Key Stats

- Current Price: $79 (May 6, 2026)

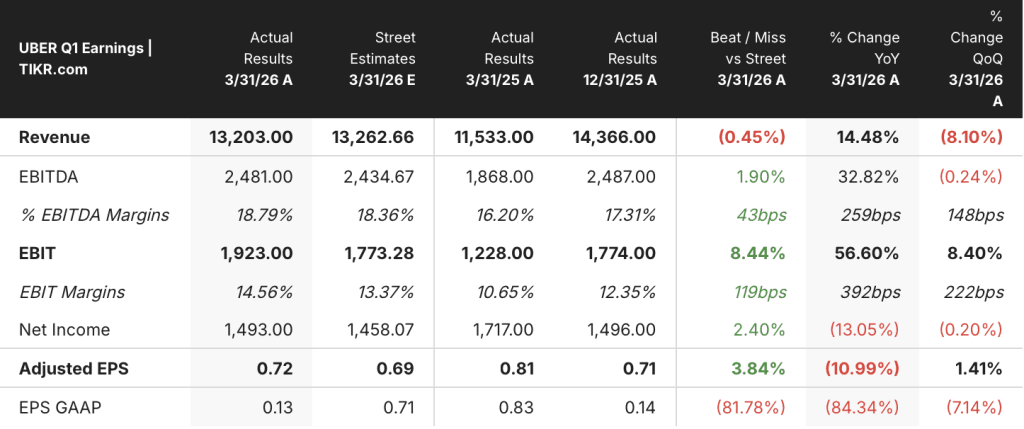

- Q1 2026 Revenue: $13.2B, +14% YoY

- Q1 2026 Adjusted EPS: $0.72

- Q1 2026 Non-GAAP EPS Growth: +44% YoY

- Q1 2026 Gross Bookings Growth: +21% YoY

- TIKR Model Price Target: $187

- Implied Upside: +136%

What Happened?

Uber stock (UBER) opened the year with gross bookings up 21% year-over-year to reach the high end of company guidance despite weather disruptions and geopolitical headwinds across operating markets.

Revenue came in at $13.2B, up 14% from $11.5B in Q1 2025, while non-GAAP EPS grew 44% year-over-year, according to CEO Dara Khosrowshahi on the Q1 2026 earnings call.

Mobility was the headline driver, with gross bookings accelerating to 20% growth alongside what Khosrowshahi described as record Mobility margins on the call.

Delivery grew 23%, led by grocery and retail, extending the momentum that has made Uber’s food and goods business increasingly central to the platform’s compounding flywheel.

Freight returned to growth for the first time in nearly two years, according to Khosrowshahi, adding a segment that had been a consistent drag on the consolidated growth narrative.

Uber One membership surpassed 50 million members, growing 50% year-over-year, with Uber One now accounting for more than 50% of gross bookings, according to Khosrowshahi on the call.

The company returned $3B to shareholders through share repurchases in Q1 alone, a record single-quarter buyback that signals management confidence in the current valuation of Uber stock.

CFO Balaji Krishnamurthy noted on the call that 2026 is expected to be the first year since COVID where Uber sees meaningful operating leverage on its U.S. Mobility insurance cost line, with hundreds of millions of dollars in savings anticipated for the full year.

Looking ahead, management’s Q2 guidance language pointed to continued momentum with disciplined capital allocation, though no specific revenue or EPS figures were disclosed on the call.

