Key Stats for RTX Stock

- Past week’s performance: Consolidating

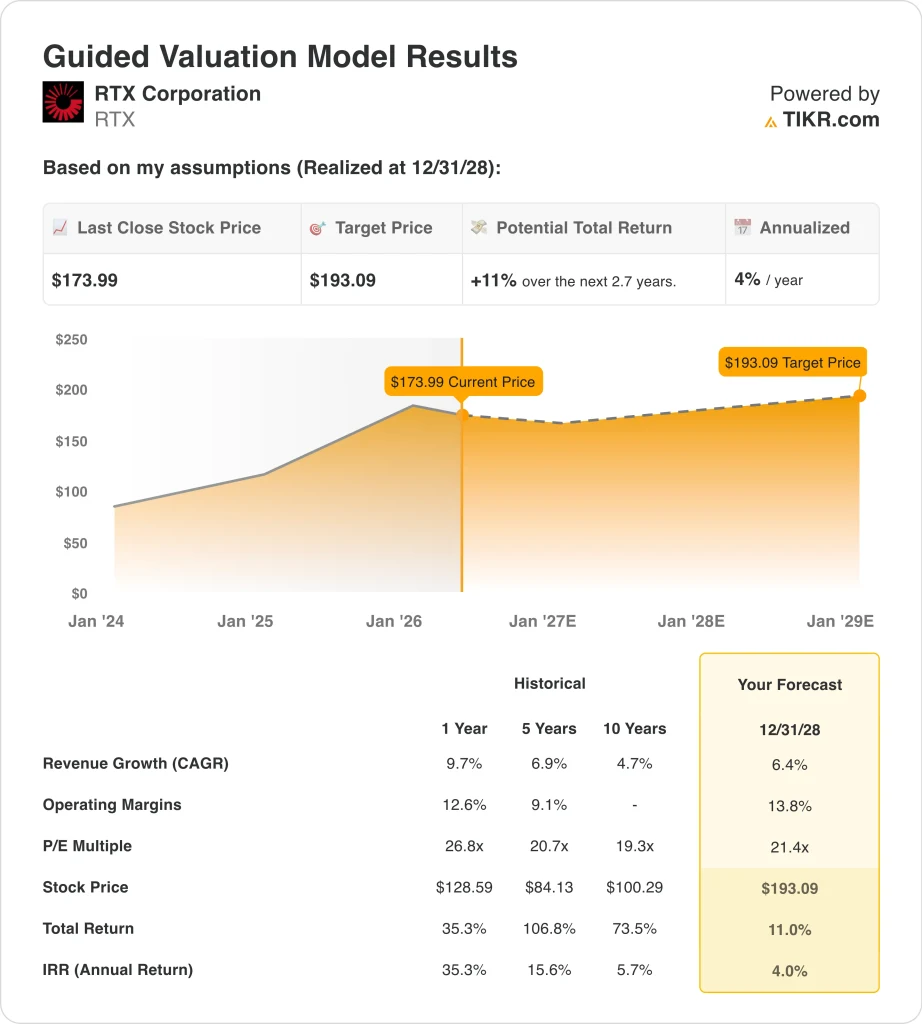

- 52-week range: $126 to $215

- Valuation model target price: $193

- Implied upside: 11% over 2.7 years

Value your favorite stocks like RTX with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

RTX Corporation (RTX), formerly known as Raytheon Technologies, researches, develops, and manufactures advanced technology products for the aerospace and defense industry. The company operates three major business segments: Collins Aerospace, Pratt and Whitney, and Raytheon.

Shares gained about 0.4% over the past week, trading near $174 after a standout Q1 2026 earnings report. RTX reported adjusted EPS of $1.78 per share, well above the Wall Street estimate of $1.52. That result was driven by strong demand across all three segments and especially by Raytheon, which continues to benefit from rising global defense budgets.

Pratt & Whitney secured the most significant Q1 contract win: a $6.6 billion F135 engine production award for lots 18 and 19 of the F-35 fighter jet engine program. As the world’s most widely deployed fifth-generation fighter aircraft, the F-35 deepens RTX’s long-term revenue visibility.

RTX also received a DARPA contract to develop kilometer-range detection technology, known informally as “X-ray vision,” reflecting the company’s expansion beyond traditional weapons into advanced sensing systems. Raytheon separately delivered its second missile-warning sensor to the U.S. Space Force’s Next Generation OPIR (Overhead Persistent Infrared) satellite program.

RTX raised its quarterly dividend to $0.73 per share, announced on May 1, 2026, up from the prior $0.68 rate. That increase signals management’s confidence in continued free cash flow generation.

The current payout ratio is around 50%, so there is room for further increases if earnings continue growing. Pratt and Whitney also invested more than $100 million to expand its GTF MRO sites in the U.S. and opened a new manufacturing facility in Morocco in April 2026.

Going forward, RTX stock will be watched for further defense contract wins, Pratt and Whitney engine production rates, and any guidance update at the next quarterly call.

See analysts’ growth forecasts and price targets for RTX (It’s free) >>>

Is RTX Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 6.4%

- Operating Margins: 13.8%

- Exit P/E Multiple: 21.4x

Based on these inputs, the model estimates a target price of $193, implying 11% total upside from the current share price and a 4% annualized return over the next 2.7 years.

