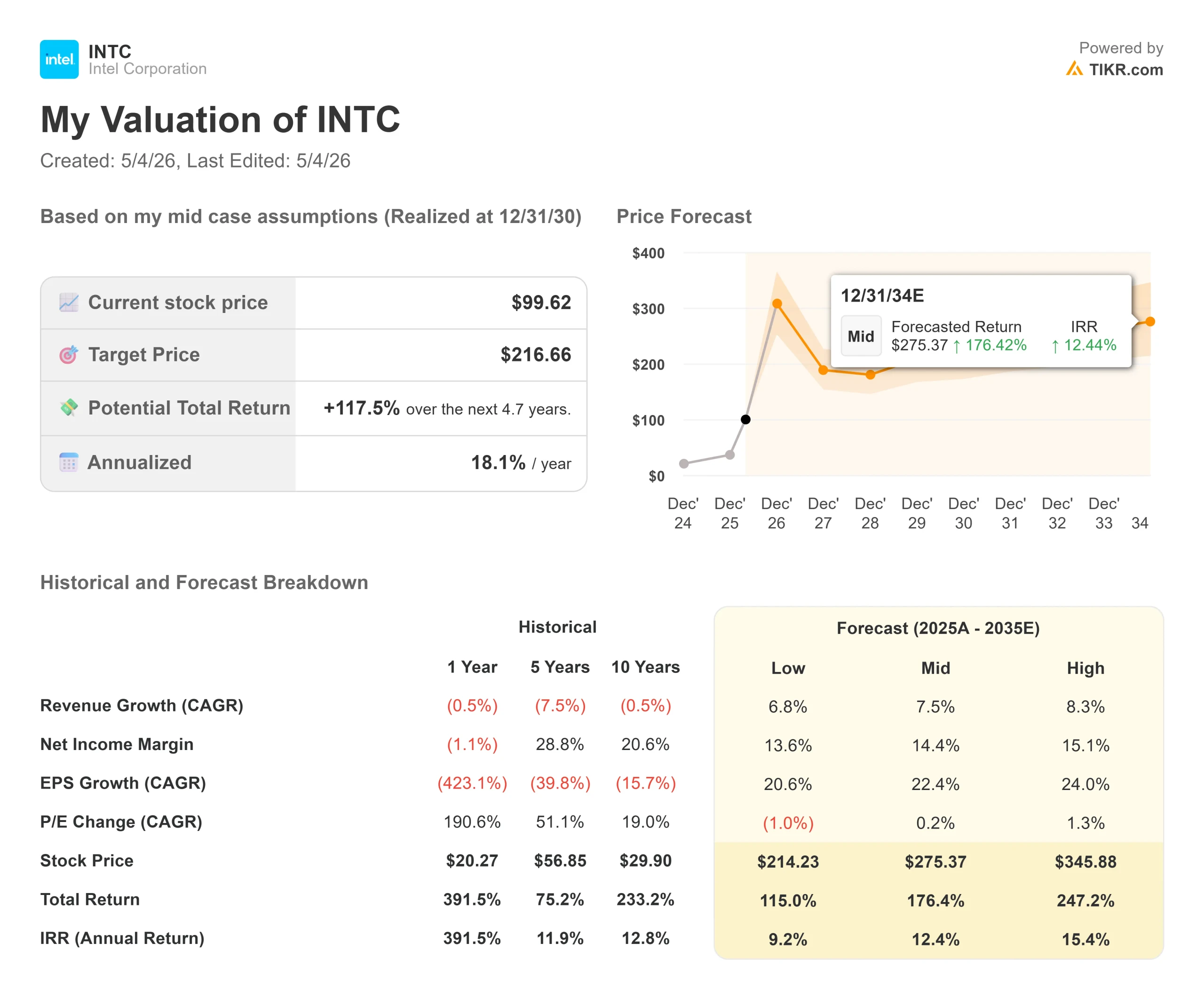

Key Stats for Intel Stock

- Current Price: $99.62

- Target Price (Mid): ~$217

- Street Target: ~$78

- Potential Total Return: ~118%

- Annualized IRR: ~18% / year

- Earnings Reaction: +23.60% (April 24, 2026)

- Max Drawdown: 24.17% (March 30, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

