibility justified the reset. What the earnings call actually reveals leans heavily toward the bulls.

The Quarter That Broke Every Company Record

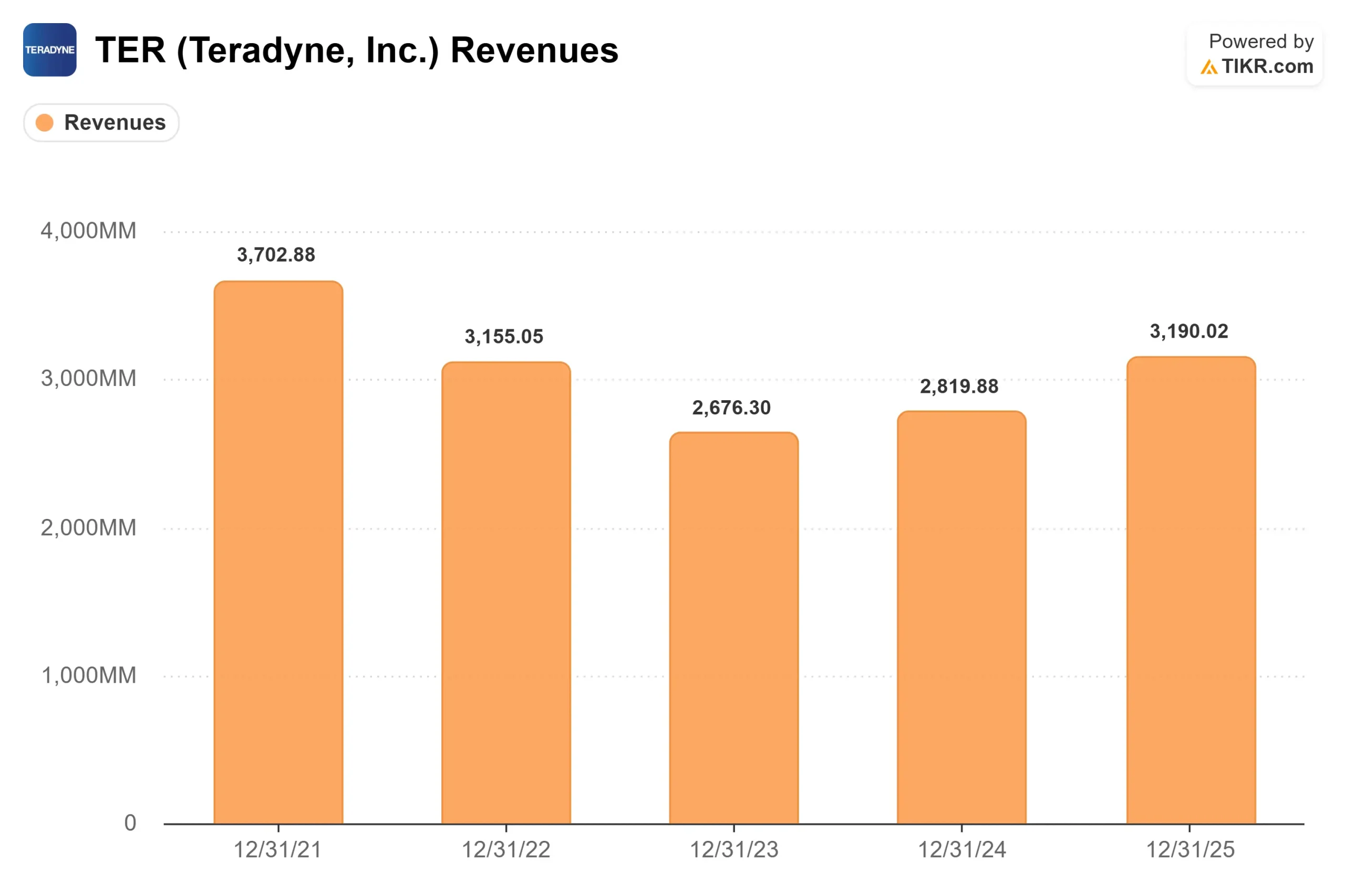

Q1 2026 results beat on every line. Revenue of $1.282 billion came in 5.45% above the $1.216 billion analyst estimate and 87% above Q1 2025. Non-GAAP EPS of $2.56 beat the $2.12 consensus by 20.93%. The previous quarterly revenue record, set during the mobile peak of Q2 2021, fell by $200 million.

“Our previous high watermark was in the consumer-driven mobile peak of Q2 of 2021,” CEO Greg Smith said. “In Q1 of 2026, our revenue was $200 million or 18% higher than that previous record.”

The sell-off had nothing to do with Q1. It was about Q2 guidance: non-GAAP EPS of $1.86 to $2.15 and gross margin of 58% to 59%, both below Q1’s record 60.9%. CFO Michelle Turner explained on the call that about half of Q1’s margin outperformance came from nonrecurring operational benefits. Normalized for those, Q1’s underlying margin was closer to 59.5%, making the Q2 guide a normalization, not a deterioration. First-half gross margins are expected to average around 59.7%, within the company’s stated target model range of 59% to 61%.

