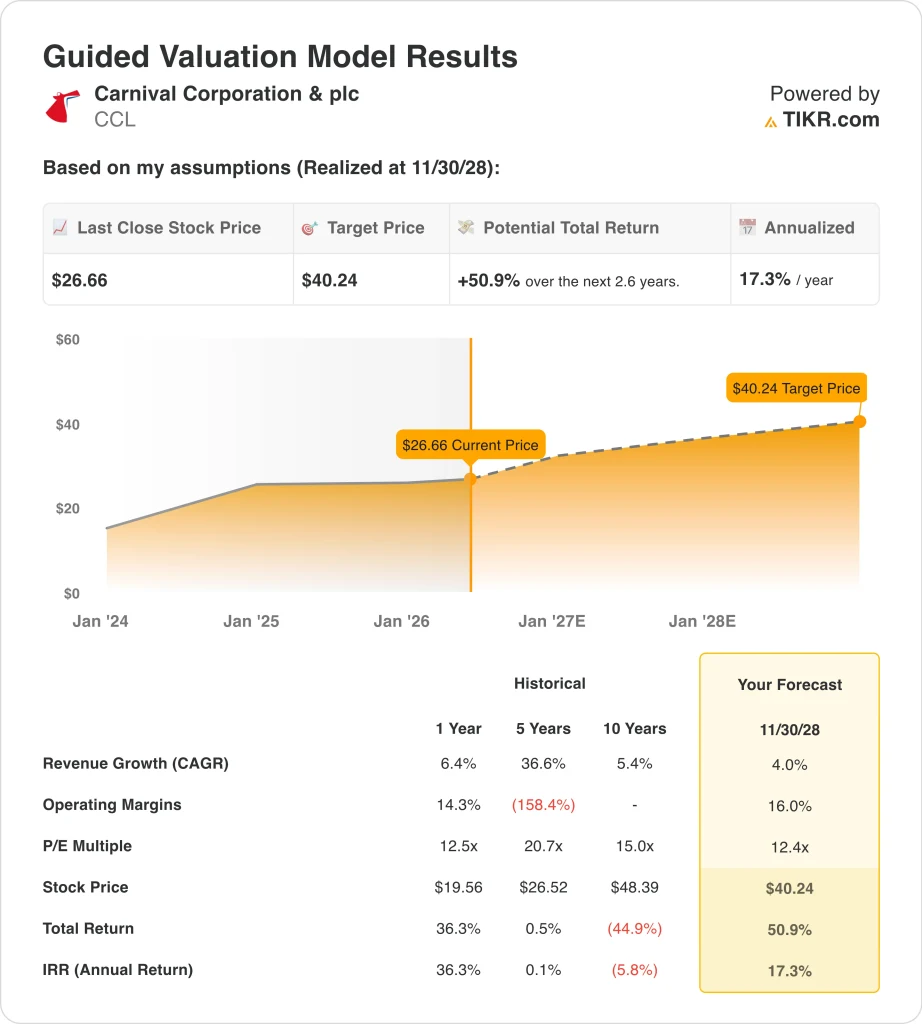

Key Stats for Carnival Stock

- Past week’s performance: Consolidating

- 52-week range: $19 to $34

- Valuation model target price: $40

- Implied upside: 50.9% over 2.6 years

Value your favorite stocks like CCL with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Carnival reported Q1 2026 adjusted EBITDA of $1.3 billion, beating the analyst estimate of $1.26 billion. Royal Caribbean also beat its Q1 estimates on April 30 but flagged higher fuel costs going forward.

Both companies acknowledged that the Iran war-driven fuel price surge is a growing margin headwind. Investors who were excited about Carnival’s record full-year 2025 adjusted net income are now wondering whether that profitability can hold through the rest of 2026.

On the constructive side, Princess Cruises signed a deal with Italian shipbuilder Fincantieri for three new Voyager-class ships worth more than 2 billion euros. That order signals strong confidence in long-term demand.

Shareholders also approved the company’s DLC (dual-listed company) unification plan in April, simplifying Carnival’s complex cross-listed structure across New York and London. DLC unification means both share classes will eventually consolidate, making the stock easier for global institutional investors to own.

Going forward, CCL stock will be largely driven by summer booking trends, fuel price movements, and any guidance update at the Q2 2026 earnings call expected in late June.

See analysts’ growth forecasts and price targets for CCL (It’s free) >>>

Is Carnival Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 4%

- Operating Margins: 16%

- Exit P/E Multiple: 12.4x

Based on these inputs, the model estimates a target price of $40, implying 50.9% total upside from the current share price and a 17.3% annualized return over the next 2.6 years.

The Street consensus target sits near $35, so the valuation model is more bullish, but both agree on meaningful upside. The 12.4x exit P/E is conservative and reflects the discount investors apply to Carnival because of its heavy debt load.

Net debt stands at $25 billion, and the leverage ratio is about 3.3 times EBITDA. But the company is actively paying debt down and reinstated a $0.15 quarterly dividend, signaling confidence in cash generation.