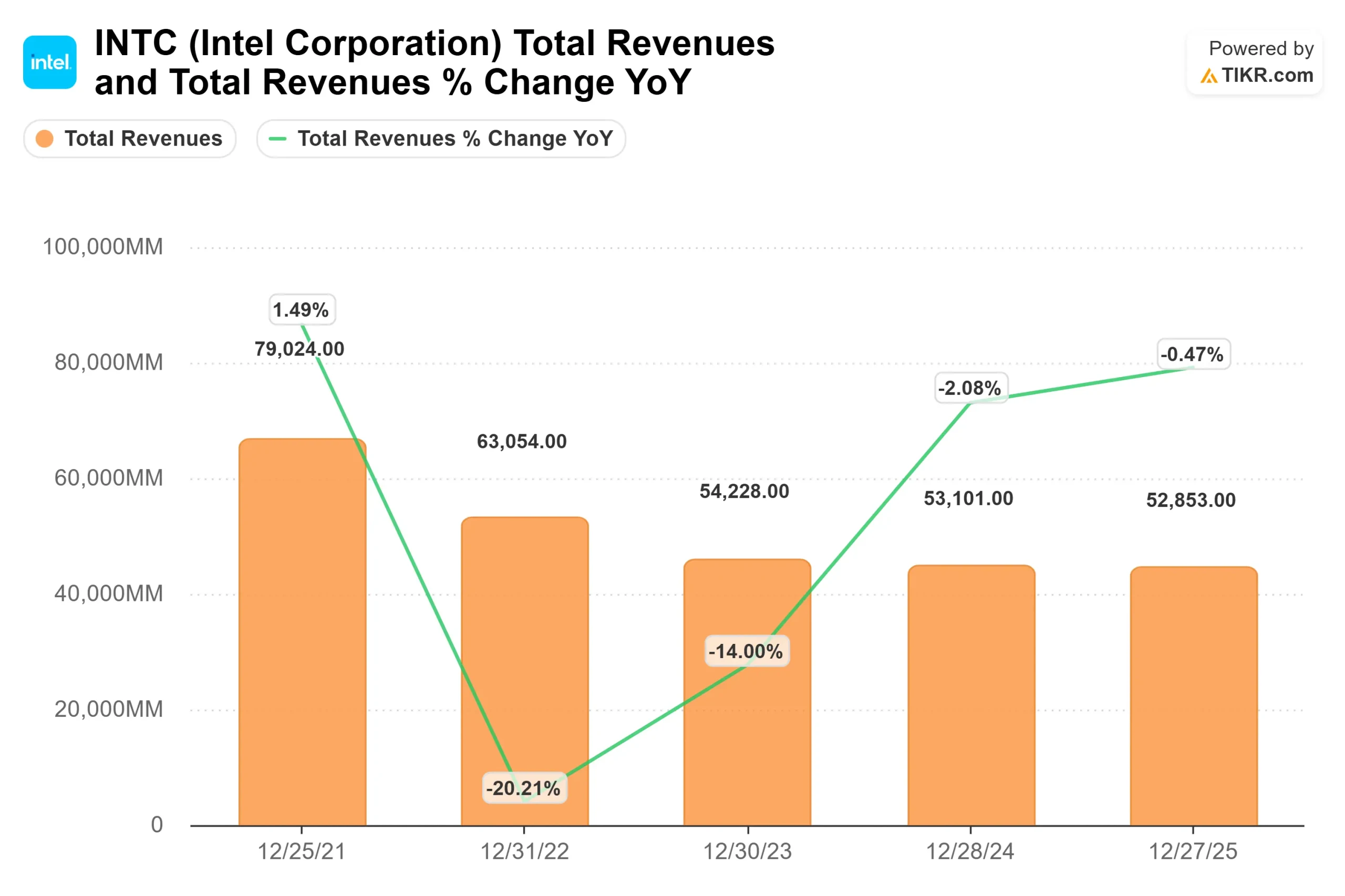

Intel (INTC) surged 23.60% on April 24, 2026, its biggest single-day gain in nearly four decades, after a Q1 report that reframed what kind of company Intel is becoming. Bulls are pointing to six consecutive quarters above expectations and a data center business growing 22% year-over-year. Bears, anchored by a Street consensus target of around $78 that the stock has already blown past, argue it now trades at around 96x forward earnings on a business still posting GAAP losses. The real question: was the 24% surge rational, or has the stock run ahead of the fundamentals?

Intel reported Q1 2026 revenue of $13.6 billion, $1.4 billion above the midpoint of its own guidance and well ahead of the Wall Street consensus of approximately $12.36 billion. Non-GAAP EPS landed at $0.29 against a consensus of just $0.01. CFO David Zinsner attributed the beat to higher volume, improved product mix, pricing actions, and better-than-expected yields on Intel’s 18A process node (its most advanced chip manufacturing technology). Q2 guidance of $13.8 to $14.8 billion also topped the $13.07 billion the Street expected.

