Key Stats for Toast Stock

- 52-Week Range: $24 to $50

- Current Price: $28

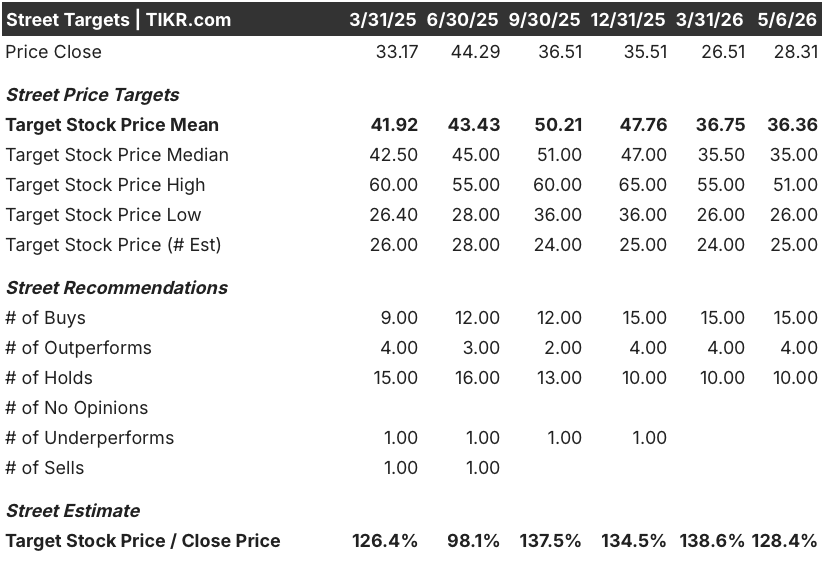

- Street Mean Target: $36

- Street High Target: $51

- Analyst Consensus: 15 Buys / 4 Outperforms / 10 Holds

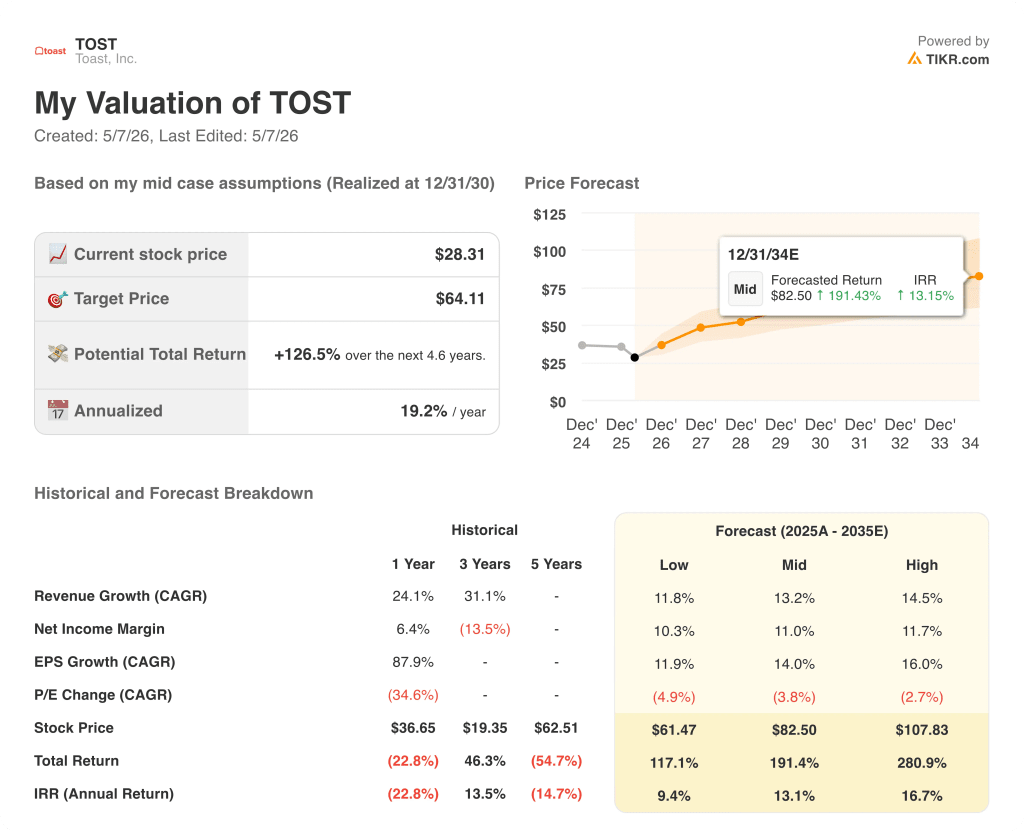

- TIKR Model Target (Dec. 2030): $64

What Happened?