A 4% annualized return is below what most long-term equity investors require. The Street consensus target of $216 is more optimistic, implying roughly 24% upside. The difference reflects how aggressively RTX can expand margins and whether the current defense demand cycle sustains through 2028.

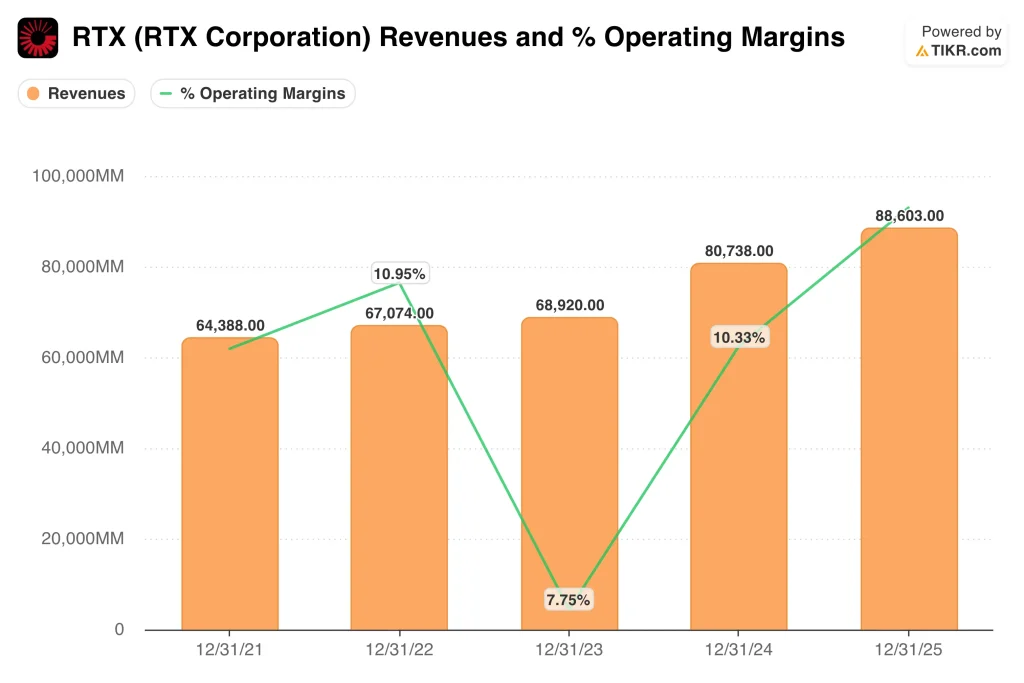

Revenue growth of 6.4% per year is consistent with the company’s recent trend. RTX grew revenue by about 9.7% over the past year and is expected to maintain a solid trajectory as global defense spending continues to rise.

Operating margins of 13.8% represent a modest improvement from the current 12% LTM EBIT margin. Achieving that improvement requires continued operational efficiency in the Collins Aerospace and Raytheon segments, where supply chain investments have been ongoing for the past two years.

The exit P/E of 21.4 times is well below RTX’s current trailing P/E of roughly 32.6 times. So the model is actually assuming meaningful multiple compression by 2028, which is what produces the low implied annual return.

If RTX maintains its current valuation multiple rather than compressing, the total return would be considerably higher. But that higher return scenario depends on the defense cycle not peaking and margins continuing to expand through the forecast period. The stock suits investors who value dividend income and defense sector exposure alongside capital appreciation.

What’s Driving RTX Stock Going Forward?

Global defense spending is the biggest structural tailwind for RTX. NATO countries continue increasing budgets in response to ongoing geopolitical tensions, and the Middle East market is actively buying advanced defense systems.

The U.S. government recently approved $8.6 billion in military sales to Middle East allies, bypassing the standard congressional review process. That approval signals urgency in the procurement cycle and benefits Raytheon’s portfolio of Patriot air defense systems, advanced missiles, and surveillance platforms.

Pratt and Whitney’s F135 engine production contract win is a multiyear revenue anchor. The $6.6 billion contract covers production lots 18 and 19 of the F-35 program, and the program is expected to continue for decades as additional allied nations put F-35s into service.

Pratt and Whitney also invested more than $100 million to expand GTF MRO sites in the United States. Those capacity investments position the company to handle growing service demand as the global GTF engine installed base expands.

Collins Aerospace continues to grow its commercial aviation footprint. Thai Airways activated advanced connectivity services for its A321neo fleet through Collins in February 2026, and Vietjet selected Pratt and Whitney engines for 44 additional A320neo family aircraft.

Commercial aviation is adding new aircraft at a healthy pace, and that sustains demand for Collins’s avionics, communications, and cabin systems. Commercial exposure balances the defense segment and reduces RTX’s dependence on government budget cycles alone.

The most important risk to monitor is the stock’s current valuation. RTX is up 35.3% over the past year and trades at roughly 32 times trailing earnings. If defense contract wins slow or Pratt and Whitney faces new GTF engine reliability issues, the stock could give back recent gains relatively quickly.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in RTX?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up RTX, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track RTX alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze RTX stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!