Key Stats for Microsoft Stock

- Current Price: $414.44

- Target Price (Mid): ~$840

- Street Target: ~$563

- Potential Total Return: ~103%

- Annualized IRR: ~19% / year

- Earnings Reaction: -3.93% (April 29, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Microsoft (MSFT) posted one of its strongest quarters in years on April 29, and the stock fell nearly 4% anyway. According to CNBC, MSFT was already down 12% year-to-date heading into earnings, following its worst quarterly stock performance since 2008. Bulls said the quarter would finally prove that the AI infrastructure spending was working. Bears said $190 billion in guided capital expenditures confirmed returns were still too far away. The results landed in the bulls’ column on nearly every metric. The question investors are now asking is whether the market mispriced a turning point.

Every Metric Beat. The Stock Still Dropped.

Microsoft’s press release confirmed revenue of $82.9 billion for the quarter ended March 31, up 18% year-over-year, with EPS of $4.27 on a GAAP basis, up 23%. Per TIKR’s Beats & Misses data, the average analyst revenue estimate was $81.43 billion, making the beat 1.79%. EPS of $4.27 cleared the $4.06 adjusted consensus by 5.22%.

Azure, the cloud platform underpinning Microsoft’s AI business, grew 40% in constant currency, ahead of the roughly 39% analysts expected. CFO Amy Hood stated results exceeded expectations “across revenue, operating income, and earnings per share, driven by strong demand and execution.”

The AI-specific numbers were the headline. CEO Satya Nadella said Microsoft’s AI business surpassed a $37 billion annual revenue run rate, up 123% year-over-year. Microsoft 365 Copilot, the AI productivity add-on for commercial Office users, reached over 20 million paid seats, up 250% year-over-year from 15 million the prior quarter. Nadella put the usage milestone plainly: “Weekly engagement is now at the same level as Outlook, as more and more users make Copilot a habit.”

See historical and forward estimates for Microsoft stock (It’s free!) >>>

What the Call Says That the Headlines Missed

Three disclosures from the call matter for the long-term thesis and received little attention post-earnings.

The first is usage depth behind seat growth. Nadella said first-party agent monthly active usage is up 6x year-to-date, with Copilot queries per user rising nearly 20% quarter-over-quarter. That is compounding intensity on top of seat growth.

The second is the contracted revenue backlog. Hood disclosed that remaining performance obligations (the total value of contracted future revenue) reached $627 billion, up 99% year-over-year. About 25% of that $627 billion will convert to recognized revenue in the next 12 months, itself up 39% year-over-year.

The third is the business model shift. The call was Microsoft’s clearest articulation yet of a move from per-seat to seat-plus-consumption pricing. Nadella said: “Any per-user business of ours, whether it’s productivity, coding, security, will become a per user and usage business.” Nearly 60% of customer service customers are already purchasing usage-based credits. GitHub Copilot moved to consumption-based pricing effective June 1, 2026. A consumption layer on top of seat revenue expands free cash flow per customer without requiring new seat sales.

The OpenAI Deal: Better Than the Headline

Two days before earnings, Microsoft and OpenAI announced a revised partnership ending Microsoft’s revenue-sharing payments to OpenAI and making the OpenAI license non-exclusive, allowing OpenAI to serve products on rival cloud providers. The headline spooked investors. The actual structure is more favorable for Microsoft.

Under the revised agreement, Microsoft retains a 27% stake in OpenAI, remains its primary cloud provider, and continues to receive a 20% share of OpenAI’s revenue through 2030, with royalty-free access to OpenAI’s IP through 2032. Hood was direct on the call: “Having the revenue share exist through 2030, the predictability of that is a real positive for us, and the IP being royalty-free with the elimination of our rev share to them.” Microsoft stops paying out and keeps collecting. Margins improve directly.

The loss of exclusivity is real, but Microsoft has spent two years building model diversity into its own platform. Nadella noted that over 10,000 customers have used more than one model on Azure Foundry, with the number using both Anthropic and OpenAI models doubling quarter-over-quarter. Microsoft’s competitive advantage is increasingly the platform, not any single model relationship.

See how Microsoft performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $414.44

- Target Price (Mid): ~$840

- Potential Total Return: ~103%

- Annualized IRR: ~19% / year

See analysts’ growth forecasts and price targets for Microsoft stock (It’s free!) >>>

The mid-case uses a revenue CAGR of around 15%, driven by two engines: Azure taking enterprise cloud market share as AI workloads scale, and Microsoft 365 Copilot deepening monetization as the seat-plus-consumption model matures. TIKR’s Actuals and Forward Estimates data show consensus revenue reaching approximately $601 billion by fiscal 2030, up from $282 billion in fiscal 2025, which is consistent with the mid-case assumption.

The margin driver is operating leverage in the Productivity and Business Processes segment, where net income margins are expected to expand to around 39% from 36% today as the infrastructure build cycle peaks. LTM ROIC (return on invested capital) sits at 27.4% per TIKR, reflecting current capex pressure. As new capacity converts to productive revenue, that figure should recover.

The primary risk is timing. Hood confirmed supply will remain constrained at least through calendar 2026. Free cash flow for the quarter was $15.8 billion, well below the operating cash flow of $46.7 billion, because $31.9 billion in capital expenditures consumed the gap. TIKR consensus estimates show free cash flow declining year-over-year in fiscal 2026 before recovering sharply from fiscal 2028 onward. A delay in that recovery keeps the multiple compressed even if revenue holds.

