Key Stats for SoFi Technologies Stock

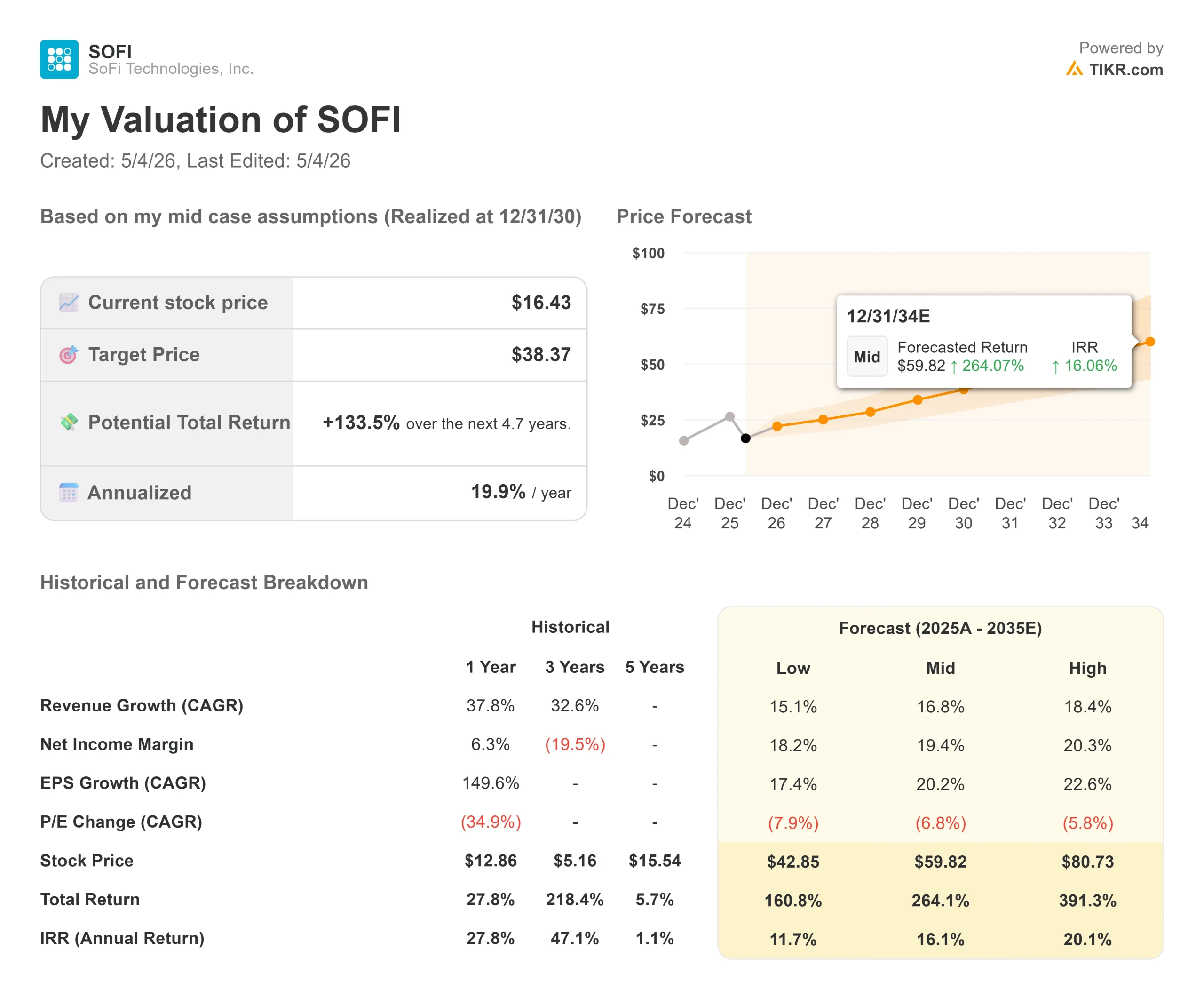

- Current Price: $16.43

- Target Price (Mid): ~$38

- Street Target: ~$22

- Potential Total Return: ~134%

- Annualized IRR: ~20% / year

- Earnings Reaction: -2.13% (4/28/26)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Fintech investors are watching a strange disconnect. SoFi Technologies (SOFI) posted its strongest quarter on record on April 29, beat revenue estimates by 4%, doubled net income year-over-year, and logged its tenth consecutive profitable quarter. The stock fell. Bears say SoFi is a lender with contested accounting. Bulls say the market is pricing a short-seller narrative over the actual business. The question that matters at $16: Does what the earnings call revealed support owning SOFI?

