Key Stats for Seagate Stock

- Current Price: $726.93

- Target Price (Mid): ~$1,520

- Street Mean Target: ~$755

- Potential Total Return: ~109%

- Annualized IRR: ~19% / year

- Earnings Reaction: +11.10% (April 28, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Seagate Technology (STX) jumped 11.10% on April 28 after fiscal Q3 2026 results beat Wall Street on every major line. Revenue of $3.1 billion came in 5.02% above consensus. Non-GAAP EPS of $4.10 beat estimates by 16.56%. The stock closed within cents of its 52-week high of $728.00, and has now risen nearly 700% from its 52-week low of $91.92.

Bulls are pointing to record margins and near-decade-high free cash flow generation, with demand locked in through fiscal 2027. Bears are questioning how much is already priced into a stock at 30.86x next twelve months earnings. Both sides have a point. Neither fully captures what management disclosed about the years ahead.

What the Raised Growth Target Actually Signals

The headline numbers were strong. Non-GAAP gross margin reached 47%, up 480 basis points sequentially. Non-GAAP operating margin hit 37.5%, up 560 basis points in a single quarter, per CFO Gianluca Romano on the Q3 FY2026 earnings call. Free cash flow reached $953 million for the quarter, one of the highest levels in over a decade, also per Romano.

The detail that matters most for long-term investors: CEO Dave Mosley raised Seagate’s annual revenue growth target from the low-to-mid-teens to a minimum of 20% over the next several years. That is not quarterly guidance. It is a reset of how management views the business trajectory.

Three things support that confidence.

First, the top three global cloud service providers have nearly doubled their remaining performance obligations to approximately $1.1 trillion, per Mosley on the call, signaling sustained infrastructure spending ahead.

Second, nearline capacity, which refers to high-capacity drives sold into cloud data centers, is almost fully allocated through calendar 2027.

Third, build-to-order contracts defining specific configurations and pricing are finalized through fiscal 2027, with customer planning discussions already underway for calendar 2028.

On pricing, Romano was direct: “We are continuing to execute this strategy that allowed us to increase profitability for the last 12 consecutive quarters. We are confident in saying that we have a good opportunity to increase our profit and our revenue sequentially through fiscal ’27.”

See historical and forward estimates for Seagate stock (It’s free!) >>>

The Demand Drivers Analysts Are Still Catching Up To

The Q3 call added specificity to the demand story beyond the hyperscaler buildout already locked in through 2027. Mosley described agentic AI, which refers to systems that autonomously execute tasks rather than responding to individual queries, as creating a new type of data intensity.

“When you do that, you may actually reference enormous data sets to draw your conclusion, and you may actually create new data that needs to be propagated out in the world. To the extent that that’s unstructured data, video data, that’s where it’s actually hitting the storage tiers fairly hard.”

Romano added, “You need historical data for agents to reason, and you need to store that data for compliance. We see those as huge benefits to our business.”

Physical AI is the longer-range piece. Mosley cited a single autonomous vehicle as producing up to 4 terabytes of data per hour, with retention requirements of five to ten years for compliance and model retraining, a storage workload that barely exists in current demand forecasts.

Wall Street repriced quickly after the print. Rosenblatt doubled its target from $500 to $1,000, maintaining a Buy rating and citing fully allocated nearline supply through 2027. BofA raised to $840, Goldman Sachs to $700, TD Cowen to $850, and Barclays to $750, each citing tight supply and AI-driven demand. UBS raised its target to $545 but kept a Neutral rating, arguing the market may already be pricing in structural improvements.

Per TIKR, the Street currently shows 16 Buy ratings, 4 Outperform, 4 Hold, 1 Underperform, and 1 Sell across 27 analysts, with a mean price target of $755.29 based on 22 submitted price targets.

The Mozaic Platform and What It Does to Margins

Mozaic 4, the second-generation HAMR (Heat-Assisted Magnetic Recording, a laser-based technology enabling denser data writing) product, delivers up to 44 terabytes per drive, more than 30% more capacity than its predecessor, using the same number of disks and heads with minimal change to the bill of materials, per Mosley on the call. Revenue shipments began in late March. Management expects Mozaic 4 to represent a majority of HAMR exabyte shipments by the end of calendar 2026.

Romano explained the cost logic plainly: “Now that we have second-generation HAMR, we have a very good increase in terabytes per unit. This is the main driver for the future cost reduction.” More revenue-generating capacity from roughly the same manufacturing cost base means each product generation widens profit margins as the mix shifts upward.

Mozaic 5 targets 50-terabyte drives with qualification shipments in late calendar 2027, using the same 10-disk platform and power footprint. For hyperscalers designing data centers years in advance, a predictable upgrade path with no changes to power or floor space requirements is a genuine competitive advantage.

Fitch upgraded Seagate’s credit to investment grade during the quarter, citing balance sheet strengthening and profitability expansion, per Romano on the call. Per TIKR, LTM Net Debt/EBITDA now stands at 0.76x.