The Street is less optimistic than the TIKR mid-case. TIKR’s Street Targets data shows a mean analyst price target of ~$563, with 42 Buys, 9 Outperforms, 3 Holds, 2 Underperforms, and 0 Sells across 56 analysts as of May 1, 2026, implying around 36% upside from current levels, roughly half the return the TIKR mid-case implies. That gap reflects what the model prices in: that seat-plus-consumption monetization compounds more aggressively than current Street estimates assume once the capex cycle turns.

Conclusion

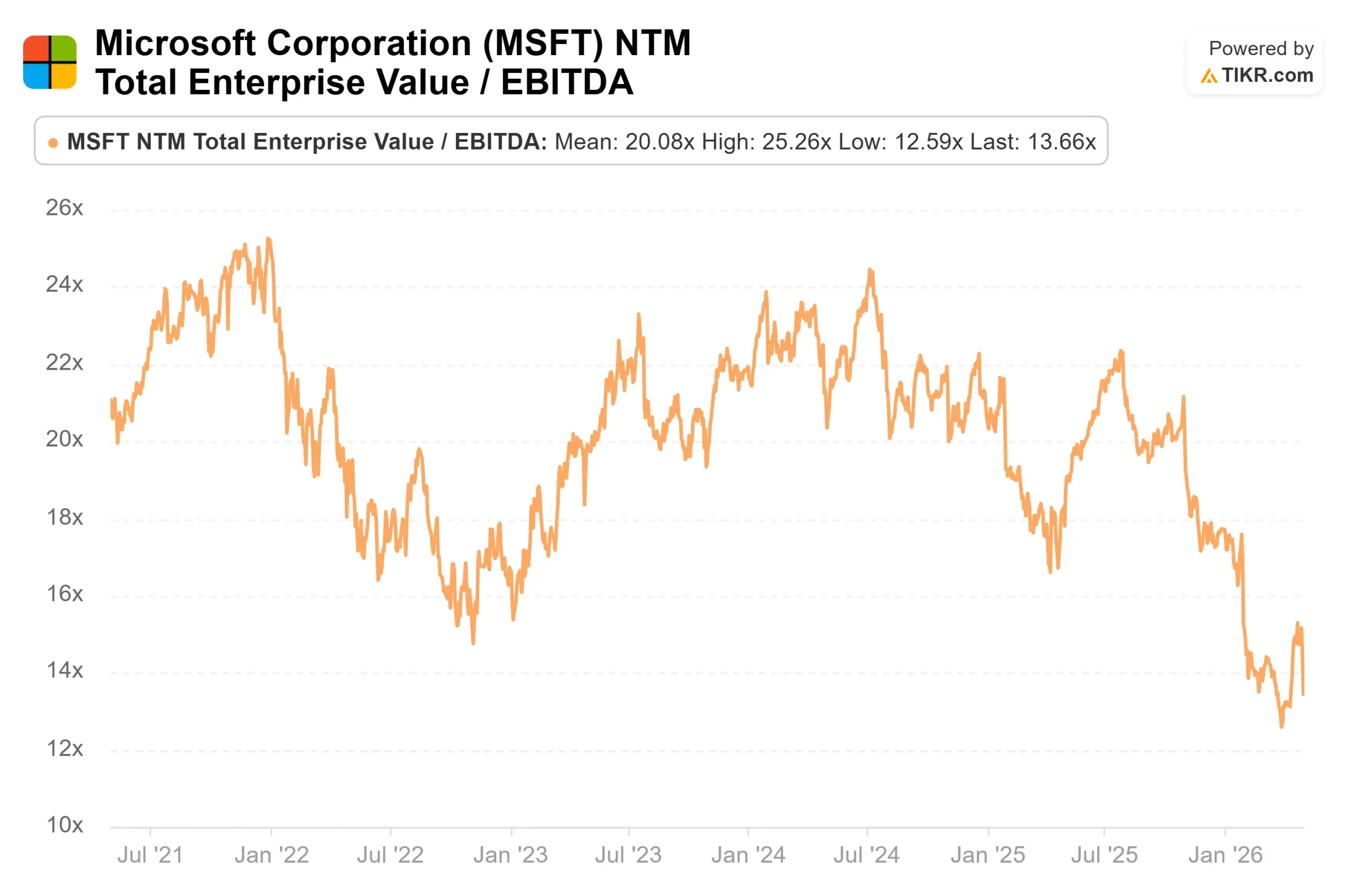

The single metric to watch at Q4 fiscal 2026 earnings (expected July 29, 2026) is Azure constant-currency revenue growth against Hood’s guided range of 39% to 40%. Any print above that range, paired with a sequential improvement in free cash flow margin, is the first concrete signal the infrastructure cycle has peaked. At $414.44, Microsoft trades at a multi-year low on NTM EV/EBITDA with a $627 billion contracted backlog and 20 million Copilot seats growing at 250% annually. The post-earnings selloff looks like the market pricing the capex risk it can see while discounting the monetization it cannot yet fully model.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Microsoft?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Microsoft, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Microsoft alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Microsoft on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!