SoFi’s investor relations materials show a company reporting $1.087 billion in Q1 adjusted net revenue, ahead of the $1.049 billion consensus, alongside a 31% EBITDA margin and a Rule of 40 score of 72 for the 18th consecutive quarter. The Rule of 40 combines revenue growth rate and EBITDA margin as a measure of high-growth business efficiency.

The sentiment backdrop is genuinely ugly. On March 17, Muddy Waters Research published a short report calling SoFi a “financial engineering treadmill” and alleging at least $312 million in unrecorded debt. SoFi called the report “factually inaccurate and misleading” and said it would explore legal action. CEO Anthony Noto purchased $500,000 of shares shortly after. By March 30, SOFI had already fallen 52.96% from its late-2025 peak. Q1 earnings arrived strongly, and the stock still fell. What the market appeared to miss was what was inside the numbers.

What the Record Quarter Actually Shows

Adjusted EBITDA hit $340 million in Q1 2026, up 62% year-over-year, at a 31% margin. Net income was $167 million, more than double the $71 million from Q1 2025. SoFi added a record 1.1 million new members in Q1, bringing total membership to 14.7 million, up 35% year-over-year. Total products reached 22.2 million, up 39%. Forty-three percent of new products in Q1 were opened by existing members, up from 36% in Q1 2025. More existing members adding more products means SoFi collects more revenue without paying to acquire those customers again.

The most significant disclosure on the call was SoFi’s first-ever cash revenue breakdown. CFO Chris Lapointe stated that SoFi generated over $1 billion in cash revenue in Q1: roughly $690 million from net interest income and roughly $390 million from interchange, brokerage, technology platform, origination, and loan platform fees.

He added that “100% of our reported adjusted net revenue was cash revenue in both 2024 and 2025.” The Muddy Waters report alleged that fair value accounting inflated earnings. The cash revenue disclosure is the direct rebuttal: the revenue reflects actual cash collected, not a mark-to-market adjustment.

See historical and forward estimates for SoFi Technologies stock (It’s free!) >>>

The Credit Data Bears Need to Address

The bear case rests on credit risk. Q1 delivered a direct test.

The personal loan net charge-off (NCO) rate, meaning the share of outstanding loans written off as losses, was 4.4% annualized, excluding delinquent loan sales, flat to Q4 and down roughly 40 basis points from Q1 2025. Including delinquent loan sales, it was 3.03%. The 90-day delinquency rate was 47 basis points, down 5 basis points from the prior quarter.

Lapointe walked through cohort data on the call: the Q4 2022 through Q2 2025 vintage loans are running at 4.64% net cumulative losses with 36% of principal still outstanding, compared to 6.32% at the same point for the 2017 vintage, the last time SoFi approached its 7% to 8% loss tolerance. That gap has widened for seven consecutive quarters. For charge-offs to reach the 8% threshold on the remaining book, the rate on remaining unpaid principal would need to reach approximately 10%, well above any comparable historical point in loan seasoning, per Lapointe’s math.

SoFi’s personal loan borrowers carry a weighted average income of $154,000 and a weighted average FICO score of 745. Student loan borrowers average $161,000 in income and a 767 FICO score. The credit bear case requires a deterioration that the existing cohort data does not support.

