Key Stats for Alphabet Stock

- Current Price: $385.69

- Target Price (Mid): ~$609

- Street Target: ~$403

- Potential Total Return: ~58%

- Annualized IRR: ~10% / year

- Earnings Reaction: +9.96% (April 30, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Alphabet (GOOGL) Q1 2026 earnings dropped on April 29, and the stock jumped 9.96% the next day. Most investors focused on the headline: $109.9 billion in revenue, Cloud up 63%, Search still accelerating. The number that deserves more attention is buried in CFO Anat Ashkenazi’s segment commentary: a Google Cloud backlog of $462 billion, nearly doubled in a single quarter. Bulls say that figure rewrites the investment case. Bears say the $180 to $190 billion CapEx plan, financing it, is a risk the market hasn’t fully priced. The central question is not whether the AI bet is paying off. It is how much of that $462 billion converts, and how fast.

What the $462 Billion Backlog Actually Means

A cloud backlog is contracted customer commitments not yet recognized as revenue. It is the strongest forward signal a cloud business can produce because it reflects signed contracts, not management projections.

At the end of Q1 2026, Google Cloud’s backlog stood at $462 billion, up from $240 billion at the end of Q4 2025, per Alphabet’s Q1 2026 10-Q filed with the SEC. That is a sequential jump of more than $220 billion in one quarter. Ashkenazi told analysts the increase was driven by “strong demand for enterprise AI offerings and the inclusion of TPU hardware sales.” She added that just over 50% of the backlog is expected to convert to revenue within 24 months, meaning more than $230 billion in already-contracted Cloud revenue is scheduled to be recognized by mid-2028.

CEO Sundar Pichai added the most important detail: “our cloud revenue would have been higher if we were able to meet the demand.” Supply, not demand, is the binding constraint. The backlog is not speculative pipeline. It is revenue waiting on compute capacity to deliver it.

See analysts’ Cloud revenue forecasts for Alphabet (It’s free) >>>

Two Forces That Built the Pipeline

The backlog didn’t nearly double by accident. Two forces drove it during Q1.

The first is Gemini Enterprise, Alphabet’s platform bundling AI agents, data tools, and Gemini models for business use. Paid monthly active users grew 40% quarter over quarter. Alphabet doubled the number of $100 million to $1 billion deals year over year, signed multiple $1 billion-plus contracts, and saw existing customers outpace their initial commitments by 45%. Deepening customer relationships directly converts into backlog.

The second force is new: TPU hardware sales to third parties. Tensor Processing Units (TPUs) are Alphabet’s proprietary AI chips built for machine learning workloads. For the first time, Alphabet has agreed to deliver TPUs directly into select customers’ own data centers, targeting capital markets firms, frontier AI labs, and high-performance computing operators, per Pichai. These agreements are already embedded in the $462 billion backlog. Ashkenazi said a small percentage of that revenue will be recognized in 2026, with the majority arriving in 2027.

That timing matters. Cloud’s quarterly revenue growth rate may appear to soften in Q2 and Q3 2026 even as underlying demand stays strong, because hardware revenue recognition is back-weighted. Sequential Cloud growth numbers over the next two quarters should be read with that dynamic in mind.

Search Answered Its Critics

The Cloud story would be less compelling if Search were slipping. It isn’t.

