Key Takeaways:

- Pfizer is a global pharmaceutical company rebuilding growth after a post-COVID revenue decline through major acquisitions and pipeline wins, while Amgen is a mature biotech growing steadily with a diversified biologics portfolio and an emerging obesity drug catalyst.

- Analysts expect both companies to sustain operating margins near 30% to 35%, with Amgen generating $8.1 billion in free cash flow in 2025 and growing revenues to $35.1 billion, while Pfizer faces an estimated annual revenue contraction of around 3% over the next two years.

- Based on our valuation assumptions, Amgen stock could rise from around $330 to around $397 per share by December 2028, while Pfizer stock could reach around $30 per share from $26 today, reflecting meaningful but modest upside for both.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

What’s Happening?

Pfizer (PFE) is one of the world’s largest pharmaceutical companies. It discovers, develops, and sells medicines across oncology, cardiovascular, and infectious disease. Key products include Eliquis, Ibrance, Vyndaqel, and Paxlovid, covering blood clots, cancer, and heart disease. But Pfizer’s revenue dropped after COVID demand faded, so the company is rebuilding through acquisitions and pipeline progress.

Pfizer paid around $43 billion to acquire Seagen in 2023, adding a focused oncology business. The FDA also approved Veppanu in May 2026, a breast cancer drug developed in collaboration with Arvinas.

Amgen (AMGN), by contrast, is a leading biotech focused on inflammation, oncology, bone health, and cardiovascular disease. And Amgen has been broadening its weight-loss drug development, adding a key new growth catalyst beyond its core biologics portfolio.

Both companies operate in the same healthcare sector, but they tell very different stories. Pfizer is larger and more globally diversified, but still navigating a complex revenue reset. Amgen is smaller but more focused, with rising revenues and a stronger margin trajectory.

Here’s why the margin and valuation comparison make this matchup genuinely interesting.

Estimate a company’s fair value instantly (Free with TIKR) >>>

The Margin Recovery Story Is Very Different for Both Companies

Amgen’s revenue grew from $24.3 billion in 2021 to $35.1 billion by 2025. That growth was driven largely by the Horizon Therapeutics acquisition and strong organic product performance. But operating margins declined from around 38% in 2022 to around 29% in 2024, reflecting higher integration costs. By 2025, margins recovered to around 31.5%, showing the business is stabilizing.

Amgen also generated $8.1 billion in free cash flow in 2025. That dipped from $10.4 billion in 2024, as higher capital spending weighed on results. The company invested heavily in its Horizon integration and US manufacturing expansion. Still, Amgen’s free cash flow remains robust and well above its annual dividend cost.

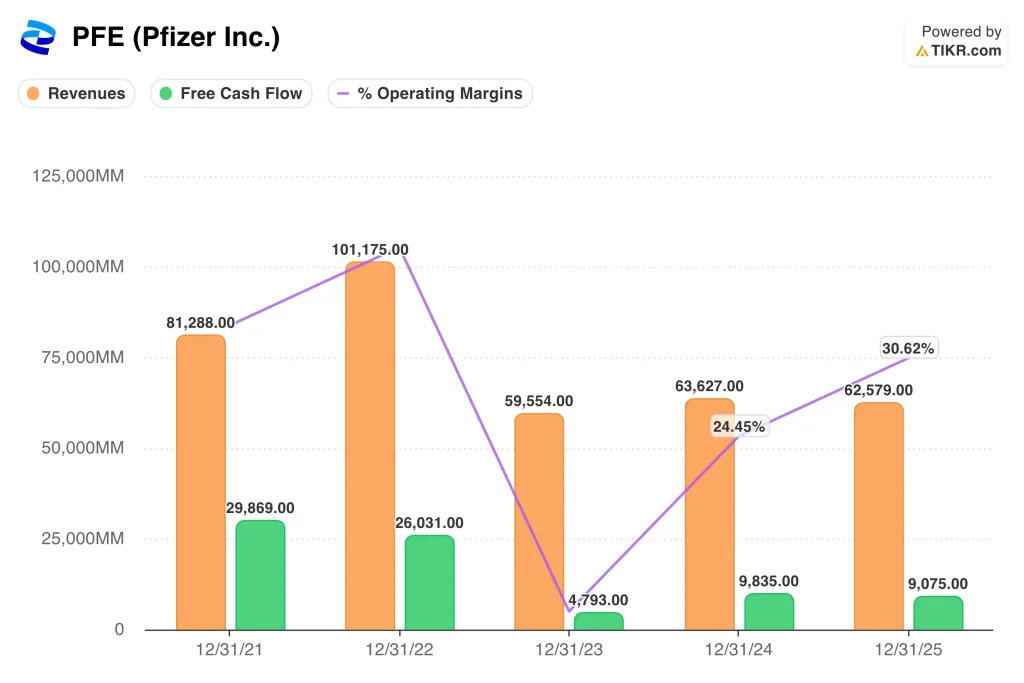

Pfizer’s revenue trajectory is more dramatic and harder to interpret. Revenue peaked at $101.2 billion in 2022 because of massive COVID vaccine and treatment demand. But it fell sharply to $59.6 billion in 2023 as COVID products lost their momentum. Since then, revenues have partially stabilized at around $62.6 billion in 2025.

