Key Stats for Sandisk Stock

- Current Price: $1,187

- Target Price (Mid Case): ~$1,328

- Target Price (High Case): ~$1,558

- Street Target Mean: ~$1,062

- Potential Total Return (High Case): ~31%

- Annualized IRR (High Case): ~3% per year

- Earnings Reaction: +8.25% (April 30, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

SanDisk (SNDK) jumped 8.25% on May 1, 2026, after reporting one of the most dramatic earnings beats in recent semiconductor history. Based on TIKR data, the stock has risen more than 330% year-to-date, from a January 2, 2026, close of $275.24 to $1,187.00. Bulls see a company that has permanently repriced its earnings power through multiyear customer contracts. Bears think 80% gross margins in a commodity memory market are a cycle peak, not a new normal. The central question: can Sandisk actually lock in these margins?

The answer depends on five contracts CEO David Goeckeler calls new business models, or NBMs.

A Quarter That Didn’t Look Like a NAND Company

Sandisk reported Q3 FY2026 revenue of $5,950 million, up 97% sequentially and 251% year-over-year, against guidance of $4,400 million to $4,800 million. Non-GAAP gross margin hit 78.4%, up from 51.1% the prior quarter, well above the 65% to 67% guidance range. Non-GAAP EPS came in at $23.41 against a consensus estimate of $14.66, a 59.67% beat.

The data center was the growth engine. Revenue in that segment grew 233% sequentially to $1,467 million, driven by Sandisk’s TLC-based enterprise SSD portfolio. TLC, or triple-level cell, is a flash memory format prioritizing speed and low latency, making it the go-to choice for AI inference workloads. Edge revenue grew 118% sequentially to $3,663 million. Consumer came in at $820 million, down 10%, in line with seasonal norms.

See historical and forward estimates for SanDisk stock (It’s free!) >>>

The NBM Contracts: What They Are and Why They Matter

Three NBM agreements were signed during Q3, and two more were added in the first weeks of Q4 FY2026. The three Q3 contracts alone carry a minimum contractual revenue of approximately $42 billion, which will appear in Sandisk’s 10-Q as remaining performance obligations. Across all five agreements, financial guarantees exceed $11 billion, with $400 million in prepayments already on the Q3 balance sheet. These NBMs cover over one-third of Sandisk’s expected bit shipments in fiscal year 2027.

The structure is straightforward. As Goeckeler explained on the call: “We run a fab. We have very consistent output. We need very consistent consumption.” Customers get a guaranteed supply for up to five years. SanDisk gets committed demand backed by financial instruments held by third-party institutions. If a customer misses its quarterly purchase commitment, the financial guarantee triggers immediately.

Pricing inside the contracts blends fixed and variable components. Near-term pricing is mostly fixed, CFO Luis Visoso said, while longer-dated portions carry more variable elements. That variable structure is also the bear case: if NAND capacity expands industry-wide and spot prices fall, the variable portions of these contracts could erode margins faster than the backlog suggests. Morgan Stanley, Citigroup, and BNP Paribas have said the structure should reduce cyclicality and support more stable long-term returns. Not all analysts are fully convinced.

Q4 Guidance and the Buyback

Management guided Q4 FY2026 revenue of $7,750 million to $8,250 million, with non-GAAP gross margin of 79% to 81% and EPS of $30 to $33, assuming 158 million fully diluted shares. Both ranges were roughly double what analysts had modeled before the print.

Two Q4 catalysts drive that guidance.

First, Sandisk expects to begin shipping its QLC Stargate product for revenue. QLC, or quad-level cell, stores more data per chip than TLC at a lower cost per bit, suited for high-density AI storage deployments. Stargate has been in hyperscaler qualification for over a year.

Second, Sandisk deliberately built BiCS8 QLC inventory during Q3, which is why bit shipments fell high-teens sequentially even as revenue surged. The inventory build was preparation for the ramp, not a demand signal. The company also announced a $6 billion share buyback with no expiration date. Sandisk closed Q3 with $3,735 million in cash and no debt after repaying the remaining $650 million on its term loan. Free cash flow reached $2,955 million in Q3, a 49.7% margin, giving the buyback a clean funding source without requiring new leverage.

Sandisk trades at 4.69x NTM EV/Revenue and 6.09x NTM EV/EBITDA per TIKR. Western Digital (WDC) trades at 9.20x NTM EV/Revenue and 19.17x NTM EV/EBITDA. Samsung Electronics trades at 1.85x NTM EV/Revenue and 2.95x NTM EV/EBITDA, reflecting its broader diversification across consumer electronics and displays. On these figures, Sandisk is cheaper than Western Digital on an EBITDA basis and carries a premium to Samsung’s blended multiple.

The Street mean target of $1,061.67 sits below the current price, but that consensus was set before the Q3 print. Post-earnings, Bernstein raised its target to $1,700 with an Outperform rating, Goldman Sachs raised to $1,200, Bank of America raised to $1,550, and Susquehanna set a target of $2,000.