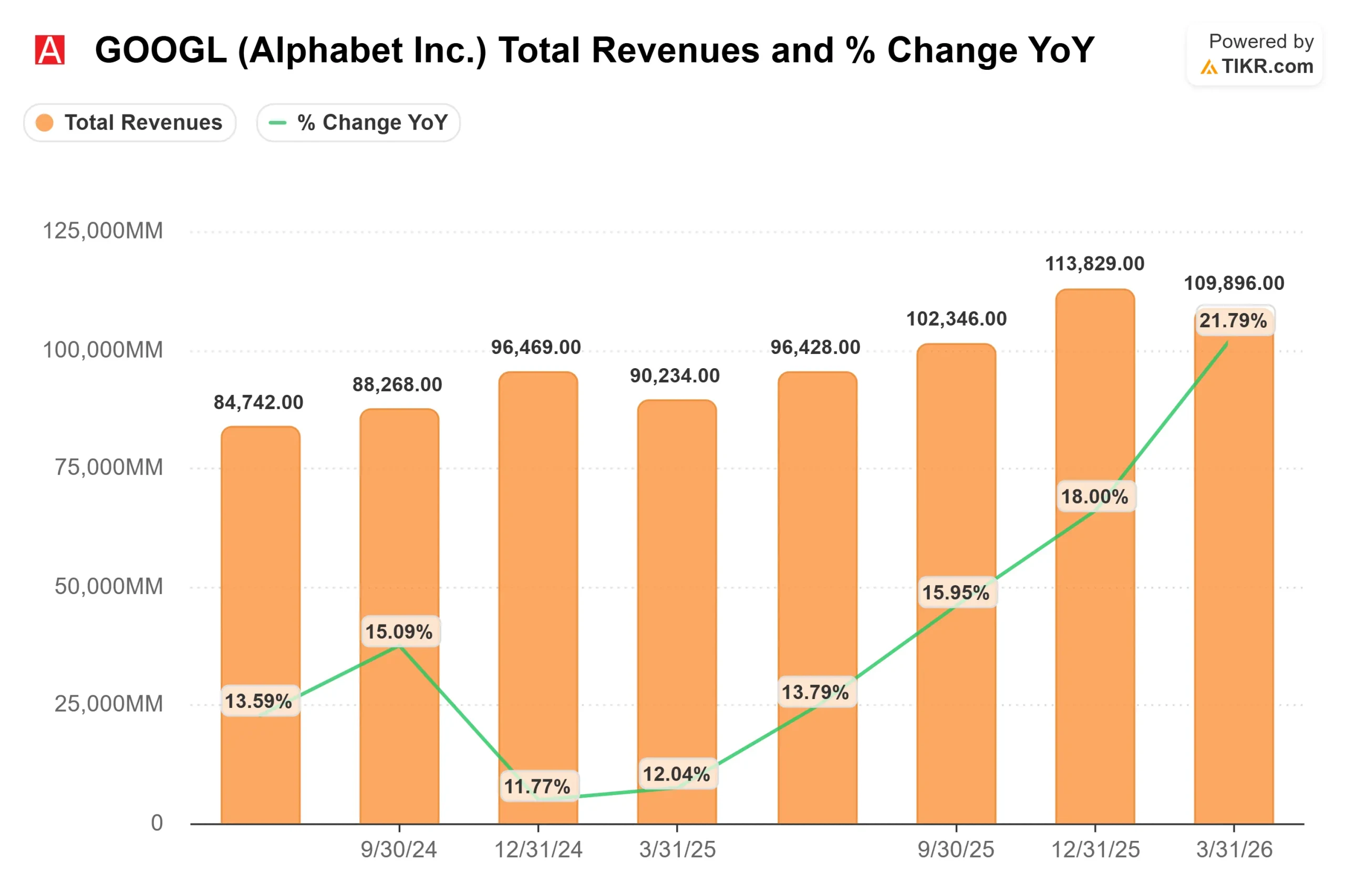

Google Search and Other advertising revenue grew 19% year over year to $60.4 billion in Q1 2026, an acceleration from 17% growth in Q4 2025 per Alphabet’s Q4 2025 earnings release. Pichai said search queries are at an all-time high. AI Overviews (AI-generated answer summaries above traditional results) and AI Mode (a conversational search interface) are pulling more queries, not fewer, directly rebutting two years of concern that AI chatbots would erode Google’s dominance.

Chief Business Officer Philipp Schindler added a forward signal: historically, around 20% of search queries carry ads. He told analysts there is “upside in that coverage number” as Gemini’s improved intent understanding opens monetization of longer, more complex queries “that were previously really difficult to monetize.” On a $60-billion-per-quarter base, even a modest increase in coverage rate is material.

YouTube advertising came in at $9.9 billion for the quarter. Subscriptions were the stronger story: YouTube Music and Premium posted their largest quarterly increase in non-trial subscribers since YouTube Premium launched in June 2018, per Pichai. Total paid subscriptions across Alphabet reached 350 million.