Pfizer’s operating margin also collapsed alongside revenue, falling to very low levels in 2023. By 2025, margins recovered to around 30.6%, close to Amgen’s current level. Free cash flow recovered too, rising from $4.8 billion in 2023 to $9.1 billion in 2025. So Pfizer is showing real margin recovery, but sustaining it depends on pipeline execution.

See what analysts think about Amgen and Pfizer stock right now (Free with TIKR) >>>

Pfizer Trades at a Deep Discount While Amgen Commands a Premium

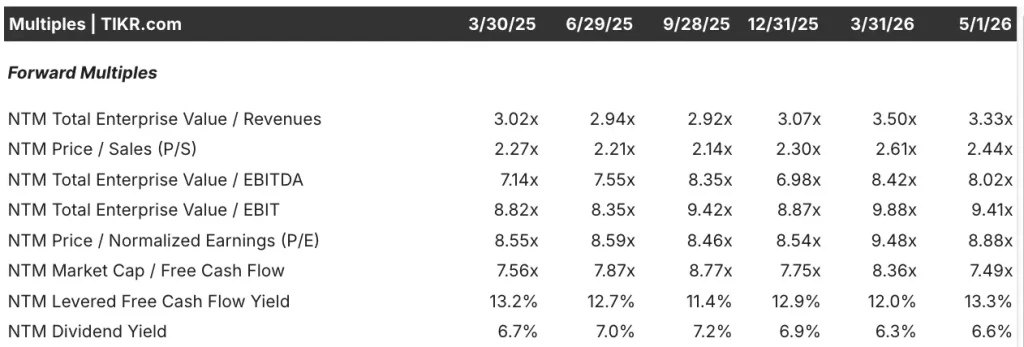

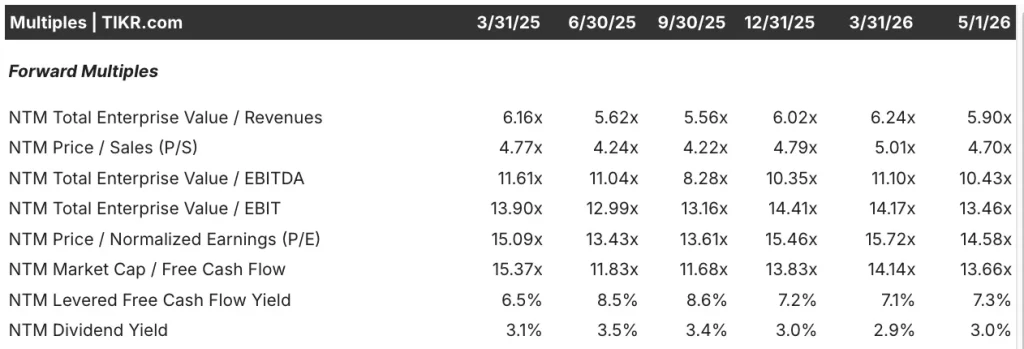

Forward valuation multiples reveal a significant gap between these two stocks. Pfizer trades at a forward price to earnings ratio of around 9x. Amgen trades at around 15x forward earnings, so investors pay a meaningfully higher premium. That gap reflects Pfizer’s ongoing revenue uncertainty versus Amgen’s more stable growth profile.

Enterprise value to EBITDA is another key valuation measure used widely in healthcare. EBITDA stands for earnings before interest, taxes, depreciation, and amortization, and it reflects core business profitability. Pfizer trades at around 8x on this measure, while Amgen trades at around 10x. So Pfizer again looks cheaper, and its lower multiple reflects the market’s caution around its recovery.

Free cash flow yield is an important metric for investors who prioritize dividends. Pfizer’s levered free cash flow yield is around 13%, compared to around 7% for Amgen. That means Pfizer generates more cash relative to its market cap today. And Pfizer’s 6.6% dividend yield is notably higher than Amgen’s 3.0% yield.