Toast, Inc. (TOST) is the dominant cloud-based restaurant management platform in the U.S., powering everything from point-of-sale terminals and kitchen display systems to payroll, online ordering, loyalty, and now AI-driven operational tools across more than 164,000 live restaurant and retail locations.

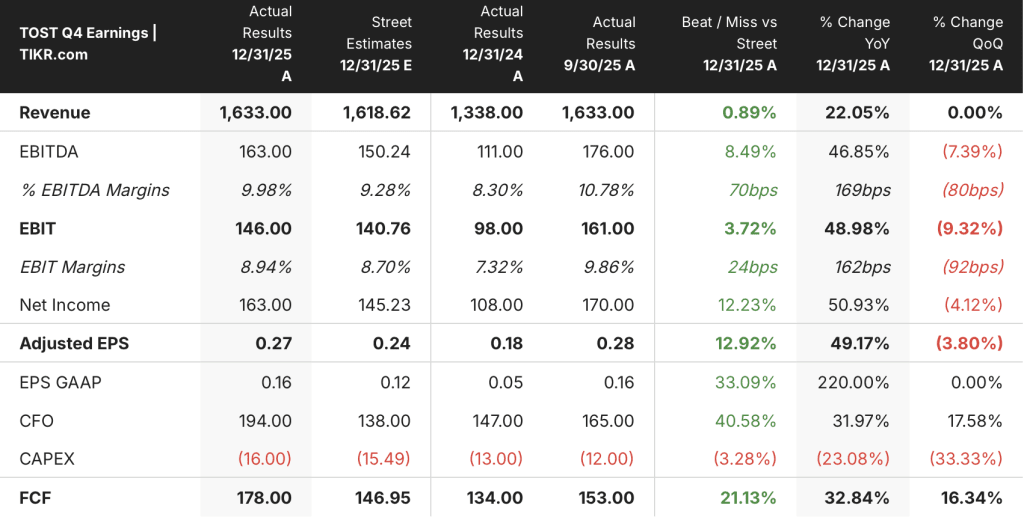

Toast stock closed Q4 2025 with results that beat Wall Street on nearly every line: revenue came in at $1,633 million against the consensus estimate of $1,619 million, while adjusted EPS of $0.27 topped the $0.24 estimate by 12.9%.

The headline number that mattered most was EBITDA, which hit $163 million in Q4, a 46.85% jump year over year and a 70-basis-point beat on margins, with the full-year figure landing at $633 million.

Toast added a record 30,000 net locations in 2025, ending the year at 164,000, and CEO Aman Narang stated on the Q4 earnings call that the company now powers 20% of SMB and mid-market restaurants in the U.S., a share that has nearly doubled over the past three years.

The platform’s subscription services revenue surged 33% for the full year to $936 million, outpacing total revenue growth of 24% to $6.15 billion, a signal that higher-value software adoption is accelerating faster than the overall business.

Beyond the core, Toast’s new markets doubled ARR in 2025, crossing $100 million, with enterprise wins including Applebee’s and Firehouse Subs representing two of the largest customer signings in the company’s history.

The international footprint now spans four markets — the U.S., Canada, the UK, Ireland, and Australia — with the Toast Go 3 handheld POS device launching in all four international markets in late April, expanding the hardware ecosystem and strengthening the go-to-market flywheel outside North America.

On the product side, Toast launched ToastIQ, a conversational AI assistant, less than four months before the earnings call, and over half of all 164,000 Toast locations had already used it, with customers collectively sending more than 8 million queries.