Three Things the Sell-Off Ignored

Forbes named SoFi the number one U.S. bank in its World’s Best Banks 2026 ranking, based on a survey of over 54,000 consumers. J.D. Power ranked SoFi number one in its 2026 U.S. Investor Satisfaction Study for do-it-yourself investing. Unaided brand awareness reached 10% in Q1, up 300 basis points year-over-year per Noto on the call. Brand trust with younger depositors lowers future acquisition costs as those members need more products.

SoFi Plus relaunched on April 1 as a paid subscription at $10 per month. The product now includes 4.5% APY on deposits up to $20,000, a 1% match on taxable investment account deposits, and unlimited sessions with financial planners. Noto said on the call that 50% of members who sign up for Plus subsequently open an additional product. That makes Plus both a recurring revenue stream and a cross-sell accelerator.

Big Business Banking and SoFiUSD, launched in April 2026, the platform lets companies hold deposits, make payments, and settle transactions in both traditional dollars and digital assets in real time through SoFiUSD, the company’s own stablecoin introduced in December 2025.

Management stated on the call that SoFi is the first nationally chartered U.S. bank to have launched its own stablecoin on a public permissionless blockchain. A Mastercard partnership enables SoFiUSD settlement across Mastercard’s global payments network. Revenue here will take time to scale, but the regulatory position as a licensed bank offering real-time fiat and crypto settlement is currently unique.

