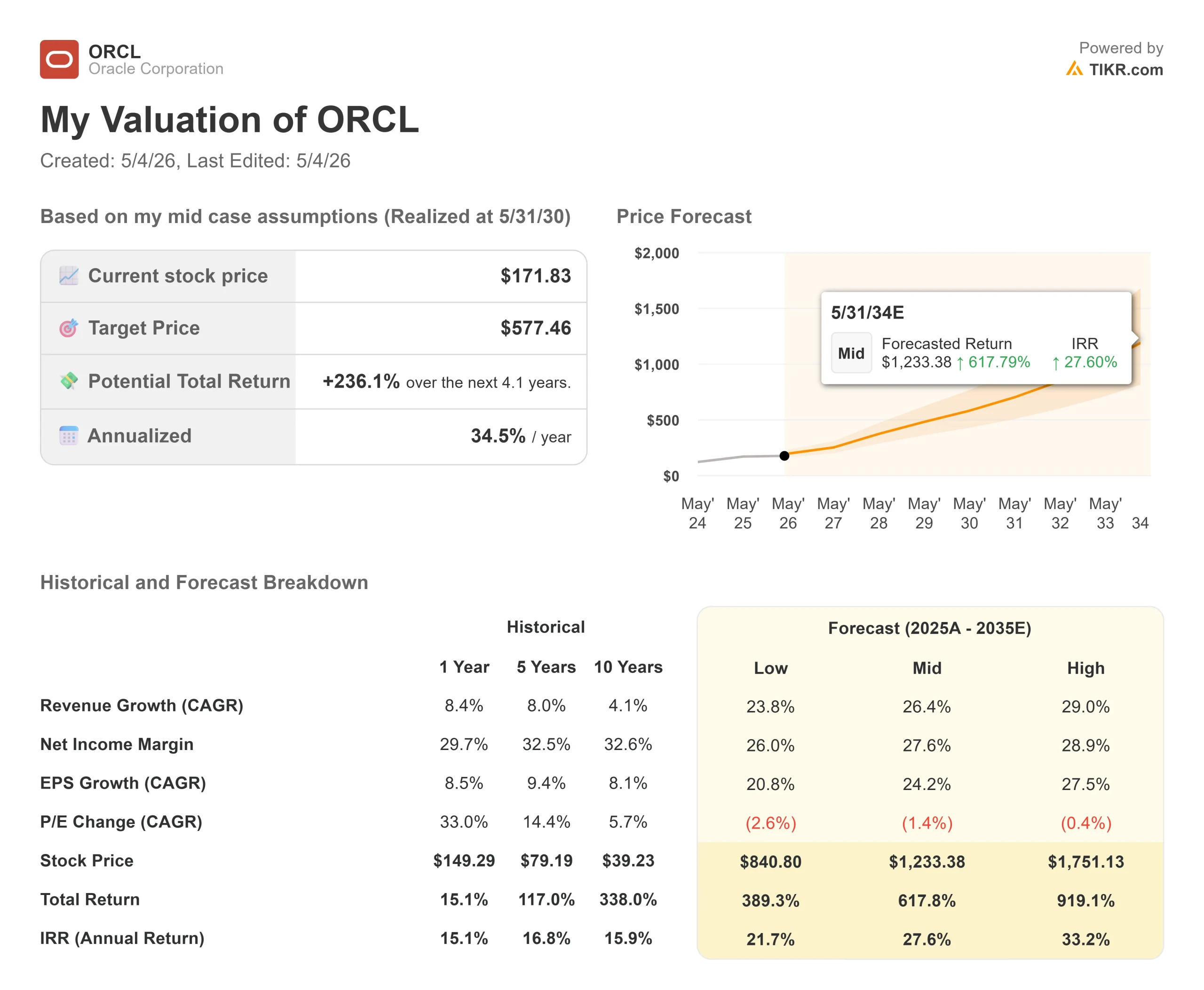

Key Stats for Oracle Stock

- Current Price: $171.83

- Target Price (Mid): ~$577

- Street Target: ~$243

- Potential Total Return: ~236%

- Annualized IRR: ~35% / year

- Earnings Reaction: +9.18% (3/10/26)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Oracle (ORCL) has been one of the most whipsawed large-cap tech stocks of 2026. Shares jumped 9.18% on March 10 after a landmark Q3 earnings beat, sold off when a Wall Street Journal report raised doubts about OpenAI’s internal revenue growth, then bounced over 6% on May 1 after Oracle announced a new CFO and an expanded fuel cell power partnership with Bloom Energy.

The stock sits roughly 50% below its September 2025 peak of $345.72. Bulls point to $553 billion in contracted backlog and 84% cloud infrastructure growth. Bears point to deeply negative free cash flow and $123 billion in net debt.