The CPU Is Back at the Center of AI

Intel’s combined AI-driven businesses now represent 60% of total revenue and grew 40% year-over-year, per CFO Zinsner on the Q1 call. The Data Center and AI segment (DCAI) generated $5.1 billion in Q1, up 22% year-over-year.

The specific insight investors are still absorbing: the ratio of CPUs to GPUs in AI deployments is narrowing fast. “The ratio of CPU to GPU used to be 1 to 8, and now it’s 1 to 4,” CEO Lip-Bu Tan said on the Q1 2026 earnings call, adding that the direction of travel is toward parity or better. If that shift continues, incremental server CPU demand at AI infrastructure scale is substantially larger than current consensus models assume.

Tan described the CPU as “the orchestration layer and critical control plane for the entire AI stack.” As workloads move from foundational training (GPU-heavy) to inference and then agentic AI (where systems handle tasks autonomously and coordinate multiple processes in parallel), compute architectures shift toward CPUs. That shift is now showing up in order patterns and multi-year contracts, not just in management commentary.

See historical and forward estimates for Intel stock (It’s free!) >>>

Google, Long-Term Agreements, and the ASIC Business

Intel signed multiple long-term agreements (LTAs, multi-year volume-and-pricing contracts with large customers) in Q1, with Google as the named example. CFO Zinsner described the typical structure as “somewhere between 3 and 5 years” with volume and pricing locked in on both sides. Google’s deal covers Xeon processors and custom silicon, making it both a CPU customer and an ASIC partner.

These agreements signal more than revenue visibility. A hyperscaler committing to a multi-year Xeon contract is making a structural bet on x86’s continued relevance inside AI infrastructure. Intel also confirmed that Xeon was selected as the host CPU for NVIDIA’s DGX Rubin NVL8 systems, meaning Intel’s chips are paired with NVIDIA’s most advanced AI compute platforms.

The ASIC business (purpose-built silicon optimized for specific customer workloads) embedded within DCAI more than doubled year-over-year in Q1 and is already running at a revenue rate above $1 billion annually, according to Zinsner. Tan called this a “fast-growing area” and said Intel’s combination of CPU design, advanced packaging, and foundry capabilities lets it build custom silicon in ways a pure-play fabless chipmaker cannot.

