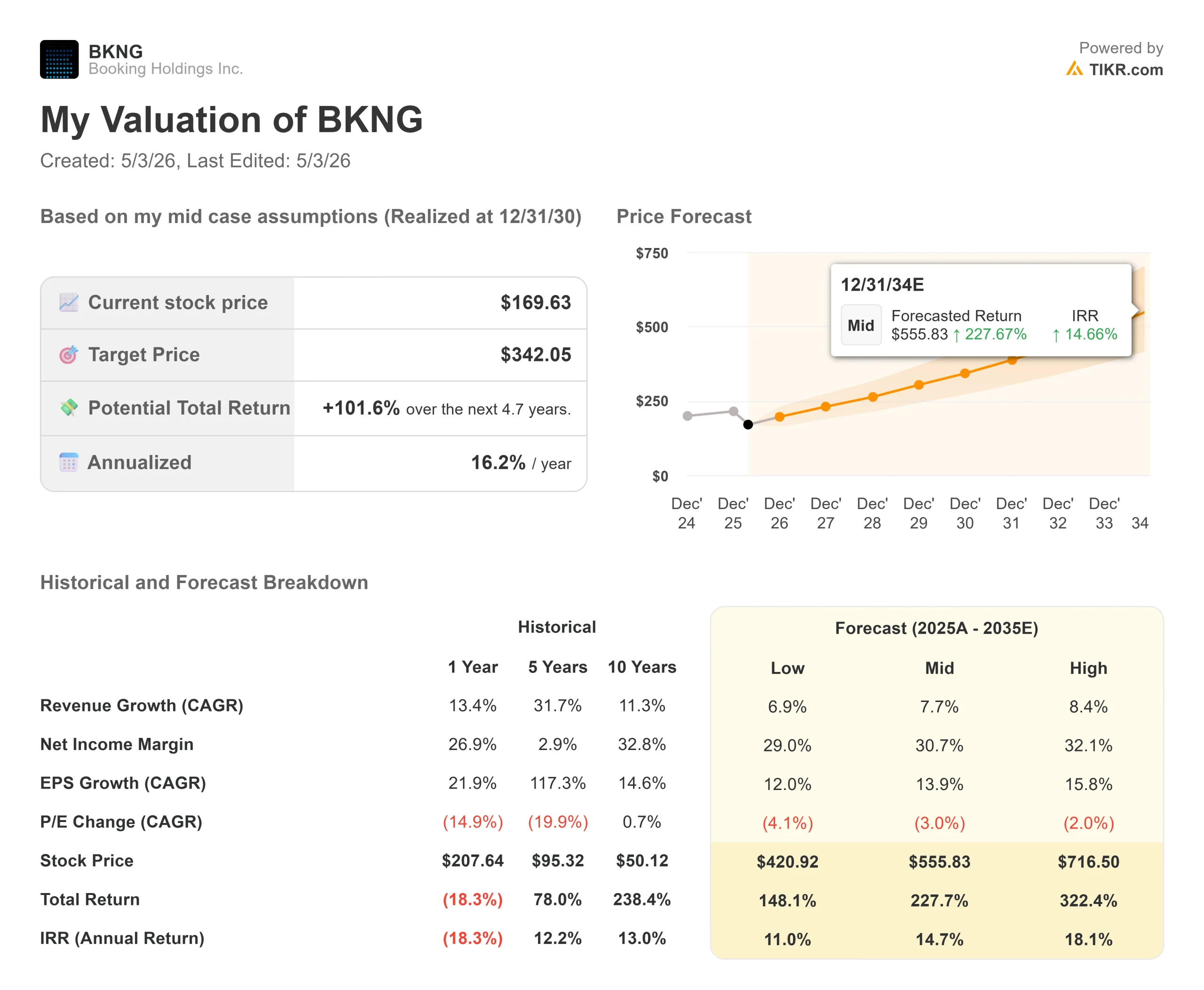

Key Stats for Booking Holdings Stock

- Current Price: $169.63

- Target Price (Mid): ~$342

- Street Target: ~$224

- Potential Total Return: ~102%

- Annualized IRR: ~16% / year

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Travel investors are staring at a split screen. Booking Holdings (BKNG) beat every Q1 2026 estimate, posted its strongest U.S. growth in years, and bought back a record $3.6 billion of its own stock in a single quarter. Then it cut its full-year guidance on the same call. BKNG now sits at $169.63, down 27% from its 52-week high of $233.58 and trading at its lowest forward EV/EBITDA in at least two years. Bulls say the selloff prices a temporary geopolitical shock as if it were permanent damage. Bears say Q2 guidance of just 2% to 4% room night growth means more pain before any recovery. The question every investor is asking: is this a great business available at a rare discount, or is $169 still not cheap enough?