The market is still deciding which one matters more. Wedbush stepped in on April 24 with an Outperform rating and a $225 price target, calling Oracle “a foundational infrastructure provider for the AI revolution.” The TIKR model’s mid case, at ~$577 by May 31, 2030, suggests even that is undershooting.

What Wedbush Said and Why the Timing Mattered

Wedbush initiated coverage on April 24 with an Outperform rating and a $225 price target, arguing the market is fundamentally misinterpreting Oracle’s contract-backed investment cycle as speculative risk, and highlighting Oracle’s strategic partnerships with OpenAI and NVIDIA as central to its positioning as an AI infrastructure provider.

Per TIKR’s Street Targets data, the broader Wall Street picture as of May 1 is 28 Buys, 6 Outperforms, 8 Holds, 1 Underperform, and 1 Sell, with a mean price target of around $243. Wedbush’s $225 sits below that consensus, making it a measured call rather than an outlier.

Four days after initiating, Wedbush doubled down. On April 28, analyst Daniel Ives reiterated the Outperform rating and $225 target after the Wall Street Journal reported OpenAI had missed internal targets, calling the selloff a “way overreaction” and pointing to Oracle’s $553 billion backlog, which includes a $300 billion cloud contract with OpenAI spanning five years, as evidence that the demand is real and contracted.