Toast also struck back-to-back partnership announcements in April and May: a deal with Alicart Restaurant Group covering Carmine’s Times Square (which processes up to 3,000 covers per day and more than $40 million in annual sales), a new alliance with Preferred Hotels & Resorts positioning Toast as a recommended POS provider across U.S., UK, Ireland, and Canada hotel food and beverage operations, and a strategic partnership with The Alinea Group to deploy Toast across Michelin-starred venues including Alinea and Next.

The company also returned $235 million to shareholders through share repurchases since inception of its buyback program, and the Board approved a new $500 million increase to the buyback authorization.

Guidance for full-year 2026 calls for 20% to 22% growth in recurring gross profit and Adjusted EBITDA of $775 million to $795 million, with Q1 2026 guidance of $160 million to $170 million in adjusted EBITDA and 22% to 24% recurring gross profit growth.

Wall Street’s Take on TOST Stock

TOST’s Q4 earnings confirmed what the data had been signaling for several quarters: the platform is scaling with operating leverage, and the new markets are not experiments anymore — they are compounding alongside the core.

Toast’s EBITDA grew 46.85% year over year in Q4 to $163 million, with full-year adjusted EBITDA reaching $633 million, and consensus estimates now point to around $785 million for 2026, representing roughly 27% growth on top of a year where margins already hit their medium-term targets ahead of schedule.

Fifteen of 29 analysts covering TOST have assigned a Buy rating, with 4 Outperforms and 10 Holds, carrying a mean price target of around $36, implying roughly 28% upside from the current price of $28.31; the Street is watching whether the new TAMs, including enterprise, retail, and international, can sustain the EBITDA expansion narrative as tariff and memory chip headwinds pressure hardware margins in the near term.

Narang told investors on the Q4 call that “over half of our support interactions now start digitally through an AI agent,” with 70% of those never escalating to a human, a structural cost reduction that directly expands EBITDA margins without requiring incremental investment.

GPV per location was down 1% year over year in Q4, a number to watch as consumer spending trends and macro uncertainty evolve through 2026.

Q2 and Q3 2026 EBITDA results will determine whether the 27% annual growth target holds as the memory chip headwind concentrates in the back half of the year.

What Does the Valuation Model Say?

The TIKR model’s mid case projects Toast stock reaching $82.50 by December 2034, anchored to a 13.2% revenue CAGR through 2035 and an 11.0% net income margin, both driven by continued location adds, ARPU expansion across new TAMs, and operating leverage from AI-enabled support and product infrastructure.

At $28.31, with the mid case implying a 191% total return and around 13% annualized IRR against a business already generating $633 million in adjusted EBITDA and growing EBITDA at roughly 27% forward, Toast stock is undervalued for investors with a multi-year horizon willing to let the TAM expansion thesis compound.

The investment case for Toast comes down to one question: does the platform’s multi-vertical expansion hold its monetization curve as it moves beyond restaurants?

The investment case for Toast comes down to execution: today’s Q1 2026 earnings report is the first test of whether the platform’s multi-TAM expansion holds its monetization curve under real cost pressure

What to Look for in Q1 2026 Earnings

Toast reports Q1 2026 results today after market close, with management having guided to $160 million to $170 million in adjusted EBITDA and 22% to 24% recurring gross profit growth.

- Adjusted EBITDA: consensus expects around $165 million; a print at or above $170 million would signal the hardware cost headwind is being absorbed better than feared, while a miss below $160 million reopens the margin compression debate

- Recurring gross profit growth: guidance midpoint of 23% implies the platform’s monetization engine held through a seasonally lighter Q1; watch whether SaaS ARR growth sustains the 28% pace reported in Q4 2025

- Net location adds: management guided for full-year net adds above the 30,000 record set in 2025, so Q1 sets the trajectory; any sequential deceleration in new TAM contributions (retail, enterprise, international) would be the first sign the expansion thesis is slowing

- GPV per location: after a 1% year-over-year decline in Q4, investors will watch whether consumer traffic at restaurant locations stabilizes or deteriorates further as macro uncertainty builds through Q2

- ToastIQ commentary: with over 8 million queries sent in the first four months post-launch, any monetization signal or usage-based pricing disclosure on the call would materially reprice the AI optionality currently embedded in Toast stock at zero

Should You Invest in Toast, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Toast, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Toast, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze TOST stock on TIKR for Free →