What Q1 Actually Showed

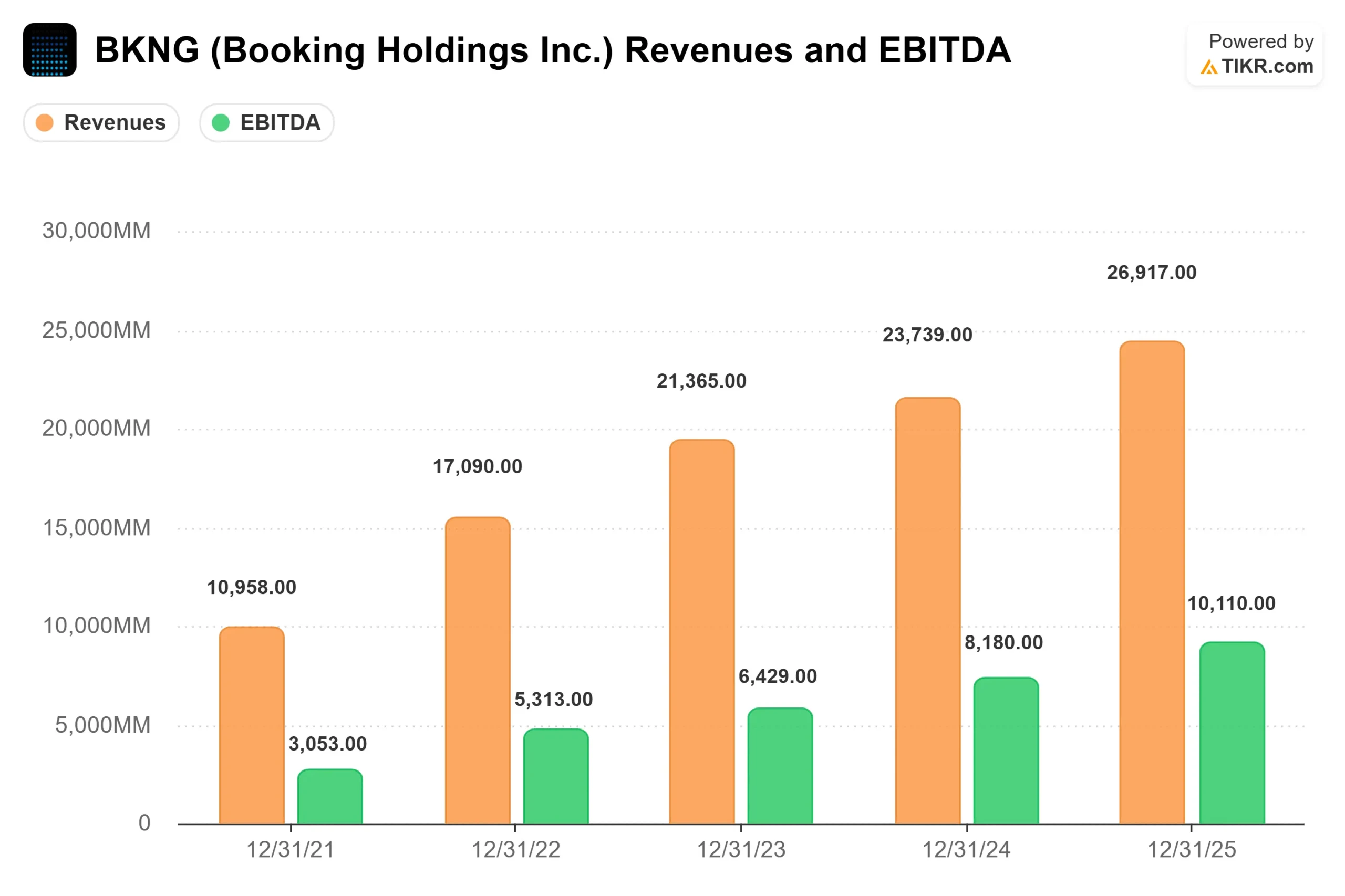

Booking delivered Q1 2026 revenue of $5.53 billion, up 16% year over year. Adjusted EBITDA of $1.29 billion beat consensus by 3.47%, and adjusted EPS of $1.14 topped the $1.08 estimate by 5.67%, per TIKR’s Beats & Misses data. The company booked 338 million room nights in the quarter, growing 6% year over year.

The cleaner read on the business comes from stripping out the conflict. CFO Ewout Steenbergen said on the Q1 2026 earnings call that the Middle East situation clipped room night growth by approximately 2 percentage points, and that without it, room nights would have grown approximately 8%, above the high end of guidance.

The headline most investors missed was U.S. growth. CEO Glenn Fogel confirmed that U.S. room night growth reached the low teens in Q1, “driven primarily by strong domestic demand,” for the fourth consecutive quarter of acceleration. That strength extended across flights, cars, and packages, not just hotels. Booking is gaining share in its most underpenetrated major market, and doing it across every vertical.

Connected Trip transactions, meaning bookings that include more than one travel category, such as a hotel and a flight together, grew in the high-teens range in Q1. That is approximately three times faster than Booking.com’s total transaction growth. These multi-vertical travelers return more frequently, which is a compounding retention dynamic that improves platform economics over time.