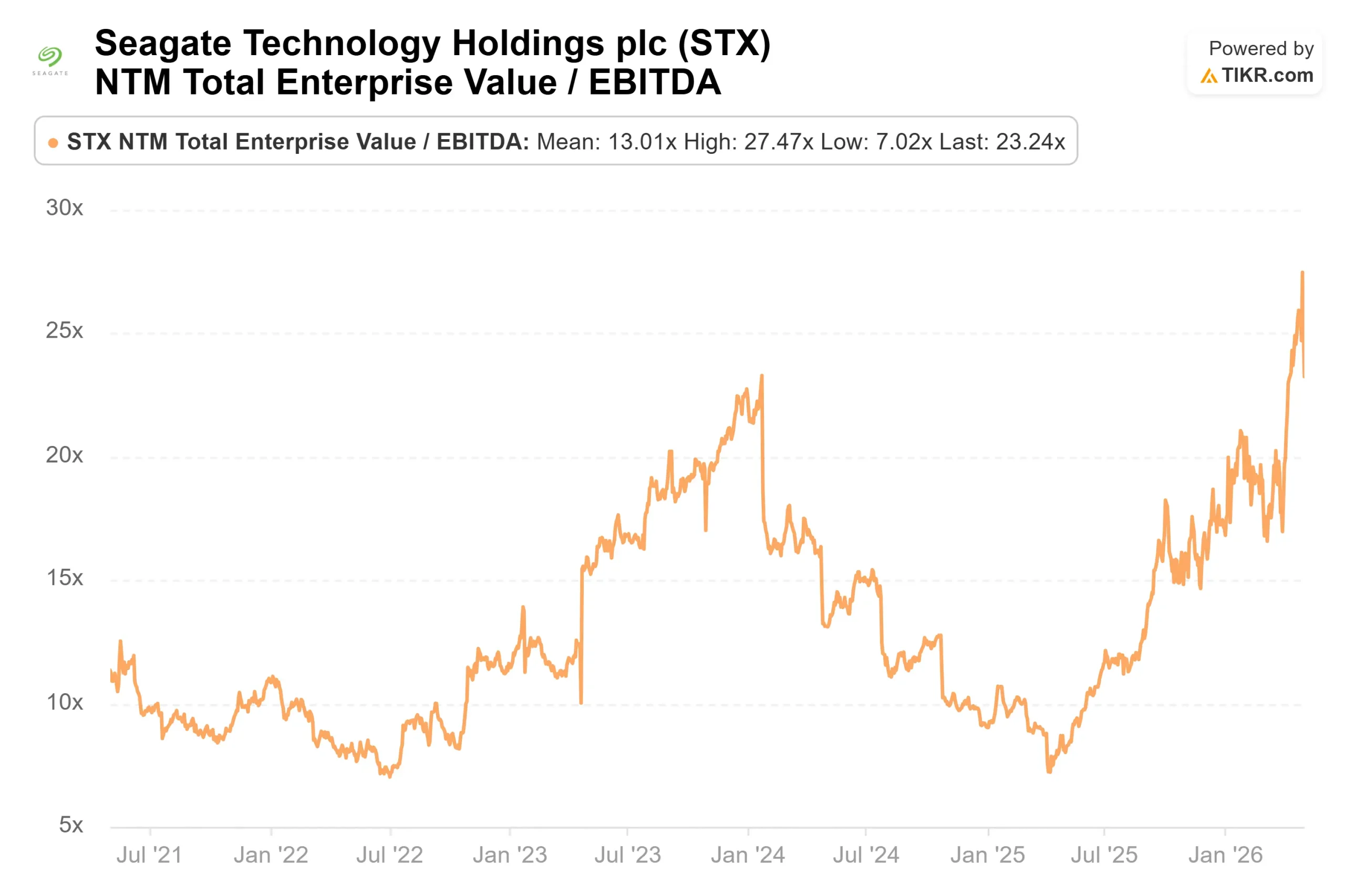

Seagate’s premium valuation is stark against peers. Per TIKR’s Competitors page, Dell Technologies (DELL) trades at 10.64x NTM EV/EBITDA and 16.24x NTM P/E. NetApp (NTAP) trades at 9.55x NTM EV/EBITDA and 13.32x NTM P/E. Seagate sits at 23.24x NTM EV/EBITDA and 30.86x NTM P/E.

Neither Dell nor NetApp is posting 44% year-over-year revenue growth with 12 consecutive quarters of improving pricing power in a supply-constrained market. Whether Seagate’s premium holds depends on whether the 20%-plus growth target survives into the Mozaic 5 cycle, and management now has more contracted visibility on that question than at any point in the last two years.

The risk is real. Seagate’s revenue fell 36.7% in fiscal 2023. Any material slowdown in hyperscaler capex would compress demand faster than locked-in contracts can fully absorb.

See how Seagate performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $726.93

- Target Price (Mid): ~$1,520

- Potential Total Return: ~109%

- Annualized IRR: ~19% / year

See analysts’ growth forecasts and price targets for Seagate stock (It’s free!) >>>

The TIKR mid-case uses a revenue CAGR of approximately 24% and net income margins of around 41% through 6/30/30. The two primary revenue drivers are AI-driven nearline exabyte demand from hyperscalers and sustained pricing power from a supply-constrained market. The margin driver is the Mozaic platform, where each generation adds capacity without proportional cost increases.

The low case puts STX at around $2,012 by 6/30/30, implying roughly 177% total return and about 13% IRR, under a lower revenue CAGR of approximately 21%. The high case reaches approximately $4,241 with about 24% IRR, requiring a ~26% revenue CAGR and net income margins near 43%. The primary risk across all scenarios is demand cyclicality. If AI capex normalizes by fiscal 2027, the CAGR assumption compresses, and the model’s margin trajectory needs revision.

What changed this quarter is the quality of visibility. Contracts are finalized, pricing is locked, and customers are already planning for 2028. That is a different demand signal than existed 90 days ago.

Conclusion

The metric to watch at the next report, expected around July 23, 2026, per TIKR’s event calendar, is Mozaic 4’s share of total HAMR exabyte shipments. Management has guided it to represent a majority of HAMR output by calendar year-end. If that crossover is on track entering Q4, it confirms both the margin expansion path and the 20%-plus annual revenue growth target Mosley committed to this week. The structural thesis for Seagate is intact. The next several quarters will show whether it compounds.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Seagate?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Seagate, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Seagate alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Seagate on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!