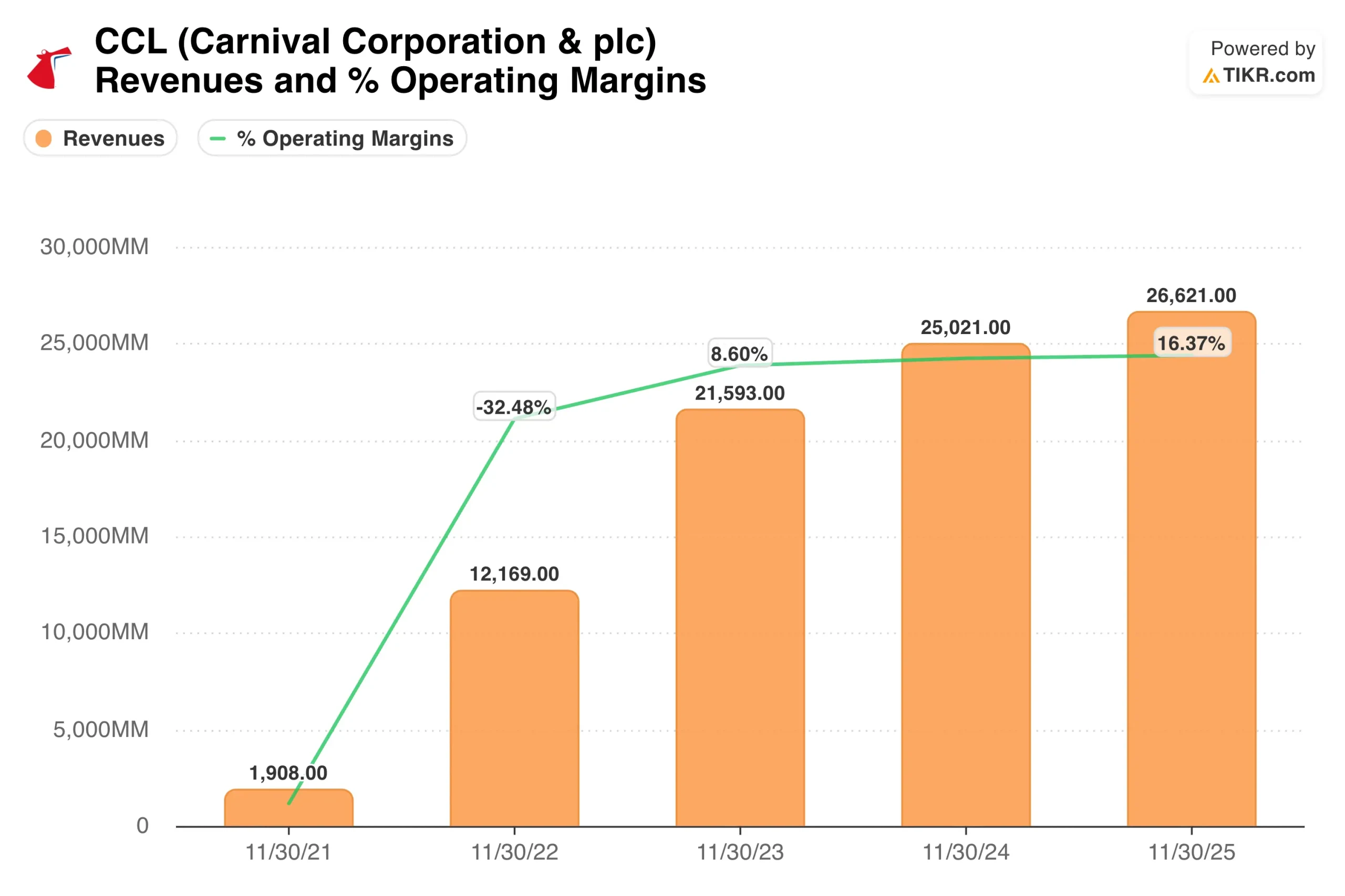

Revenue growth of 4% per year is modest but realistic. Carnival grew revenue 6.4% over the past year, and analysts expect a similar trajectory going forward. Cruise revenue grows primarily through pricing, occupancy gains, and onboard spending rather than aggressive fleet expansion.

Operating margins of 16% are close to the current level, so the model does not require a dramatic margin improvement but does assume fuel costs stabilize and pricing discipline holds.

The valuation looks attractive at around 12 times forward earnings. Peer Royal Caribbean trades at a higher multiple with a lower dividend yield, so Carnival offers a relative value setup. Carnival’s 2.4% dividend yield also provides income support while investors wait for debt to come down.

If bookings remain strong through summer and fuel costs plateau, the stock looks modestly cheap relative to intrinsic value at current levels.

What’s Driving CCL Stock Going Forward?

The biggest near-term catalyst is summer 2026 booking data. Royal Caribbean’s Q1 beat showed North American cruise demand remains strong, but fuel costs are now a meaningful risk to margins.

Carnival’s Q2 2026 earnings, expected around June 22, will reveal whether pricing gains can offset the fuel drag. If average ticket prices continue rising faster than fuel expenses, the earnings setup stays intact, and the stock likely recovers toward analyst targets.

Princess Cruises’ Voyager-class ship order is a long-term capacity growth driver. The three new ships will allow Carnival to serve higher-spending passengers on longer premium itineraries.

New offerings like Holland America Line’s expanded Alaska season and the debut of the Star Princess also add near-term revenue support. These investments take years to pay off, but they build the asset base that drives future free cash flow.

The DLC unification is a structural tailwind worth tracking. Simplifying the dual-listed structure should lower administrative costs and broaden Carnival’s appeal to institutional investors who prefer cleaner share structures.

The company also launched new beverage programs and shore excursion packages across brands in April. Onboard revenue is a high-margin stream, and even modest gains there can improve overall profitability materially.

One near-term risk is the scheduled S&P Global BMI Index removal on May 6. Index-tracking funds may need to sell shares mechanically, adding short-term technical pressure. But that event does not change the fundamental outlook.

Long-term investors may view the mechanical selling as a temporary entry opportunity, especially given the 50.9% implied upside in the valuation model and the improving booking environment.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Carnival?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CCL, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CCL alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Carnival stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!