See historical and forward estimates for Oracle stock (It’s free!) >>>

What the Q3 Transcript Reveals About the Business

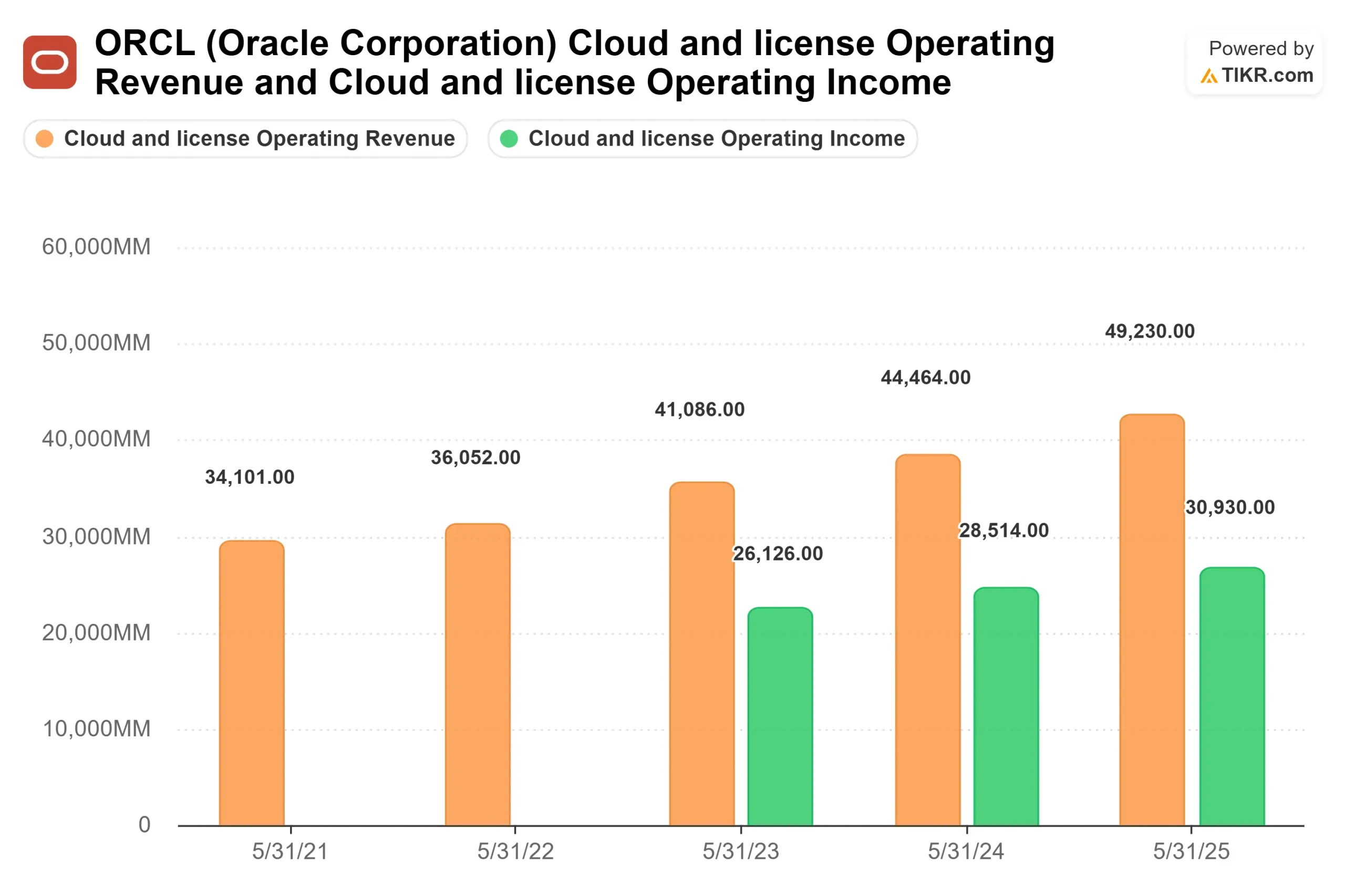

The Q3 FY2026 earnings call on March 10 was specific about the mechanics of how Oracle’s backlog converts into profit. CEO Clay Magouyrk reported that AI infrastructure gross margins on delivered capacity came in at 32%, above Oracle’s own 30% guidance floor. The multicloud database business, which he described as operating at 60% to 80% gross margins, is growing alongside infrastructure and lifting the overall margin mix as it scales.

Multicloud Database revenue grew 531% year-over-year in Q3. AWS regions scaled from 2 to 8 during the quarter, with a target of 22 by Q4 close. Oracle now has 33 live regions with Microsoft and 14 with Google. Each new region opens another distribution channel for Oracle’s highest-margin database services inside competing cloud environments.

On execution, Magouyrk noted that 90% of committed capacity was delivered on or ahead of schedule. Oracle delivered more than 400 megawatts to customers in Q3, rack output has increased 4x in the past year, and the time from rack delivery to recognized revenue has been cut by 60%. These are the metrics that determine how quickly $553 billion in contracted obligations becomes reported revenue.

CEO Mike Sicilia addressed the “SaaSapocalypse” debate directly on the call, whether AI coding tools would displace enterprise software: “We are the disruptor because we’re actually embedding the AI right into our applications, full stop.”

Cloud applications revenue reached an annualized run rate of $16.1 billion in Q3, with Fusion ERP up 14%, Fusion SCM and HCM each up 15%, and industry SaaS solutions for health care, banking, and retail combined growing 19% in constant currency. More than 2,000 customers went live on Oracle’s application suite during the quarter.