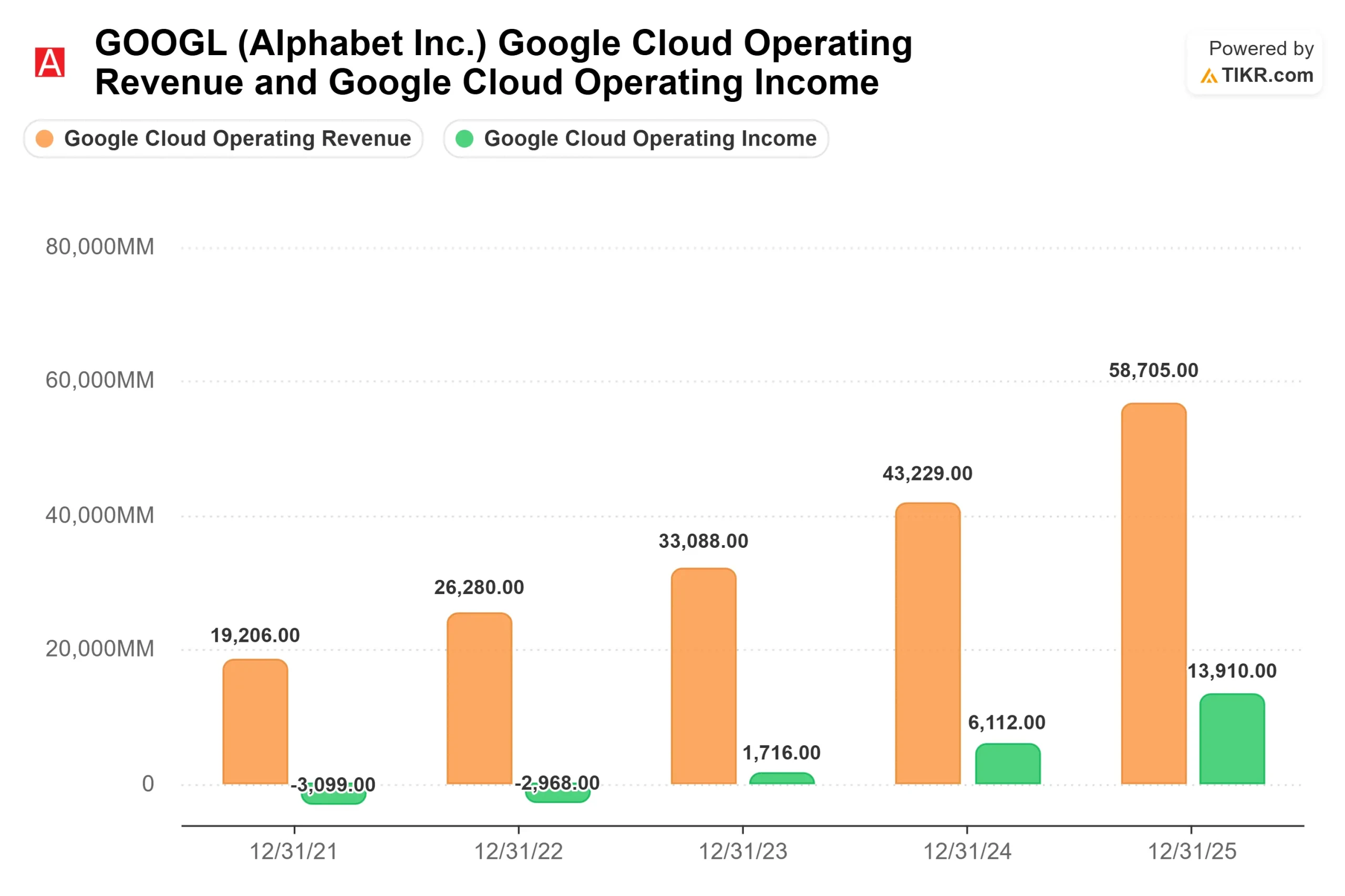

On valuation, Alphabet’s closest large-cap peer Meta Platforms (META) trades at 18.77x NTM P/E versus Alphabet’s 30.89x, and 10.27x NTM EV/EBITDA versus Alphabet’s 19.33x, per TIKR’s Competitors page. That premium reflects Cloud’s acceleration and Alphabet’s position as the only hyperscaler offering a vertically integrated AI stack from silicon to application. Cloud margin expanded from a loss in 2022 to 32.9% in Q1 2026, and sustaining margin above 30% through the Wiz integration, which Ashkenazi guided as a low-single-digit percentage point drag on Cloud margins for the rest of 2026, is the near-term test of that premium.

Wall Street is broadly constructive: 46 Buys, 13 Outperforms, 5 Holds, 2 Underperforms, and 0 Sells among analysts tracked by TIKR, with a mean Street target of around $403.

See how Alphabet performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $385.69

- Target Price (Mid): ~$609

- Potential Total Return: ~58%

- Annualized IRR: ~10% / year

See analysts’ growth forecasts and price targets for Alphabet stock (It’s free!) >>>

The TIKR mid-case model uses a revenue CAGR of around 14% through December 31, 2030, and a net income margin of around 34%, arriving at a target of approximately $609 per share. That is around 58% total return from $385.69, or around 10% annualized. For a stock already at an all-time high, that is a reasonable but not spectacular setup.

The two revenue drivers are Google Cloud and Search. The $462 billion backlog and the acceleration from 48% to 63% Cloud growth in a single quarter provide the compounding base. Schindler’s comments on ad coverage expansion in AI Mode add upside to the Search line. The margin driver is Cloud operating leverage: margin expanded from a loss in 2022 to 32.9% in Q1 2026, and the mid-case assumes further expansion as infrastructure utilization rises.

The primary risk is CapEx overshoot. Alphabet raised 2026 CapEx guidance to $180 to $190 billion, and management said 2027 CapEx is expected to increase significantly from that level. TIKR consensus estimates show 2026 free cash flow compressing to approximately $20.5 billion from 2025’s $73.3 billion, recovering to approximately $35.5 billion in 2027 and $68.1 billion in 2028 as the investment cycles through depreciation. A secondary risk is the DOJ’s pending adtech remedies ruling, which could force a divestiture of Google’s Ad Exchange (Alphabet’s digital advertising marketplace) and remove material revenue from the model.

Conclusion

Watch Google Cloud revenue growth at Q2 2026 earnings, expected in late July. The threshold: a print above 55% confirms backlog conversion is on schedule and that TPU hardware timing isn’t creating a gap in recognized revenue. Management said supply is the only constraint. If the CapEx delivers the capacity, the $462 billion backlog does the rest.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Alphabet?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Alphabet, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Alphabet alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Alphabet on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!