Uber Stock Financials: Operating Leverage Is Real

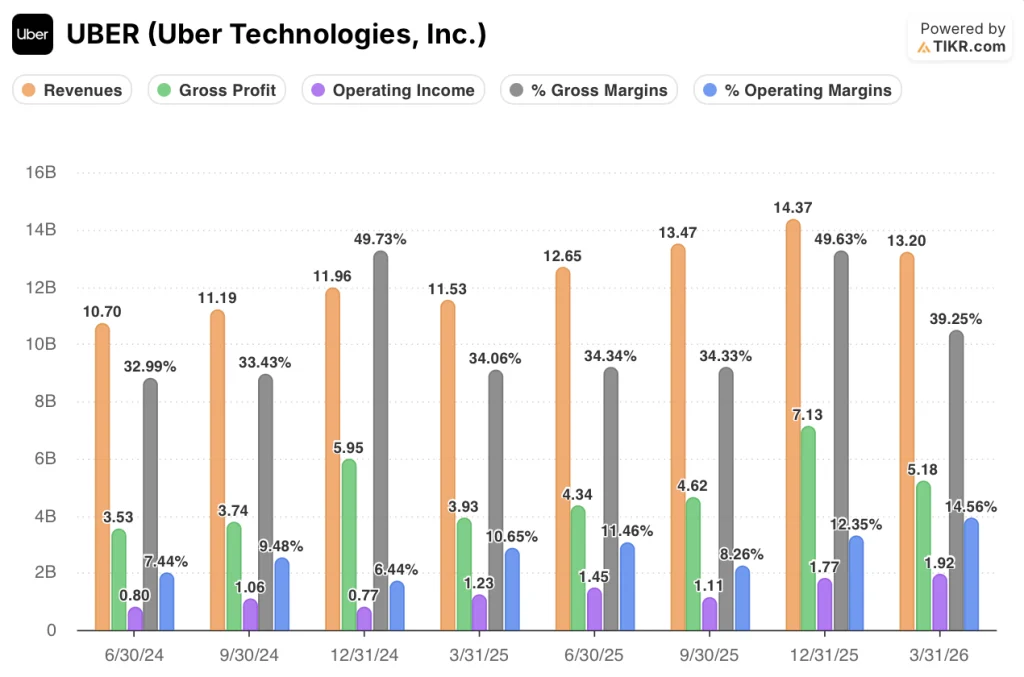

The income statement tells a clear operating leverage story: revenue has grown every quarter since Q1 2025, and operating margin has expanded from 10.6% in Q1 2025 to 14.6% in Q1 2026.

Gross margin jumped to 39.2% in Q1 2026, up from 34.1% in Q1 2025, a 510-basis-point expansion year-over-year driven by scale and mix shift toward higher-margin Mobility.

Gross profit reached $5.18B in Q1 2026, up 32% from $3.93B in the prior-year quarter, growing significantly faster than revenue and reflecting the operating leverage this platform is beginning to generate.

Operating income reached $1.92B in Q1 2026, up 57% from $1.23B in Q1 2025, with operating margin improving to 14.6% from 10.6% over the same period.

The sequential revenue dip from $14.4B in Q4 2025 to $13.2B in Q1 2026 follows the same seasonal pattern seen in the prior year, when Q1 2025 at $11.5B also trailed Q4 2024’s $12B.