See historical and forward estimates for Booking Holdings stock (It’s free!) >>>

The Headwinds Are Real, But Contained

The guidance cut is what sent shares lower despite the beat. Management guided Q2 2026 room night growth of just 2% to 4%, with gross bookings, revenue, and adjusted EBITDA each expected to grow 4% to 6%. Steenbergen estimated approximately 3 percentage points of headwind from the Middle East conflict in Q2, up from 2 percentage points in Q1, because the conflict now spans the full quarter.

The full-year plan assumes the conflict’s impact persists through June, followed by a second-half recovery. The exposure is real but specific: approximately 7% of Booking’s 2025 global room nights involved the Middle East as a destination or transit hub, per Steenbergen’s call remarks. Outside those corridors, demand held up well in Q1. Intra-European travel was up high single digits and intra-Asia travel was up low double digits, consistent with Q4 2025 trends.

One more layer of uncertainty: Italy’s competition authority, the AGCM, launched a formal investigation into Booking.com on April 22, 2026, examining whether its Preferred Partner and Preferred Partner Plus programs prioritize hotels paying higher commissions rather than those offering the best value. Booking.com confirmed it is cooperating. The company has resolved similar European regulatory inquiries before, but the investigation adds uncertainty heading into what is already a pressured year.

See how Booking Holdings performs against its peers in TIKR (It’s free!) >>>

Is the Discount Justified?

At 12.08x NTM EV/EBITDA and 15.80x NTM P/E, BKNG is trading near a multi-year valuation low. Consider what you get at that price: an LTM ROIC of 93.6%, an 87% gross margin, and an NTM free cash flow yield of 8.1%, all per TIKR data.

For context, Airbnb trades at 28.52x NTM P/E at 5.50x NTM EV/Revenue, and Expedia trades at 12.96x NTM P/E and 8.10x NTM EV/EBITDA. BKNG’s historically wide premium to Expedia has nearly collapsed despite structurally higher margins and a stronger direct booking mix. That compression looks like sentiment-driven repricing, not a fundamental verdict on the business.

Management is voting with its capital. The $3.6 billion Q1 buyback, the largest single quarter of repurchases in Booking’s history, signals exactly what the board thinks of $169.63. Fogel noted on the call that since 2014 the company has reduced its share count by over 40% at an average repurchase price of $93 per share. The current buyback pace is not the behavior of a leadership team worried about the business.

The AI narrative also cuts in Booking’s favor more than the stock price suggests. Fogel confirmed active partnerships with OpenAI, Google, Anthropic, and Amazon on the call.

At Agoda, AI-assisted automation drove a double-digit year-over-year reduction in customer service cost per booking in Q1. At Priceline, the company’s AI travel assistant Penny is showing early conversion uplift in limited testing. The fear that AI chatbots disintermediate online travel agencies drove part of BKNG’s 2026 selloff. The execution on the ground suggests a different outcome.

The honest counterargument: near-term visibility is genuinely limited. Piper Sandler analyst Thomas Champion, maintaining a Neutral rating after Q1 results, described BKNG as “a great business and long-term EPS compounder of 15%+, but near-term visibility is limited given an uncertain timeline for conflict resolution.” Goldman Sachs, also Neutral, noted investor debates will stay centered on when Middle East travel patterns normalize. Both are fair points for anyone with a shorter time horizon.

TIKR Advanced Model Analysis

- Current Price: $169.63

- Target Price (Mid): ~$342

- Potential Total Return: ~102%

- Annualized IRR: ~16% / year

See analysts’ growth forecasts and price targets for Booking Holdings stock (It’s free!) >>>

The mid case uses a forward revenue CAGR of around 8%, driven by continued U.S. market share gains and structural growth in Asia-Pacific, and a net income margin rising toward around 31% by 12/31/30. The margin driver is the transformation program, which targets $500 million to $550 million in in-year savings for 2026 and compounds into EBITDA expansion over the forecast period.

The upside path: the conflict resolves on the assumed June timeline, second-half room night growth rebounds to high single digits, and U.S. momentum continues. At 12x forward EBITDA with those fundamentals, the current price looks like a significant misvaluation.

The downside path: the disruption extends past June, broader macro pressure weighs on discretionary travel, or the Italy investigation expands into a wider European action on Booking.com’s commission model. In that scenario, the stock tests the 52-week low of $150.62.

Conclusion

The number to watch at Q2 2026 earnings, scheduled for July 30, 2026, is room night growth guidance for the second half. If management signals high-single-digit or better room night growth resuming in Q3, the recovery thesis holds, and the valuation gap closes. If the second-half recovery is pushed out, the full-year guide falls apart. At $169.63 and 12x forward EBITDA, the market is treating a temporary, geographically specific disruption as if it were a structural break in the business. The Q1 transcript says otherwise.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Booking Holdings?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Booking Holdings, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Booking Holdings alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Booking Holdings on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!