Amgen’s premium multiple is not surprising given its steadier revenue and margin trajectory. But Pfizer’s discount reflects genuine business uncertainty around its ongoing revenue rebuild. If Pfizer’s pipeline delivers on analyst expectations, that discount could narrow quickly. Both valuations look reasonable given where each company sits in its current cycle.

See analysts’ full growth forecasts and estimates for Amgen and Pfizer stock (It’s free) >>>

Amgen’s Upside Looks Stronger, but Pfizer’s Income Helps Bridge the Gap

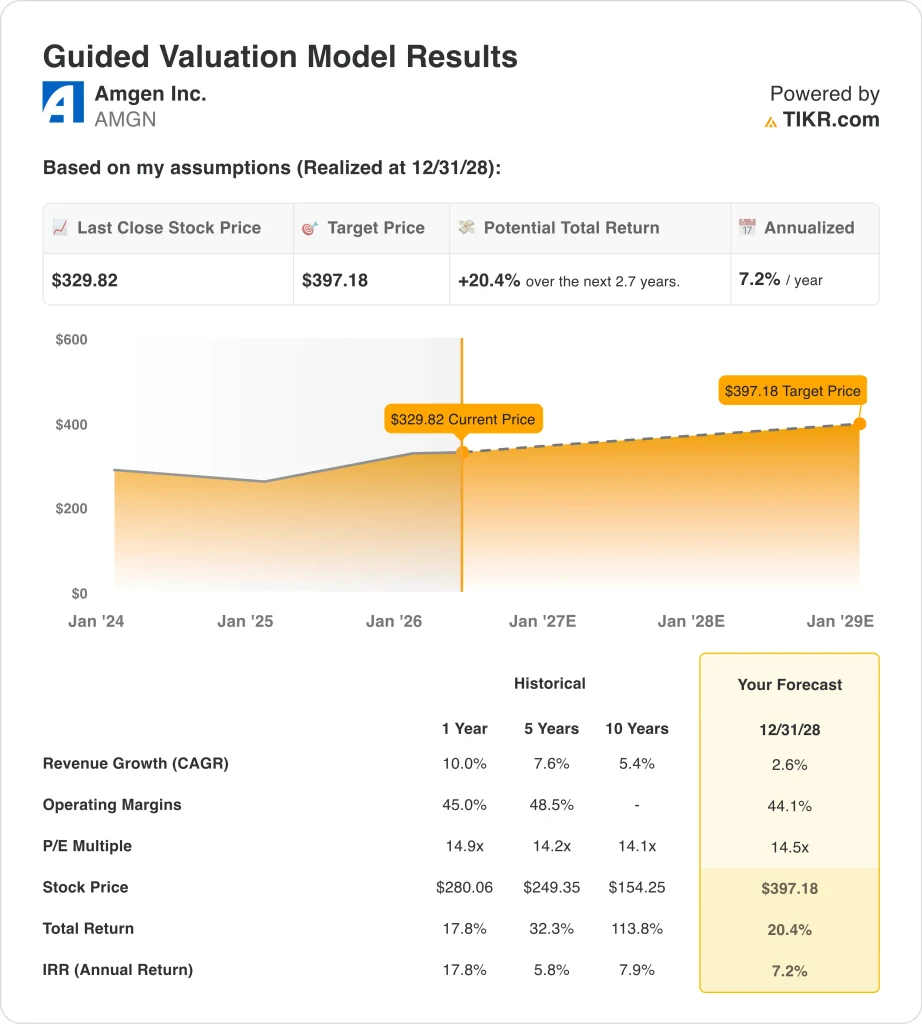

We analyzed the upside potential for Amgen stock based on its growing biologics portfolio and advancing obesity drug pipeline.

Based on estimates of 2.6% annual revenue growth, 44.1% operating margins, and a normalized P/E multiple of 14.5x, the model projects Amgen stock could rise from $330 to around $397 per share.

That would be a 20.4% total return, or a 7.2% annualized return over the next 2.7 years.