See historical and forward estimates for Teradyne stock (It’s free!) >>>

What the Call Says About the Second Half

AI-related revenue reached nearly 70% of total Q1 sales, up from about 60% in Q4 2025. Within Semiconductor Test, which produced $1.111 billion of the $1.282 billion total, compute represented roughly 75% of SoC (system-on-chip) revenue at $882 million. Memory added $203 million, and IST contributed $27 million.

Smith described demand through three stacking AI waves: first, general-purpose data center buildout (the 2025 surge); second, inference-optimized silicon (now underway); third, edge AI and physical AI (yet to arrive). “These waves are broad-based,” he said, “and we expect them to stack on top of each other, driving significant ATE TAM growth over the full midterm.” ATE stands for automated test equipment, the systems Teradyne builds to verify that chips work correctly before they ship.

The front-half weighting reflects VIP compute (very-integrated platform compute, meaning chips designed by hyperscalers for their own data centers) demand concentrated in H1, with the next generation of those products targeted for early 2027. But two product lines run counter to the front-half story. Memory test is expected to be more back-half weighted as HBM (high-bandwidth memory) and DRAM demand continue to build. IST is also tracking toward a stronger second half, driven by HDD storage demand growing at more than 20% annually, fueled by AI data requirements. The second half is a product mix shift, not a slowdown.

The GPU Win and Silicon Photonics

Two developments from the call deserve more attention than the sell-off narrative allowed.

Teradyne received its first multisystem production test orders for merchant GPU in Q1, with those systems scheduled to ship and enter production in Q2. This is new territory: Advantest (TYO: 6857) has been the established player in merchant GPU testing, and Teradyne is now a qualified alternative. Smith described a “fast follower” strategy: qualify the platform once, then rapidly convert additional device SKUs.

He was clear about the timeline, noting it will take “a few years” to reach 30% to 70% GPU market share, but the company only needs low double-digit GPU share to hit its $6 billion long-term revenue target. Full-year 2026 GPU revenue is guided at around $50 million.

Teradyne also launched Photon 100 in Q1, a platform for silicon photonics testing. Silicon photonics uses light instead of electrical signals to transmit data, enabling faster connections inside AI data centers. Management estimates this market could reach $300 million to $700 million annually over the midterm, with around $100 million in 2026 revenue already in view.

On the acquisition front, Teradyne closed two deals in April. The MultiLane Test Products joint venture (closed April 8) targets high-speed data center interconnect testing. TestInsight (closed April 16) is the leading provider of test development tools used across both Teradyne and competing platforms. Combined, the two deals used approximately $165 million of cash funded through the company’s credit revolver. TestInsight directly supports the GPU fast follower strategy by enabling a virtual test environment that reduces time to market for new devices.

See how Teradyne performs against its peers in TIKR (It’s free!) >>>

Is the Valuation Justified?