See how Sandisk performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

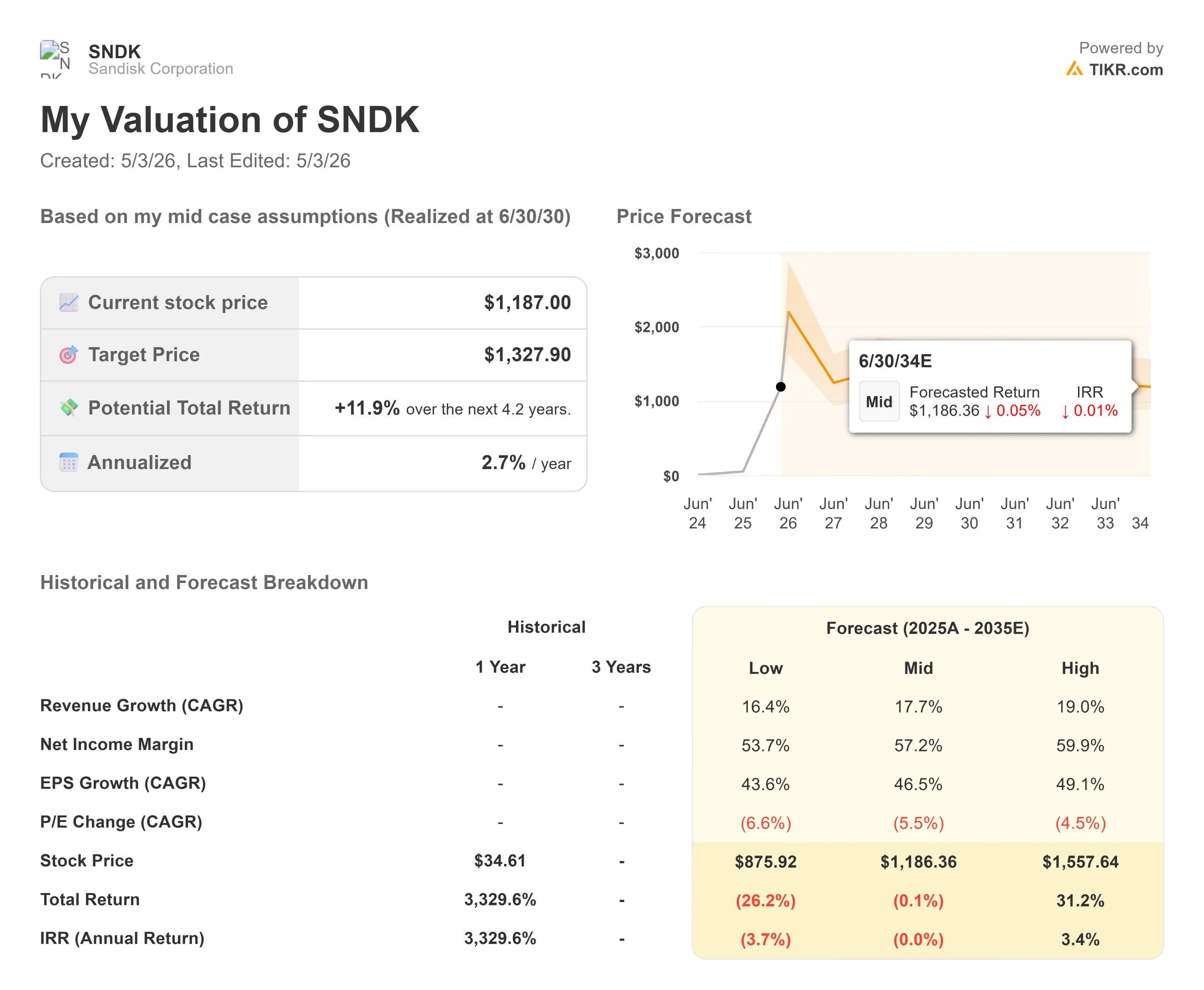

- Current Price: $1,187

- Target Price (High Case): ~$1,558

- Potential Total Return (High Case): ~31%

- Annualized IRR (High Case): ~3% per year

See analysts’ growth forecasts and price targets for SanDisk stock (It’s free!) >>>

The TIKR mid-case, realized at 6/30/30, projects a target of ~$1,328 with +11.9% total return and a 2.7% annualized IRR. That is a thin return for a stock that has already compounded more than 330% in a single year. The high case at ~$1,558 implies ~31% total return and a ~3% IRR, driven by a revenue CAGR of around 19% and a net income margin of around 60%. Two forces drive that scenario: accelerating data center revenue from AI inference workloads, and operating leverage as non-GAAP opex already fell to 7.5% of revenue in Q3 from 13.7% the prior quarter.

The primary risk is pricing durability. At ~80% gross margins, Sandisk is operating like a pricing-power compounder inside a historically cyclical commodity market. If NAND supply grows faster than demand and customers renegotiate the variable portions of NBM contracts unfavorably, margins can compress quickly. The low-case model projects a stock price of ~$876, a 26% decline from current levels, reflecting that scenario. The honest read: even the high case implies modest IRR from this price. What the model cannot capture is whether the NBM structure permanently shifts the multiple the market assigns to NAND earnings. If it does, the stock is underpriced. If it doesn’t, current margins will mean-revert, and the price will look expensive in hindsight.

Conclusion

The metric to watch at Q4 FY2026 earnings is the NBM bit coverage percentage. Management said over one-third of fiscal 2027 bits are under contract today and expects that share to grow. If it crosses 50%, the de-cyclicalization thesis gains real credibility. If it stalls below 40%, the variable pricing risk moves to the front of the debate. SanDisk is no longer just a storage company. It is a test of whether a NAND manufacturer can earn a software-style multiple.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Sandisk?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up SanDisk, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track SanDisk alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze SanDisk on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!