See how Oracle performs against its peers in TIKR (It’s free!) >>>

Valuation and the Real Risk

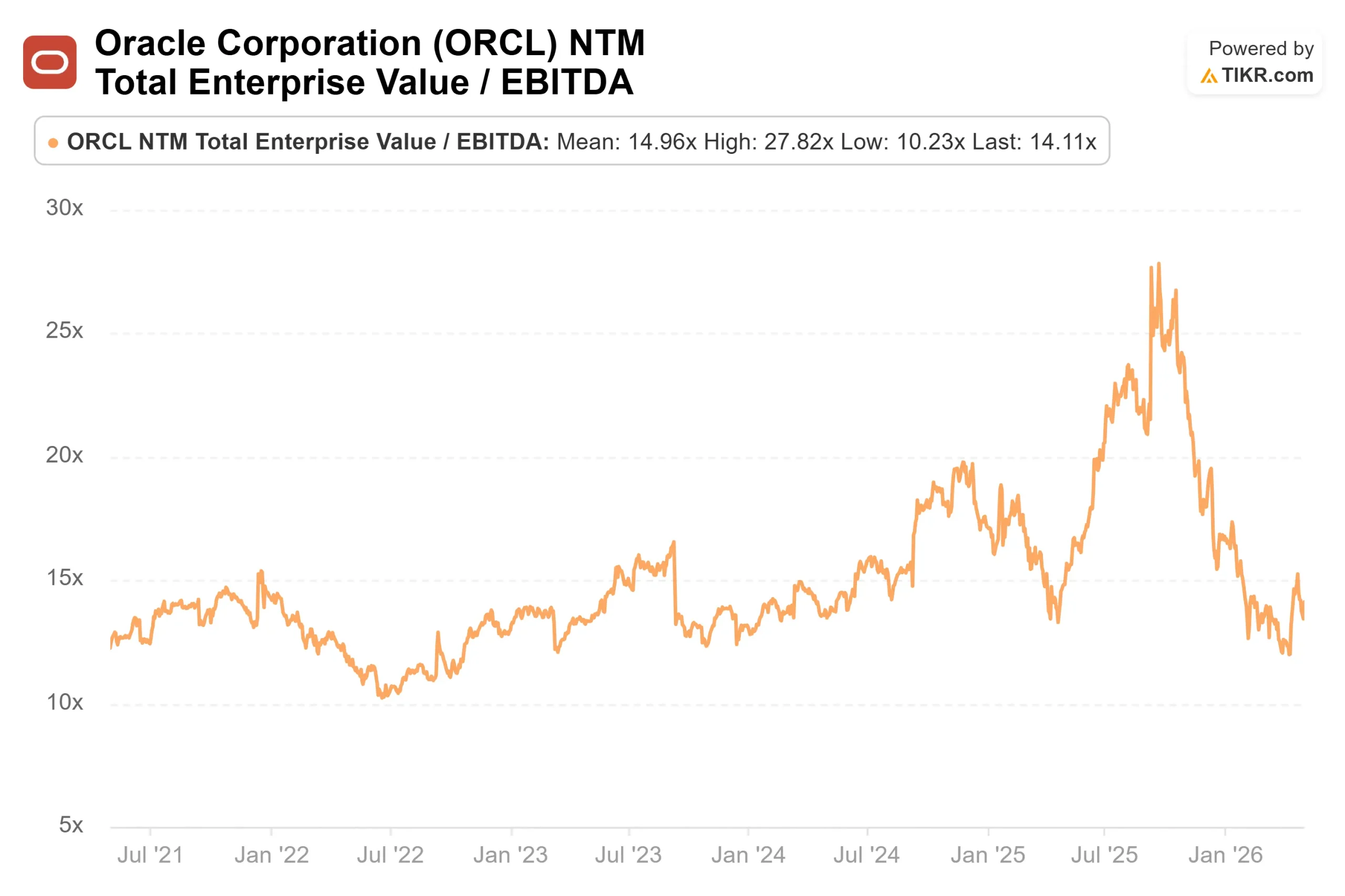

At $171.83, Oracle trades at 14.11x NTM EV/EBITDA and 22.83x NTM P/E, per TIKR. Microsoft, with a far slower cloud revenue growth rate, trades at 13.66x NTM EV/EBITDA and 22.45x NTM P/E. On a growth-adjusted basis, Oracle carries nearly the same forward earnings multiple as Microsoft, while posting 84% OCI revenue growth is the core of the valuation argument.

The balance sheet is the honest counterweight. TIKR data shows LTM net debt of $123 billion and a net debt/EBITDA ratio of 4.12x. Free cash flow remains negative through fiscal 2028 and turns positive only in fiscal 2029, per TIKR’s forward estimates. The partial offset, which Magouyrk explained on the call, is that customer prepayments and bring-your-own-hardware arrangements reduce Oracle’s net cash outlay below what the gross capex figure suggests. Oracle signed more than $29 billion in new contracts under those capital-light structures since the prior earnings call.

TIKR’s consensus estimates show revenue reaching around $88 billion in FY2027 and around $129 billion in FY2028. Oracle guided that total revenue will reach $90 billion in the fiscal year beginning in June, surpassing analyst projections at the time of the Q3 report. If those numbers land, the stock reprices against a fundamentally different earnings base than what the current multiple reflects.

TIKR Advanced Model Analysis

- Current Price: $171.83

- Target Price (Mid): ~$577

- Potential Total Return: ~236%

- Annualized IRR: ~35% / year

See analysts’ growth forecasts and price targets for Oracle stock (It’s free!) >>>

The TIKR mid-case model targets approximately $577 by May 31, 2030, implying around 236% total return and an annualized IRR of around 35% per year. The mid case assumes around 26% revenue CAGR, driven by two engines: OCI AI infrastructure scaling against the $553 billion contracted backlog, and multicloud database services compounding into all three major hyperscaler environments at the 60% to 80% gross margin level that management described. The margin driver is operating leverage as completed data center capacity reaches full utilization and construction overhead shrinks as a share of revenue.

The primary risk is backlog conversion. If OpenAI’s internal growth problems persist and draw down less capacity than contracted, or if Oracle’s delivery timeline slips, the revenue ramp delays, and the CAGR assumption weakens. That is the bear case. Wedbush’s counter, reiterated on April 28, is that OpenAI’s recent $122 billion funding round provides sufficient capital to fulfill compute commitments for at least three years, and that the broader $553 billion backlog across Meta, NVIDIA, and other customers provides enough diversification to contain single-customer risk.

At 14x forward EV/EBITDA against 84% infrastructure revenue growth, the TIKR mid-case of ~$577 implies the market has not yet priced in what Oracle has already contracted.

[GRAPH: TIKR Valuation Model Price Forecast Through 5/31/30]

Conclusion

Watch OCI infrastructure revenue growth and RPO additions at Oracle’s Q4 FY2026 earnings, expected June 8, 2026. If OCI growth holds at or above the 84% posted in Q3 and quarterly RPO additions remain above $29 billion, the case that Wedbush’s $225 understates what Oracle has already booked gets materially stronger. Oracle is trading at a legacy-software multiple, despite an AI infrastructure growth rate that the Street has not yet fully priced.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Oracle?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Oracle, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Oracle alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!