See how Intel performs against its peers in TIKR (It’s free!) >>>

The Foundry Wildcard: 18A, 14A, and Terafab

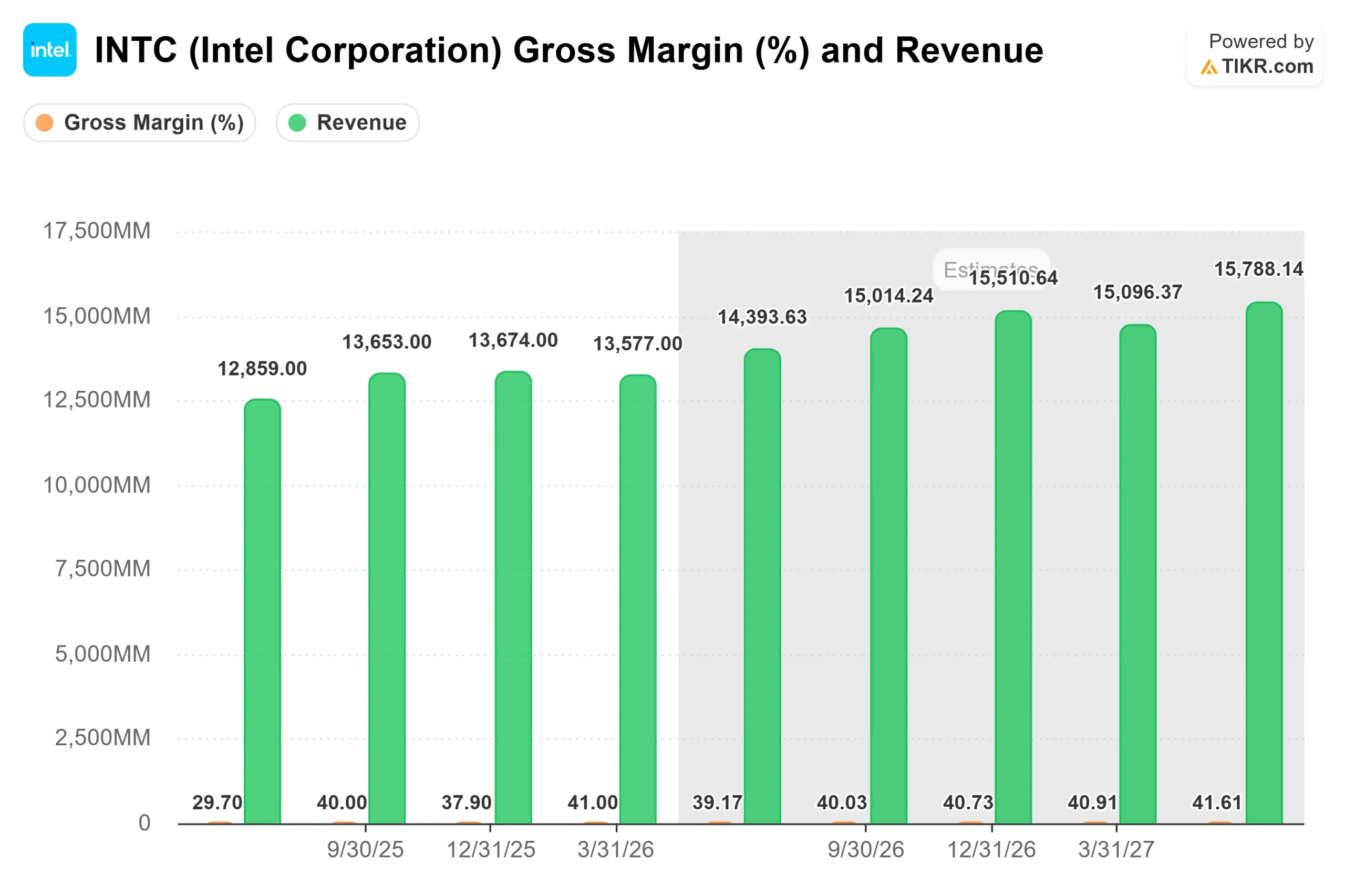

Intel Foundry reported Q1 revenue of $5.4 billion, up 20% sequentially, with an operating loss of $2.4 billion that improved $72 million quarter-over-quarter as yields across Intel 3, 4, and 18A improved. Zinsner confirmed 18A yields are tracking to hit year-end targets by mid-2026, roughly two quarters ahead of plan.

Intel 14A (the next-generation node after 18A, currently in customer evaluation) is outpacing 18A at a comparable stage of development. Design commitments from external customers are expected to begin in the second half of 2026. The partnership with Tesla, SpaceX, and xAI’s Terafab project, announced alongside these results, is the first major external signal that 14A is a production-credible target. Tan also noted Intel is routing more of its own product designs onto 14A, which improves fixed-cost absorption before external customers commit volume.

One honest caveat: external foundry revenue in Q1 was just $174 million against total foundry revenue of $5.4 billion. The foundry is still overwhelmingly internal. Bank of America analyst Vivek Arya reiterated his Underperform rating post-earnings, citing the absence of a confirmed major external wafer customer as the key risk. That concern is valid given how much of the long-term thesis depends on the external foundry becoming commercially significant.On peer valuation multiples, Intel’s NTM EV/EBITDA of 25.77x sits above TSMC’s 13.12x and near Broadcom’s 24.83x, but well below AMD’s 49.77x, per TIKR’s Competitors page. Intel’s premium over TSMC reflects the optionality of its product businesses. Its discount to AMD reflects AMD’s cleaner margins and more established AI momentum. Whether Intel closes that gap depends on foundry execution over the next several quarters.

TIKR Advanced Model Analysis

- Current Price: $99.62

- Target Price (Mid): ~$217

- Potential Total Return: ~118%

- Annualized IRR: ~18% / year

See analysts’ growth forecasts and price targets for Intel stock (It’s free!) >>>

The TIKR mid-case model targets approximately $217 by 12/31/30, implying around 118% total return and an annualized IRR of around 18%. The two primary revenue CAGR drivers are DCAI growth as CPU demand in AI infrastructure deepens, and Intel Foundry external revenue beginning to convert from backlog to recognized revenue as 14A customer commitments materialize. The margin driver is gross margin expansion as 18A and 14A yields improve and volumes absorb fixed costs, with the mid-case modeling net income margins recovering toward around 14% by 2030 from the current 3.6%.

The primary risk is gross margin pressure in the second half of 2026. Rising substrate, memory, and component costs could offset yield improvements, a headwind Zinsner flagged directly on the call. If external foundry customers delay commitments, the margin recovery timeline stretches, and the mid-case assumptions get harder to defend.

Conclusion

Watch non-GAAP gross margin when Intel reports Q2 results on July 23, 2026. Management guided around 39%, down from Q1’s 41%. If gross margin holds at or above 39% despite rising input costs, yield improvement, and pricing are working. If it slips below 37%, the margin recovery timeline shifts. Intel is no longer a question of whether the turnaround is real. It is now a question of pace and cost.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Intel?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Intel, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Intel alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!