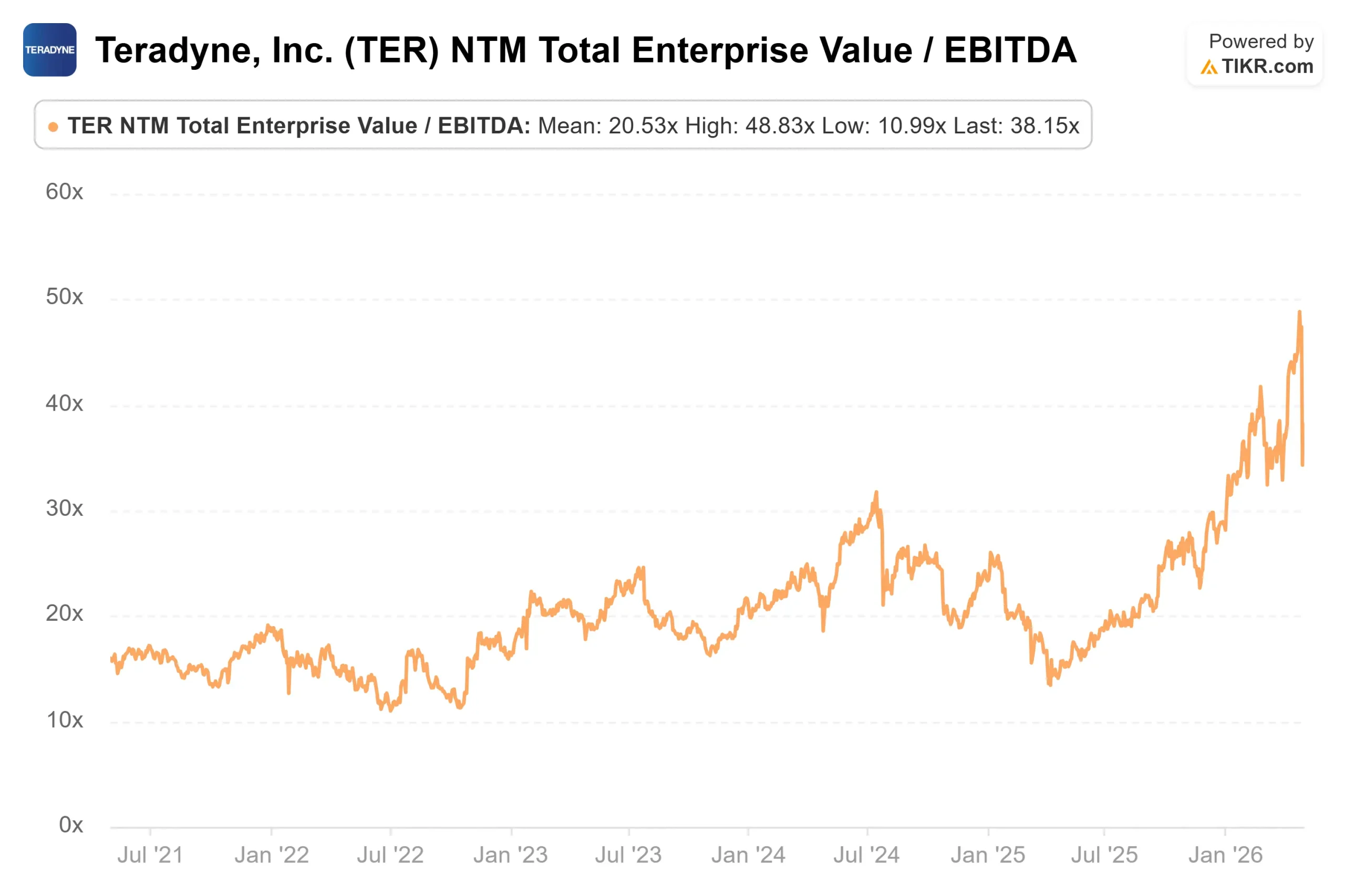

At $345.42, Teradyne trades at an NTM P/E of 52.02x. The semiconductor equipment peer group median sits at around 38x NTM P/E per TIKR’s Competitors data, with ASML (NASDAQ: ASML) at approximately 36x and Lam Research (NASDAQ: LRCX) at approximately 34x. Teradyne’s premium is real, but so is its growth rate.

The Street mean target of ~$366 implies about 6% upside from current levels. Of 17 analysts tracked by TIKR as of May 1, 2026, the breakdown is 11 Buys, 1 Outperform, 6 Holds, 2 No Opinions, 1 Underperform, and 1 Sell. The high target of $470 and low of $270 reflect the same binary: does second-half demand hold, and does GPU revenue scale as guided?

The free cash flow picture supports the longer-term case. LTM levered free cash flow stands at $292 million, but consensus estimates on the TIKR project FCF expanding to over $1.1 billion in 2026 as operating leverage on AI-driven revenue takes hold. The NTM MC/FCF of 53.34x compresses quickly at that rate of earnings growth.

The main risk is customer concentration. Three customers (two specifying and one purchasing) exceeded 10% of Q1 revenue. A program delay from any of them can, as Smith noted, “lead to short-term demand peaks and valleys superimposed over a long-term strong growth trend. In other words, it’s lumpy growth.” The valuation multiples look different against Teradyne’s own long-term model: $6 billion in revenue and $9.50 to $11.00 in non-GAAP EPS. Against today’s $345.42 price, the midpoint of $10.25 in target EPS implies a forward P/E below 34x on the company’s multi-year targets, materially different from today’s 52x.

TIKR Advanced Model Analysis

- Current Price: $345.42

- Target Price (Mid): ~$638

- Potential Total Return: ~85%

- Annualized IRR: ~14% / year

See analysts’ growth forecasts and price targets for Teradyne stock (It’s free!) >>>

The TIKR mid-case model uses a revenue CAGR of approximately 18% through 12/31/30 with a net income margin of around 28%. The two drivers are AI compute test demand growing as VIP compute programs cycle through generations and merchant GPU share builds, and memory test expansion as HBM and DRAM test intensity rises with each new AI accelerator generation. The margin driver is operating leverage: Q1’s record 37.5% non-GAAP operating margin illustrates how sharply incremental AI compute revenue drops to the bottom line at scale.

The upside scenario assumes faster GPU share gains and silicon photonics reaching the high end of the $300 million to $700 million TAM estimate. The downside scenario reflects lighter second-half demand and a delayed path to the $6 billion revenue model. The primary risk in both cases is ordering lumpiness from a concentrated customer base: as CFO Turner noted, timing shifts “can impact revenue within the quarter or across year boundaries.”

Conclusion

The metric to watch at Teradyne’s Q2 2026 earnings call, expected July 29, 2026, is merchant GPU revenue. Management has guided around $50 million for the full year, with production beginning in Q2. If Q2 discloses a GPU revenue figure tracking ahead of that guide, or if Smith confirms additional SKUs converting to Teradyne’s platform faster than planned, the fast follower strategy is ahead of schedule. Teradyne delivered record results across every metric in Q1, closed two acquisitions, launched a silicon photonics platform, and secured its first merchant GPU production win, all in one quarter. Whether the 19% drop was fair or excessive, the Q2 call will begin to answer that.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Teradyne?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Teradyne, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Teradyne alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Teradyne on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!