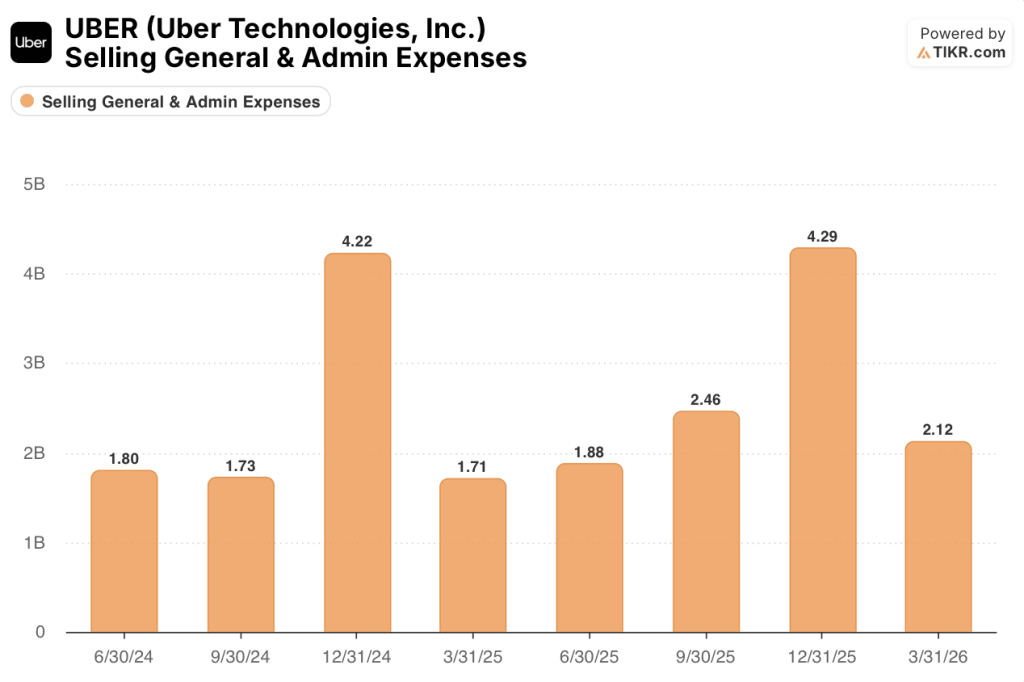

Operating margin has followed a multi-quarter expansion arc: 10.6% in Q1 2025, 11.5% in Q2 2025, 8.3% in Q3 2025, 12.3% in Q4 2025, and 14.6% in Q1 2026, with the Q3 dip driven by SG&A surging to $4.29B from $2.46B in Q2 2025, nearly doubling in a single quarter and compressing margin by 320 basis points despite revenue growing to $13.47B.

Krishnamurthy confirmed on the call that insurance cost improvements are directly translating into lower fares for riders, which is driving higher trip volumes, particularly in California markets where insurance headwinds had been most severe.

What Does the Valuation Model Say?

The TIKR model prices Uber stock at $187, implying 136% upside from the current price of $79.

The mid-case assumptions underlying that target are a revenue CAGR of 10% from 2025 to 2035 and a net income margin of 16%, both achievable given that Uber is already generating approximately 15% operating margins on a $13.2B revenue base.

The Q1 results strengthen the investment case: operating leverage is coming through ahead of expectations, the insurance cost tailwind is only beginning to materialize, and the buyback pace signals management is not waiting for the market to close the gap.

Uber stock looks mispriced at current levels if the operating leverage trend from Q1 holds through the rest of 2026.

The central question Q1 raises is whether Uber can sustain 14%-plus operating margins while simultaneously funding the AV ecosystem buildout it needs to win the next decade.

Near-Term Case

- Operating margin reached 14.6% in Q1 2026, up from 10.6% in Q1 2025, with the insurance cost line set to generate hundreds of millions in savings across the full year per CFO Balaji Krishnamurthy

- Uber One membership at 50 million and growing 50% year-over-year, with members spending 3x more than non-members and now accounting for more than 50% of gross bookings

- The $3B single-quarter buyback is the largest in company history, reducing share count and directly accreting per-share value as free cash flow scales

- U.S. Mobility is expected to accelerate further through 2026 as insurance savings translate to lower fares and higher trip elasticity, a dynamic already visible in California market data per Krishnamurthy

Long-Term Case

- AV Mobility trips grew more than 10x year-over-year per Khosrowshahi, but scaling to 15 cities by year-end requires significant investment in fleet management, depot infrastructure, financing partnerships, and insurance programs that will pressure margins

- Uber re-upped its AI spending budget mid-year after underestimating demand, a pattern that signals AI infrastructure costs are not yet stabilized and will grow faster than originally modeled

- The $15B run-rate gross bookings flowing through the Delivery app from the Mobility side of the platform represents a cross-sell opportunity, but 30% of eligible Mobility users have never used Uber Eats per Krishnamurthy, meaning the conversion upside requires additional investment to realize

- AV partner agreements with Zoox, Nuro, NVIDIA, Pony, WeRide, and Baidu create execution dependencies outside Uber’s direct control, and regulatory dialogue across up to 15 cities introduces timeline risk that could delay the AV revenue contribution the model requires

Should You Invest in Uber Technologies, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Uber Technologies, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Uber Technologies, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze UBER stock on TIKR for Free →