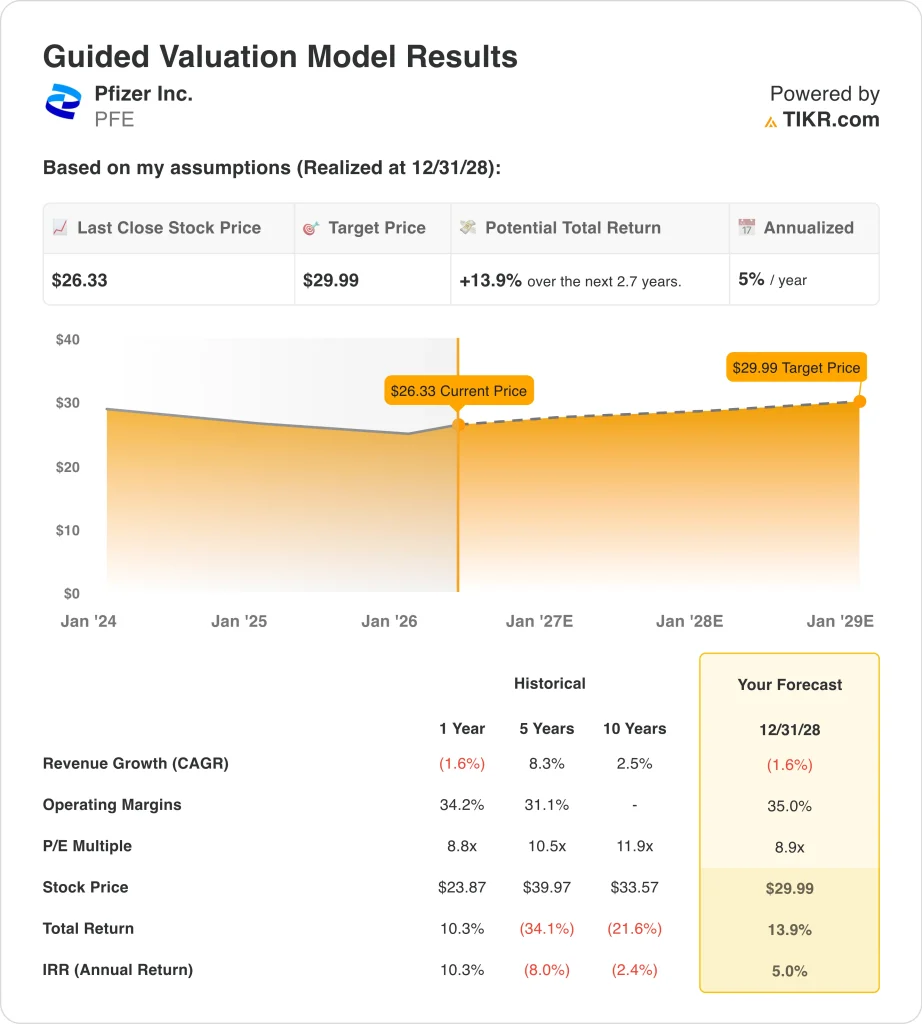

We analyzed the upside potential for Pfizer stock based on its pipeline recovery and expected margin stabilization.

Based on estimates of a 1.6% annual revenue decline, 35.0% operating margins, and a normalized P/E multiple of 8.9x, the model projects Pfizer stock could rise from $26 to around $30 per share.

That would be a 13.9% total return, or a 5.0% annualized return over the next 2.7 years.

Based on analysts’ consensus estimates, we see a meaningful gap in projected returns between the two stocks. Amgen projects a 7.2% annual return, which sits above the threshold most investors consider meaningful.

Pfizer’s 5.0% annualized return is near the lower end of what typically draws serious investor interest. So the models suggest Amgen offers the stronger return case, though both outcomes depend heavily on pipeline delivery.

Build your own Valuation Model to value any stock (It’s free!) >>>

Which One Do You Actually Buy?

Both Pfizer and Amgen are reliable dividend payers, but they serve very different investor needs. Pfizer offers a 6.6% dividend yield, so investors who prioritize income get meaningfully more from this stock today. Amgen carries a 3.0% yield, but its revenue trajectory is clearly moving upward. And Amgen’s $8.1 billion in free cash flow supports continued dividend growth ahead.

Pfizer’s pipeline has real momentum, and recent data shows meaningful progress on multiple fronts. The FDA approved Veppanu for breast cancer in early May 2026, a drug developed with Arvinas. Also, the Phase 3 ELREXFIO trial met its primary endpoint for multiple myeloma in late April 2026. And Pfizer’s GLP-1 obesity drug delivered positive Phase 2B results, opening the door to a large new market.

Amgen’s Q1 2026 revenue rose 6% to $8.6 billion, confirming the upward growth trend. The company committed nearly $2 billion in US manufacturing investment over the past year. If Pfizer’s pipeline delivers, the stock could move meaningfully higher from today’s discounted levels. Going forward, Pfizer suits income seekers who can wait for the recovery, while Amgen suits investors who prefer steadier growth and stable margins.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Should You Invest in Amgen or Pfizer?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up AMGN or VST, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track AMGN or VST alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Amgen and Pfizer stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!