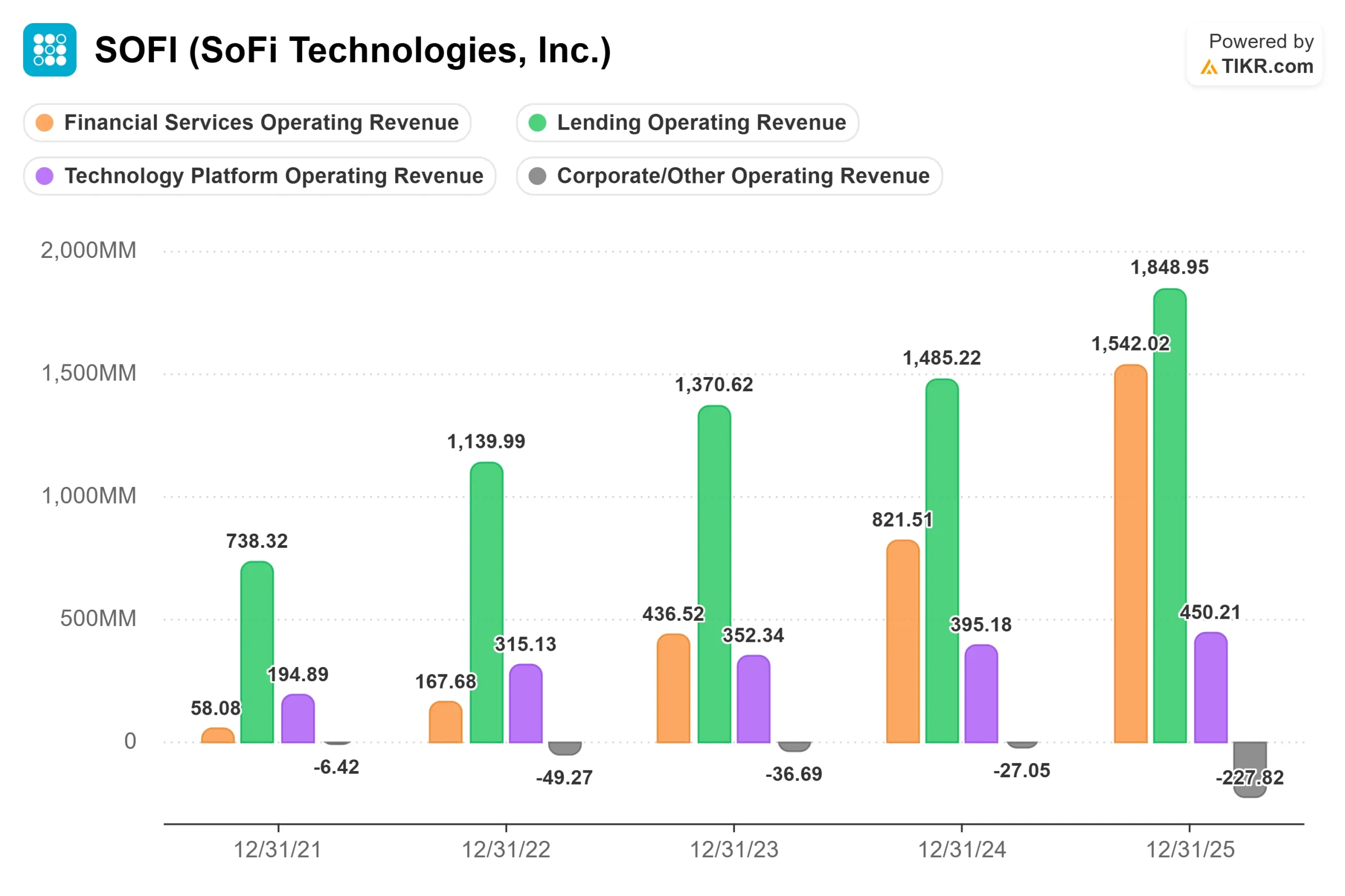

On the segment level, Financial Services revenue grew 41% year-over-year to $429 million in Q1. The Technology Platform came in at $75 million, hit by the previously disclosed exit of Chime. Excluding that client, tech platform revenue grew roughly 12% year-over-year, with 13 new clients from Q1 scaling through the year.

See how SoFi Technologies performs against its peers in TIKR (It’s free!) >>>

Valuation Relative to Peers

At $16.43, SoFi trades at 25.42x next twelve months earnings and 12.45x NTM market cap to free cash flow, per TIKR data. The consumer finance peer group on TIKR shows Ally Financial at 7.69x, SLM Corporation at 8.67x, Upstart Holdings at 14.39x, and LendingClub at 9.58x forward earnings. SoFi’s premium to all of them is real. Whether it is justified depends on whether SoFi is a lender with a tech wrapper or a financial platform with a lending segment inside it. The cross-sell data, SoFi Plus traction, and stablecoin positioning suggest the latter. The current price reflects the former.

See how SoFi Technologies performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $16.43

- Target Price (Mid): ~$38

- Potential Total Return: ~134%

- Annualized IRR: ~20% / year

See analysts’ growth forecasts and price targets for SoFi Technologies stock (It’s free!) >>>

This article uses the TIKR mid-case, which is the scenario most directly supported by Q1 2026 results. The two revenue CAGR drivers are continued member growth and cross-sell within Financial Services, and scaling of the Loan Platform Business, which added $3.6 billion in new partner commitments in Q1 alone. The margin driver is operating leverage: fixed infrastructure costs across the bank charter, Galileo, Technisys, and Big Business Banking now spread over a rapidly growing revenue base. The mid-case projects net income margins reaching around 19% by 12/31/30, against the 15% already reported in Q1 2026.

The upside, if credit holds and non-lending revenue sustains its trajectory, is approximately $38 by December 31, 2030: roughly 134% total return and roughly 20% annualized from today. The downside is a retest of the $12 to $14 range if personal loan charge-offs rise materially and compress fair value marks on the loan portfolio. The Street sits more conservatively at a mean target of around $22 across 20 analysts, with 5 Buys, 3 Outperforms, 12 Holds, 2 Underperforms, and 2 Sells per TIKR. Even that consensus implies roughly 34% upside from current levels.

Conclusion

Watch the personal loan net charge-off rate at Q2 earnings on July 28, 2026. If it holds at or below 3.03% while originations remain at record levels, the credit bear case weakens, and the case for re-rating SoFi as a platform rather than a lender becomes harder to dismiss. The one-sentence thesis: SoFi is priced like a lender the market no longer trusts, but the Q1 numbers show a platform business with accelerating cross-sell, improving credit cohorts, and a stablecoin infrastructure layer no traditional bank currently has.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in SoFi Technologies?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up SoFi Technologies, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track SoFi Technologies alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze SoFi Technologies on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!